There’s strong evidence that the pandemic is waning. That’s reason enough for businesses and investors to breathe a sigh of relief. As we set our eyes on what’s next for the economy, I think the banking industry holds lessons for the rest of us. Even for financial institutions that boldly positioned themselves for growth in 2020, that growth came in unexpected ways. Today, those that are the most well-positioned for success in 2021 have prepared themselves to pivot tactically, while keeping their mission strong.

In the months since the coronavirus pandemic began, community banks and credit unions saw their balance sheets thrown out of whack. Leaders at financial institutions will be digesting the influx of assets and liabilities for an unknown amount of time.

Stimulus programs had the desired effect at a macro level for banks and credit unions, although many continued to feel unsettled by the challenges they faced coming out of 2020. Margin compression, reduced branch hours, relatively lower loan demand, and aggressive movement by neo-banks and megabanks have left many financial institutions unsure of the next right thing.

Many halted their marketing efforts due to uncertainty. A select few re-entered the fray, ready to reassure and serve consumers. These institutions positioned themselves for growth — but deposit growth needs to be paired with loan growth. And not all deposits and loans are created equal. Financial institutions need to develop quality, long-term relationships with their account holders, both commercial and retail, if they want to be around in 20 or even ten years.

Unexpected factors influenced decision-making at banks and credit unions.

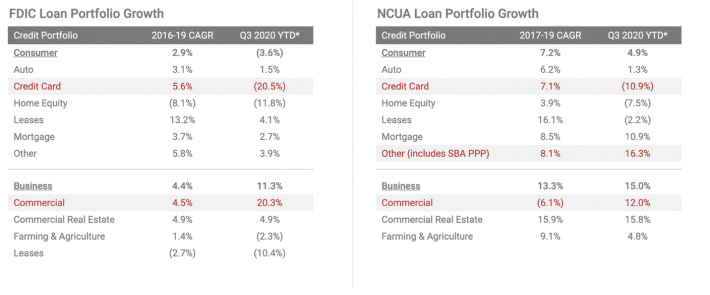

Commercial lending at banks grew by 20.3% and by 12.0% for credit unions in Q3. Credit card balances fell; consumers used their stimulus checks to pay them down. Many businesses that received PPP loans were required to open a commercial checking account to get the loan. This is a relationship of necessity that financial institutions must work hard to convert into genuine loyalty.

On the retail front, many consumers appeared to retrench, anticipating the need to use their lines of credit later. Banks and credit unions felt a one-two punch to their balance sheets as savings ballooned and many lending categories fizzled.

Business lending dominated bank and credit union portfolios as consumer lending stagnated.

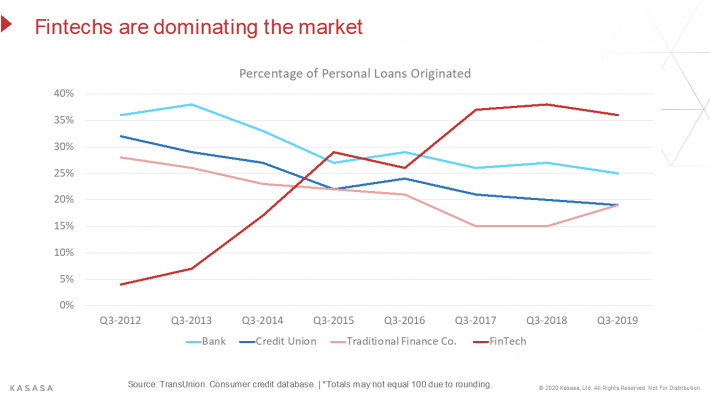

Financial institutions felt the effect of the pandemic across their entire operation. Stay-at-home orders all but eliminated foot traffic and cratered account acquisition campaigns across the board. Fintechs were already starting to devour market share. But this triggered an even more massive shift in consumer behavior: people embraced digital banking at lightning speed, which placed painful and long overdue pressure on banks and credit unions to virtualize their operations.

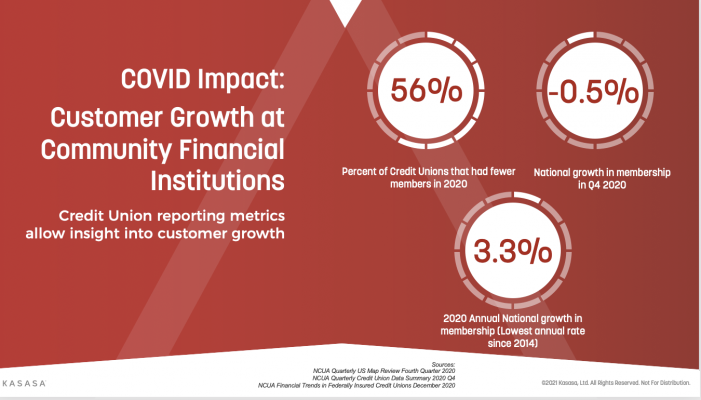

Credit union data used here to illustrate the impact of the pandemic to owned account holder relationships.

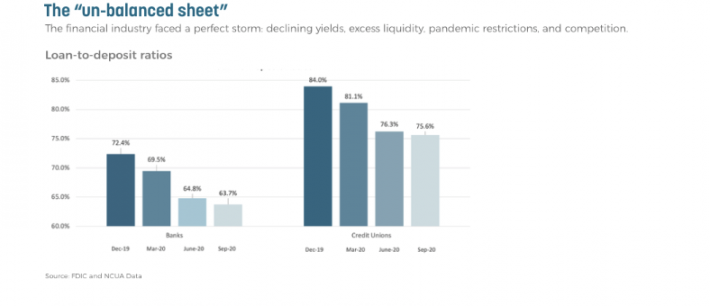

Uncle Sam and the Fed swung hard at the problem, creating "un-balanced" sheets for banks and credit unions.

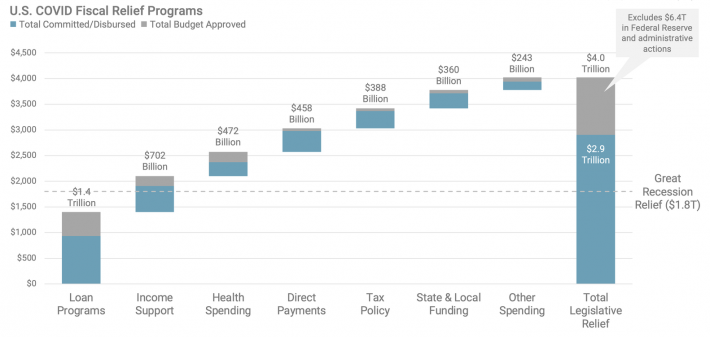

The U.S. government unleashed an unprecedented amount of fiscal and monetary support. The Federal Reserve Bank took dramatic action to support the nation's banks and credit unions. These efforts restored confidence that financial institutions, businesses, and consumers would cast adrift in a faltering economy and global health crisis.

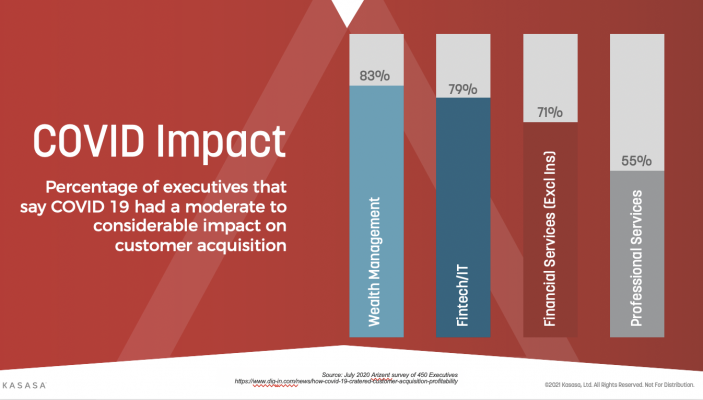

Nonetheless, the financial industry faced a perfect storm: declining yields, excess liquidity, pandemic restrictions, and competition from digitally native financial technology firms. It seemed the only way to survive was to hunker down and hope that the economic weather would calm down.

The stimulus dollars and consumer changes resulted in excess liquidity and put additional pressure on margins. The Federal Reserve Bank may recommend that institutions cut expenses, focus on non-interest income, and grow loans, but this advice is easier said than done.

And although many banks and credit unions will follow the Fed's guidance to the letter, they will only see lackluster results. Conventional strategies lead to conventional outcomes. Neo-banks have ignored the memo about cutting back and they're using the inaction of financial institutions to aggressively market to and acquire new account holders. Megabanks hold gargantuan balance sheets, allowing them to juggle some numbers before they resume business as usual.

Balance sheets won't be upside down forever, but it will take time for this much stimulus to be "digested." Many smaller institutions find themselves struggling to make big strategic moves due to the burden of margin compression and expense reduction.

Business as usual is never coming back.

Here's the uncomfortable truth that most banks and credit unions need to embrace: Now may not feel like the right time to make aggressive moves or big bets to grow, but by the time it does feel right, the competition will have disappeared over the horizon.

The beauty of our banking system lies in the potential for collaboration. Every community has unique needs — banks and credit unions are wise to tailor their operations to those needs. And workflows such as account opening, account management, customer service, and marketing must be treated as top priorities for digital experiences.

Stay the course: serve your community's needs. Prepare to pivot: Digital banking experiences are the gateway to long-term growth and success.

About the author:

Patrick Dickson serves as the Chief Research Analyst for Kasasa. Patrick analyzes Kasasa’s vast data set and economic conditions to uncover and refine insights that result in actionable intelligence for Kasasa’s community financial institution partners. Patrick has extensive experience in strategic planning, financial analysis, mergers & acquisitions, and stock valuation.

This article was originally published on Nasdaq.com.