There is a crisis looming in the form of an evaporating funding pool. Deposits might not be a strategic goal today, but increased competition and changing preferences of future generations could mean that by the time you need them, it's too late. Look at the age distribution of accounts and a picture becomes obvious: the time to address the issue is today.

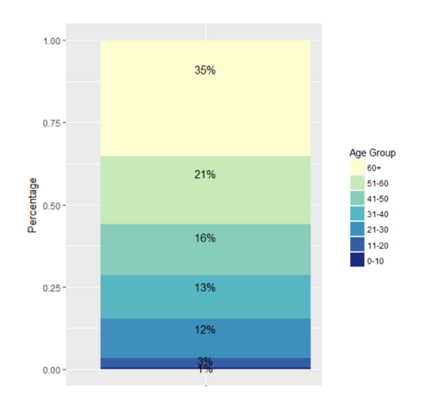

Age Distribution of Accounts

To better understand what age distribution at community banks and credit unions looked like we took a sample of 29,000 accounts from non-Kasasa community financial institutions.

More than half (56%) of the consumers in this data set were over the age of 50. That average account holder age was 52. We dove further into the 60+ group and found that 11% of the sample set fell between the ages of 65 and 74. 8.5% were over the age of 75. In the United States, the average life expectancy is 78.74 years.

Not Just Age, but Balance too.

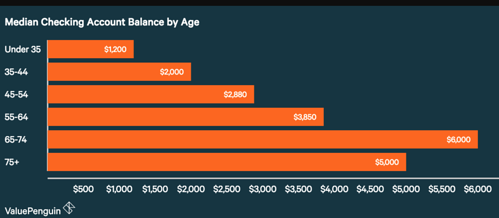

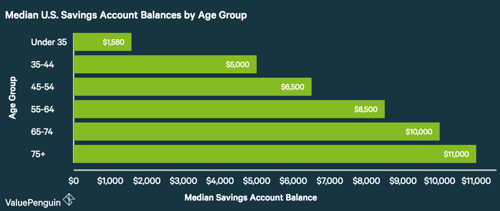

Of course, we know that not all accounts are equal. Some members or customers carry higher balances than other. As it turns out, there is often a correlation between balance and age. Value Penguin found the following breakdown for savings and checking accounts.

If you combine the checking and savings account value, you'll have a complete DDA average balance for the respective age groups.

Under 35: $2,780

35 - 44: $7,000

45 - 54: $9,380

55 - 64: $12,350

65 - 75: $16,000

75+: $16,000

In our dataset of 29,000 accounts, we found similar results.

Under 35: $1,912

35 - 44: $4,266

45 - 54: $5,502

55 - 64: $9,834

65 - 75: $17,302

75+: $21,319

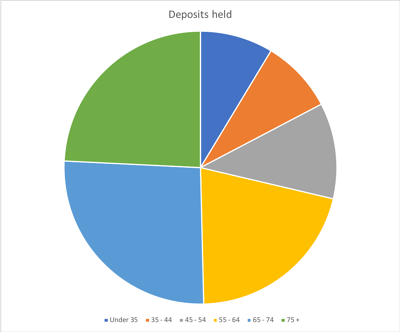

From here we can see that while account holders aged 60+ might only constitute 35% of accounts, they hold over just half (50.38%) of the deposits. Consumers over the age of 75 held 24.22% of deposits. This means there is a very real chance that you could lose a quarter of your funding within the next four years.

Are You Growing Quickly Enough?

The average account holder aged 75+ has $21,319 in deposits and the average account holder under age 35 has $1,912. To avoid a funding crisis, you need to attract 11 new average 35-year-olds for every account holder over 75 that you lose.

Let's pretend you have 3,500 account holders and that your age distributions roughly mirrors the average. That would mean you have 297 account holders over the age of 75. Based on the 11-to-1 ratio outlined above, you will need to attract 3,272 new accounts in the next four years.

That's 818 accounts a year.

What About Wealth Transfer?

Of course, there is an expectation that as your account holders mature they will gain wealth or inherit some of the unused funds. Will it be enough?

Time will tell, but many factors suggest not.

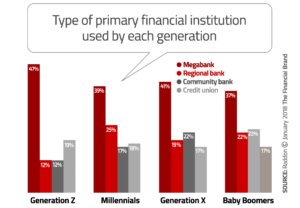

- Younger generations (Millennials and Gen Z) aren't choosing to do business with community financial institutions. So while these groups might inherit wealth, that wealth won't remain at your institution. Bank of America already has a relationship with 1 in 5 members of Gen Z.

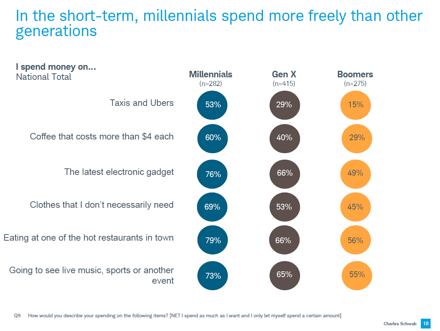

- Millennials are earning 20% less than prior generations did at the same age.

- They are also entering the workforce with more debt. Right now, the average student debt is $37,172.

- Half of Millennials are living paycheck-to-paycheck.

- This generation is also spending more than other generations.

Don't Count on CDs Either

Another traditional funding source seems to be evaporating: certificate of deposits. BankRate did a survey in 2014 and found that of respondents between the ages of 18 and 29, 69% weren't familiar with CDs and 94% had never put money into CDs.

The survey also found that sentiments around investing are also changing. Younger generations expect:

- Liquidity -- The younger the saver, the more important liquidity was.

- Higher yields -- Since liquidity is so important, there is an expectation that the trade-off is worth it. National averages are hovering around 2%. This rate is too low and the penalties too strong to make this an appealing short to mid-term investment.

- Technology -- Younger generations also prioritize an easy digital experience and the app market is flooded with options that are winning those investment dollars. Some even help automate the process or encourage investing in ETFs.

What Can You Do?

To attract younger audiences, you have to offer the products/services they want and then market to them effectively. Fortunately, we've done extensive research into how this audience shops and you can get it for free.

Get the Complete Millennial Study