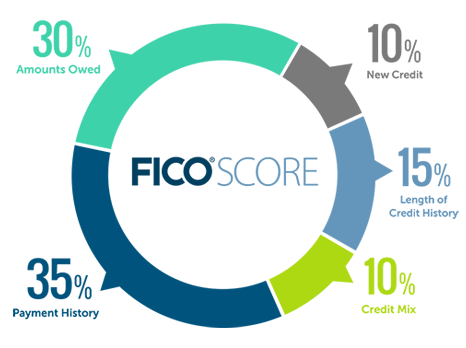

A recent announcement from FICO (creator of the venerable credit score) has the potential to impact millions of Americans in the coming year. While the main data points used to determine credit scores aren’t changing, borrower behavior will be more heavily scrutinized, which could have far-reaching consequences for individuals who are struggling financially and leaning on lines of credit to stay afloat.

The new FICO scores aim deeper into borrower history.

FICO plans on rolling out two new scores: FICO 10 and FICO 10 T. Both scores will take a closer look at how a borrower’s behavior is impacting their overall debt. For example, borrowers who consolidate their debts but continue to incur debt through other means (credit cards, for example) will see their scores impacted more significantly than in the past.

The FICO 10 T score will also take a deeper look into a borrower’s history. Today’s scoring system relies on a static month’s worth of data, among other metrics, to evaluate a borrower’s creditworthiness. The new score will take the borrower’s last two years of credit history into consideration. This clearly puts the favor on people with longer histories of better borrower behavior.

How will the new FICO scores affect borrowers?

Credit bureaus will begin providing the new scores this coming summer. However, some lenders (including Fannie and Freddie) are still required to use the old scores. And it ultimately comes down to the lender: whether they choose to use the new scores when determining creditworthiness is up to them.

That being said, because the new system will better help lenders identify potentially risky borrowers, many institutions will likely begin defaulting to the new scores as they roll out. Borrowers whose scores are negatively impacted can expect higher interest rates, and in some cases, not qualifying for loans that previously may have been within reach. Borrowers with good credit history will see their scores go up to some degree.

Community financial institutions are uniquely positioned to help.

The theory of a credit score is to provide an unbiased metric that facilitates manageable debt for consumers and productive loans for lenders. It’s easy to see how the new scores will enhance this goal, even if those with lowers scores may feel unfairly targeted. For households that rely on credit to make ends meet, these changes may signal hard times ahead.

Alternatively, it puts community financial institutions in a position to help their account holders take beneficial steps now in preparation for future borrowing needs. Paying down credit card debt and keeping it low will make a big difference.

A flexible lending solution like the Kasasa Loan could provide just the right solution, especially when used as a debt consolidation tool. With a Kasasa Loan the borrower has the ability to pay a loan off faster and save on interest, while maintaining access to excess funds if need be.

This isn’t the first time FICO has offered new scores aimed at specific portions of the lending market, and it won’t be the last. These types of changes are a great opportunity for your institution to support consumers through education and products that meet their financial needs.