In Part 1 of this series on Boomers and Millennials, we interviewed a handful of people and learned how their life experiences affected their banking behaviors. This is a powerful way to connect with real people and empathize with their situations. It can also lead to insights into how your institution can better serve your community (meaning that you should get to know your account holders to learn more about them).

In Part 2 we’ll zoom out and look at the big picture. What are some of the national trends for these generational cohorts? How will these trends affect their financial needs and choices in the next 5 to 10 years?

Take a look at the numbers

As a cohort, Millennials stand out for a number of reasons:

-

They make up 51% of mortgage purchases (Gen Z are only 2%). Followed by Boomers (32%).

-

They have the highest activity for point-of-sale transactions compared to any other generation.

-

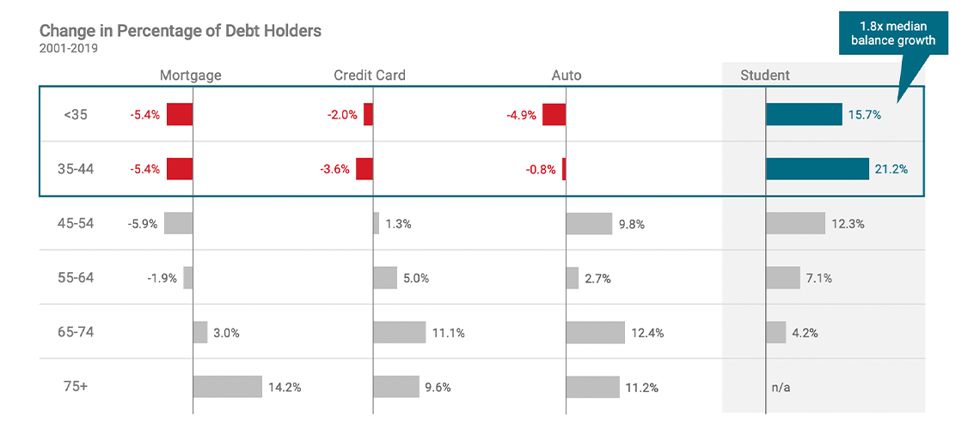

They also don’t have a lot of credit card debt but do have a lot of student loans.

Boomers have some similarities with their Millennial children, and some big differences:

-

They are the second highest mortgage holders (after Millennials).

-

They have the second lowest activity for point-of-sale transactions (only the Silent generation is lower).

-

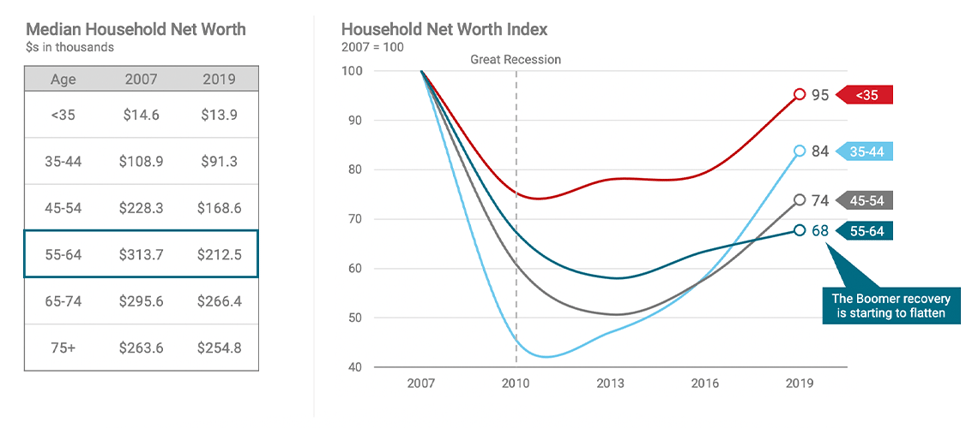

Their household net worth may never fully recover to pre-crisis levels.

-

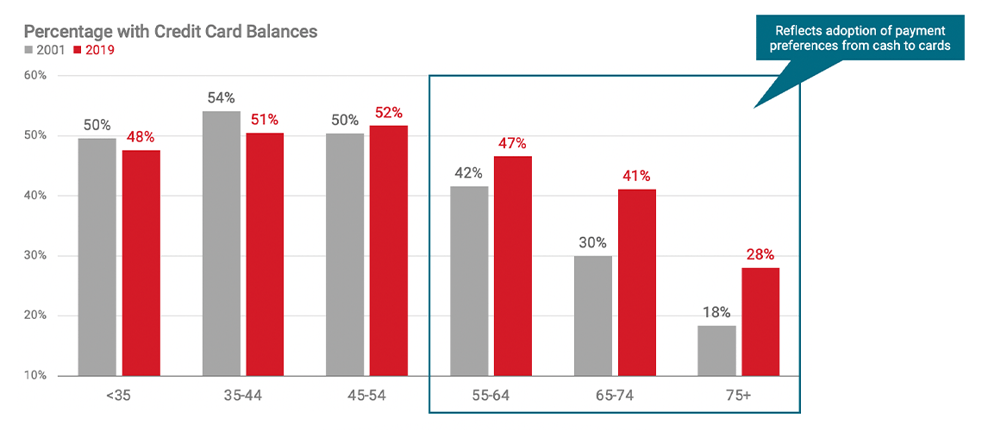

Older consumers are more likely to carry credit card debt today than ever before.

How can you use this information to act now?

It’s important to blend the macro and micro perspectives together. Make sure to read Part 1 of this series for the micro view. National and regional trends can help you avoid major missteps and capitalize on major opportunities. Alternatively, talking with individual account holders can help you uncover needs and opportunities that national economic data may obscure — that’s also the secret to building deep loyalty in your community. You want to be seen as a partner that listens and responds to feedback, as well as a strategic player that navigates economic turbulence with ease.

Look at your consumers’ behavior. Conduct your own research by analyzing the transaction data from your account holders to discover behaviors that may help your decision-making process. Where are they already paying debt to other lenders or institutions and can you offer them a better rate? What types of payment services do they use (e.g. Paypay, Cash, Venmo, Zelle, etc.)? Are they using out-of-network ATMs? Are they over-paying for services like insurance or identity protection?

The possibilities are endless when you examine your own data.

Hear what they say. But watch what they DO. Don’t be surprised if you find data that flies in the face of what your interview subjects said. It’s not uncommon for people to answer questions in an aspirational way (e.g. how much money do you want to save? How often do you buy Starbucks?) and their behavior doesn’t match up. Ultimately you want to use empathy as a lens for examining these disconnects between the data and the interview findings. It’s no secret that people aren’t as financially stable as they want to be. If you can find ways to meet them where they are to help them get to where they want to be, you’ll win their loyalty.