The numbers are compelling and scary — community financial institutions are in serious danger of losing a quarter of their core deposits in the next 4-5 years. What’s the cause? Aging account holders who are coming to the end of their lives. It’s not a pleasant thought, but it’s a reality in which banks and credit unions play an important role, as estate planners and executors.

However, today’s community financial institutions face a subsequent challenge: they need to capture enough young account holders to replace the “legacy” deposits of their oldest and most loyal consumers. And they need a lot of them (approximately 11 new accounts for each lost). Megabanks have the edge here. According to The Financial Brand, a full 47% of Gen Z uses a megabank as their primary financial institution.

A family that stays together may not bank together.

Once upon a time, kids just opened up accounts wherever their parents banked, so multiple generations would rely on a single institution to serve their needs. But today’s young adults don’t think about their money the way their parents and grandparents do. They look for a great product and then seek out an institution that can provide it. They settle transactions over Venmo and Square rather than exchanging cash or checks. They expect convenience and cutting-edge technology — having a physical branch nearby is more novelty than necessity.

What do younger consumers want in an account? Rewards.

So what’s your plan to capture these digital denizens? If your answer includes ideas like “standard free checking,” “toasters,” and “discount tickets to Six Flags,” you may be in for a rude awakening. Millennials and Generation Z are willing to develop loyalty for a brand, but only on their terms. They want rewards. In fact, a 2016 study indicated that 8 out of 10 Millennials would switch institutions for better rewards.

Regular free checking is broke, and you need to fix it.

Let’s start with the “golden standard” also known as “standard free checking.” It’s a product that nearly every community financial institution relies on, but at its best, probably inspires the same warm feelings as shoe polish and printer ink — useful, even necessary, but nothing to brag about.

Lots of people use free checking, but they’re older than is ideal for your long-term strategy. We analyzed data from more than 500 community banks and credit unions that Kasasa has worked with over the last 15 years and uncovered some useful demographic insight:

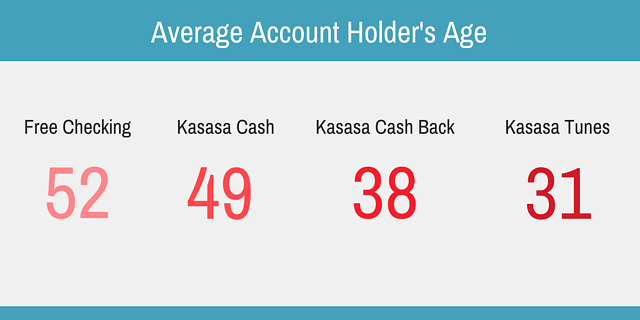

The median age for standard free checking: 52.

Now, while that may not seem problematic on the surface, it means that fully 50% of account holders are older than that. And you already know that nearly half of Generation Z deposits their money at a megabank. That doesn’t leave many options for backfilling your aging deposits.

How does reward checking stack up? Take a look.

The median ages for Kasasa’s three reward checking accounts are as follows:

Kasasa Cash: 49

Kasasa Cash Back: 38

Kasasa Tunes: 31

These ages are important because they say a lot about the future of an institution, the health of its deposit mix, and the strength of its revenue stream. Kasasa reward accounts not only bring in younger account holders, but they also provide an extremely stable source of low-cost core deposits and consumer-friendly non-interest income.

- Kasasa Cash offers high-yield on balances — appealing to those with excess income seeking easier access to their money than a certificate of deposit allows.

- Kasasa Cash Back rewards account holders with cash back on all their purchases up to a preset limit — this is attractive for people with lower average balances and high transaction volume.

- Kasasa Tunes incentivizes account holders with reimbursements for purchases made on Amazon® , iTunes®, and Google Play® — drawing in the youngest consumers who may be establishing their first relationship with a financial institution.

A strategy that works

Ask yourself, “which type of account holders does your institution need to counterbalance the change in your demographics?” and “is free checking your only tool for attracting the next generation of account holders?”

In order to turn the tide in your favor, you will need products that appeal to younger consumers and keep them engaged with you for the long haul. Younger consumers will eventually need car loans, mortgages, and other financial services — but you’ll never earn their loyalty if you can’t get their attention with rewards that fit their lifestyle.