Who participated in the Social Media Survey?

The social media survey was promoted through three channels; Kasasa's "expert exchange," through our social media channels, and through our friends at CBANC. We received a total of 112 responses. 56% of those were Community Banks and 44% were Credit Unions.

Key Takeaways from the Survey

- The biggest influence on the size of your social audience is time.

- Bankers who believe their social media is effective spent most of their budget on social media advertisements.

- Facebook is well adopted but there is an opportunity for growth on other social media platforms.

- Bankers are unsure about whether their social media efforts are having an impact on business objectives.

Here is a breakdown of each question that was asked, the results, and our interpretation of the data.

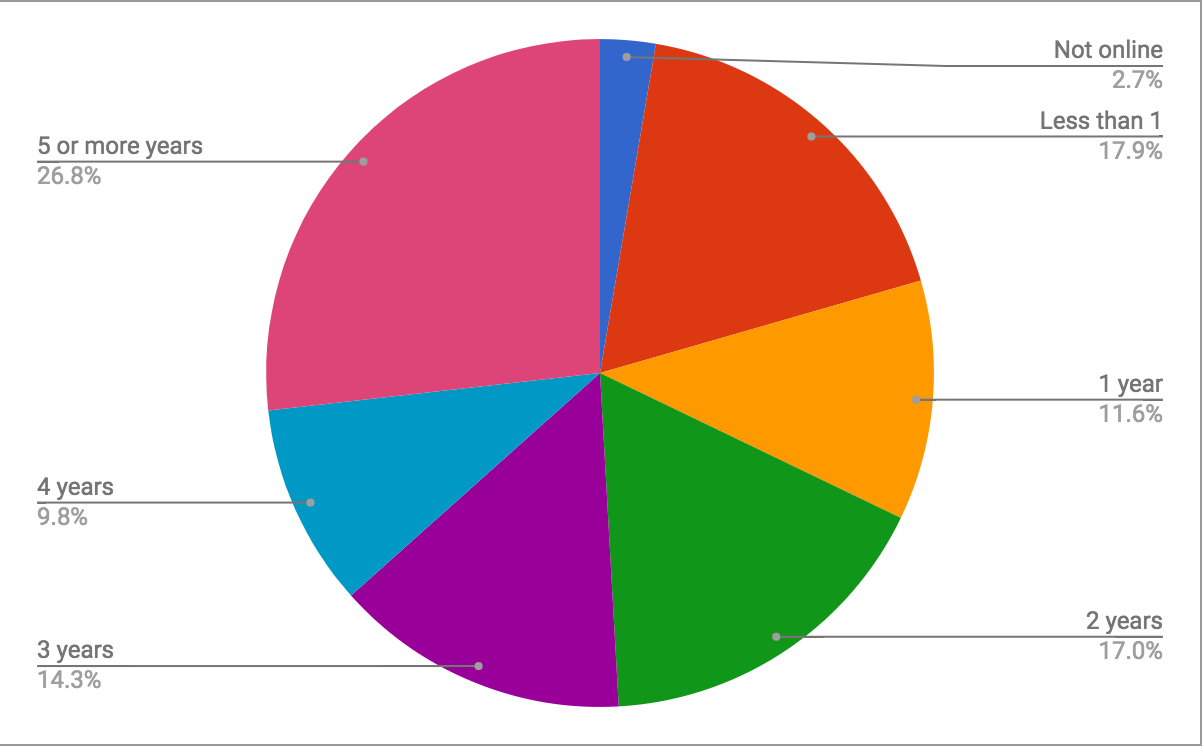

How many years has your institution been using social media?

Surprised?

When reading about social media in the financial industry you get the distinct impressions that for many institutions it is a new addition. While that is true for some (29.5% reported being active for a year or less), a majority of respondents have been active on social media for at least 3 years. On average, community financial institutions have been active on social media for 2.85 years.

What does this mean?

- You can assume with some degree of confidence that (1) your competitors are on social media (2) your customers expect you to be there (3) if you haven't started yet then you're behind.

- Regulation needs to catch up. Platforms are evolving at a breakneck pace and the FFIEC social media guidance hasn't been updated since 2013. Think of all the things that weren't available on Facebook when that guidance was authored. Institutions should invest time talking to industry experts who can help interpret outdated regulation for emerging trends.

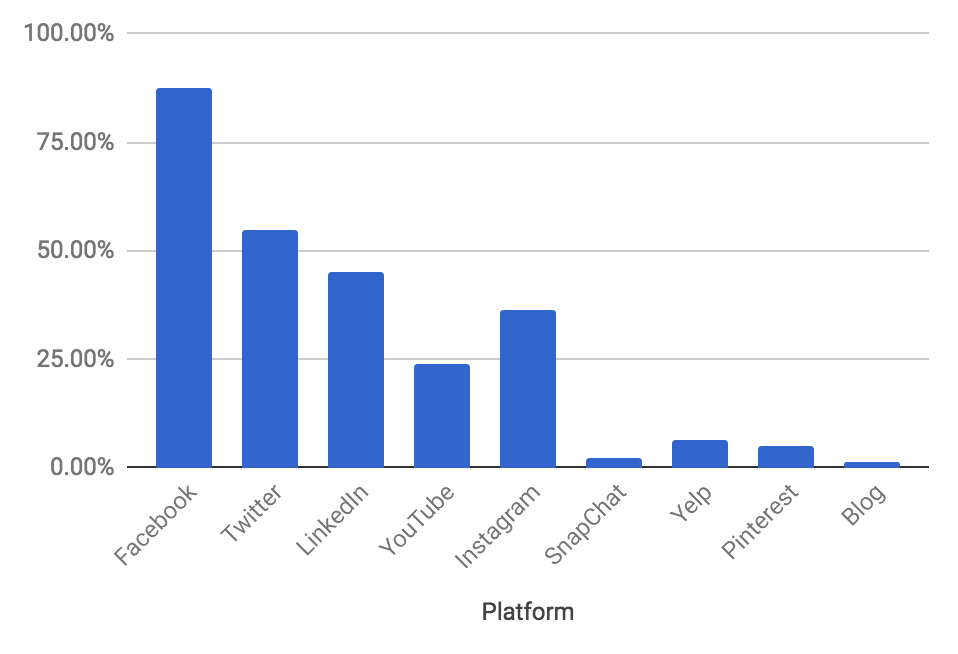

What social media platforms do you have a presence on?

Facebook is king; 87% of institutions reported being active on Facebook. Generally, Facebook is the right place to start and we like the approach of mastering one platform before exploring others. The data supports this trend as there was a correlation between the number of years being active on social media and the number of platforms an institution maintained a presence.

Institutions who have been on for a year or less were on an average of 1.35 platforms. Institutions with 5 or more years experience were on 4.56 platforms.

One thing that caught us by surprise was the lack of adoption of Yelp. This is troubling for two reasons: (1) 25% of Yelpers have used the platform to find financial services. 25% of 84 million is a lot of potential customers. (2) Yelp is designed to solicit feedback, both positive and negative. Your institution has a listing regardless of if you created it or not, which means ignoring the feedback could pose a reputation risk to your institution.

What does this mean?

Start with one channel and focus on it until you find success. Facebook is the most common, likely because it is so widely adopted, but consider researching the benefits and content requirements of each channel. For example, if you are looking to do business development Twitter or LinkedIn would be a better place to start. If you are targeting younger consumers, look to Instagram.

Yelp should increasingly become table stakes for all community banks and credit unions. If you're interested in incorporating this platform, check out our Yelp optimization guide.

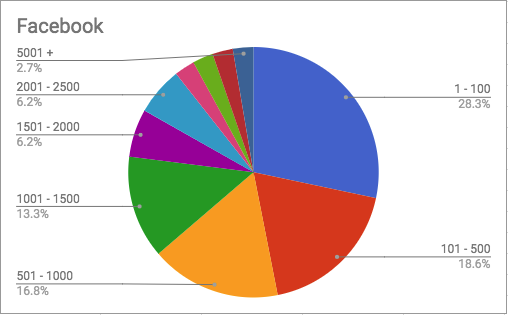

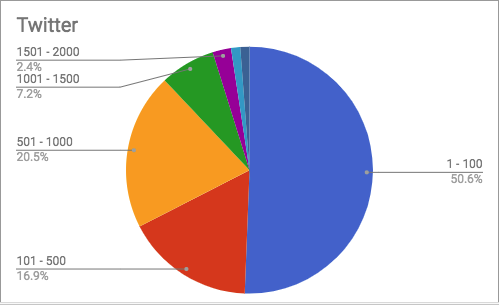

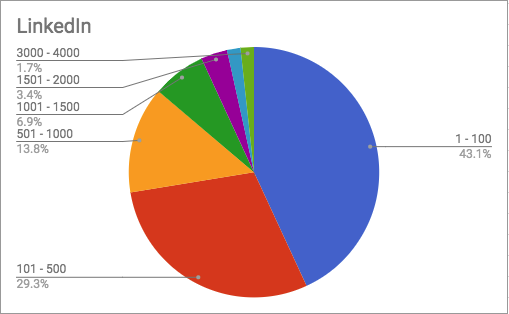

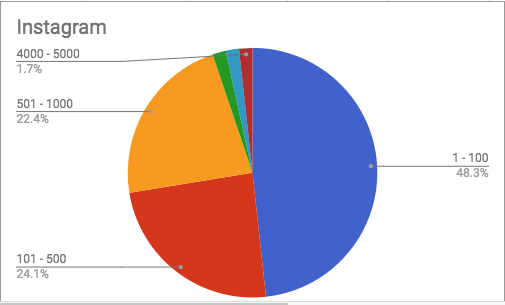

How many fans do you have?

Since banks and credit unions are only really active on Facebook, Twitter, LinkedIn, and Instagram, we'll focus on those platforms for the platform performance metrics.

There is a correlation between the number of years an institution is active on social media and fan count. Of the 11 institutions reporting over 4,000 Facebook fans, the average number of years marketing on social media was 4.77 years. For institutions reporting under 500 fans, the average number of years on social media was 1.86.

Interestingly, there was not a correlation between fan count and size of the budget. Over half the institutions with the largest followings reported a social media budget under $5,000.

Here is a set of benchmarks (according to this social media survey) for the average number of social media fans for banks and credit unions:

Facebook: 1,000 - 1,500

Twitter: 101 - 500

LinkedIn: 101 - 500

Instagram: 101 - 500

What does this mean?

Time is your greatest resource. Social media is like saving for retirement -- it requires consistent contributions over time and there is a "compounding interest" effect.

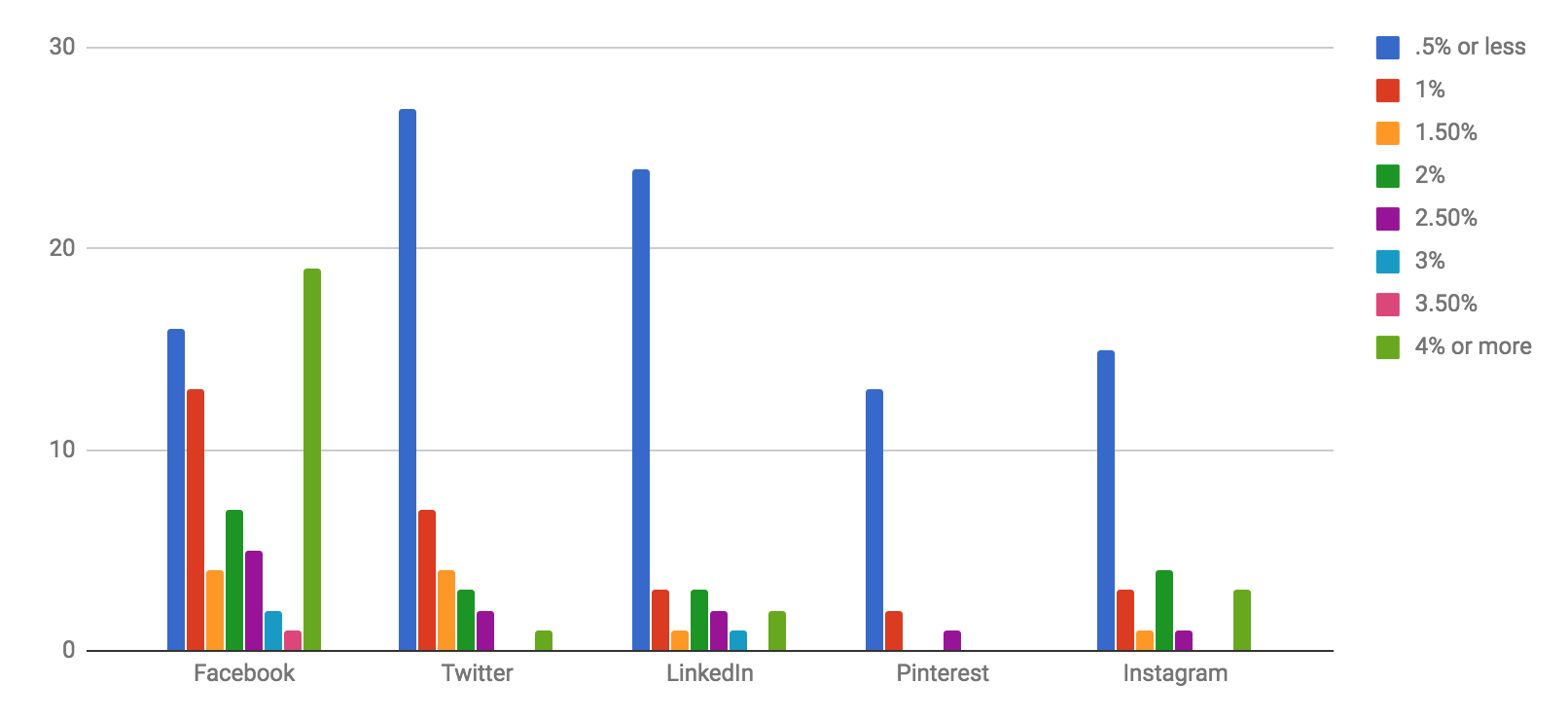

What are your engagements rates for each platform?

Okay, we have to be honest. These results surprised us and we questioned the accuracy of the reported Facebook engagement rates. One possible explanation is that there are two commonly accepted ways to calculate engagement rates.

- Post reactions / Total Fan Count

- Post Reactions / Post impressions

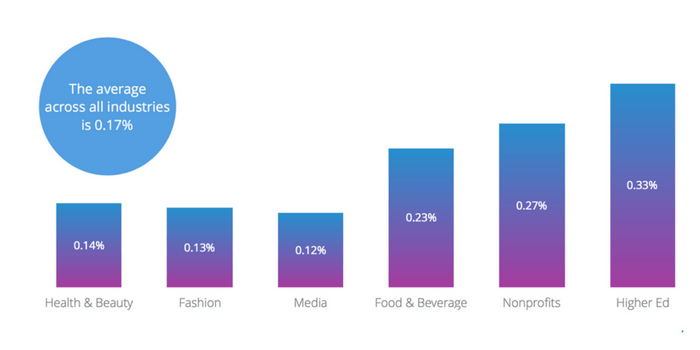

If you use the second calculation, then your engagement rates will be higher than if you use the first. Our friends at RivalIQ use the first formula to calculate engagement rate and prepared this study that looks at engagement rates across many industries.

As you can see, the average engagement rate is much lower than what was reported in our study. We looked at 100 community bank and credit union pages and calculated the average engagement rate to be .166%. This number puts us slightly lower than the "across all industries" average.

According to our social media survey group, the average engagement rate for Twitter, Linkedin, and Instagram were all under 1%.

What does this mean?

Benchmarking against others in our industry can be tricky due to how different organizations report their engagement rates. A more useful exercise is to benchmark against yourself, either month-over-month or year-over-year. It's also critical to connect metrics to business objectives. For example, community growth is only valuable if you have a business objective of brand awareness or customer engagement. If brand awareness is your primary objective then you should be comparing the cost-per-impression on social media as compared to radio, print, or other marketing channels you're using.

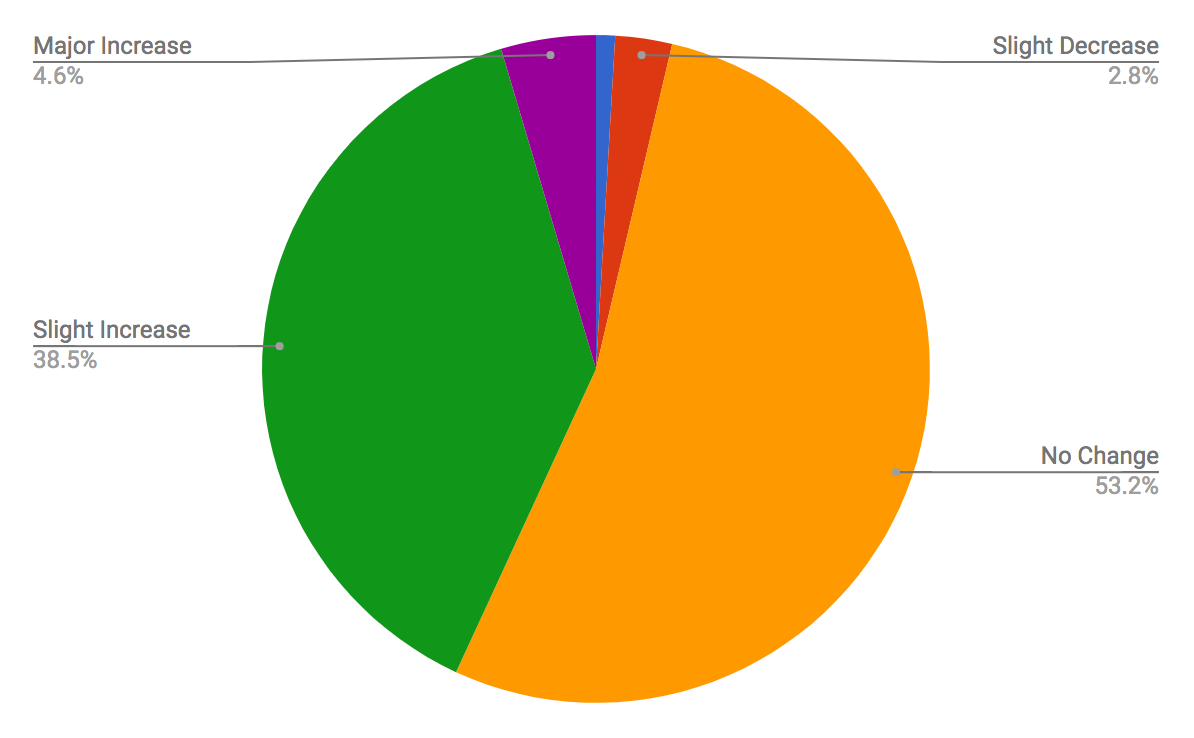

What does your social media budget look like?

Most community banks and credit unions (56%) spend under $1,000 a year on their social media efforts. However, things are changing. Here is how institutions responded when asked about their future budgets.

43.1% of community banks and credit unions are planning to increase their social media marketing budget. We think this is a reflection of the increased importance of social media in the marketing mix and the fact that every social media network is becoming increasingly pay-to-play.

One thing we found especially interesting was that there was no correlation between the current or projected budget and how successful a bank or credit union rated their social media effectiveness. 97% of those who were unsure or disagreed with the statement "Our social media marketing is effective" were planning to keep their social budget the same or increase their spending in 2018. This emphasized the importance of tying your social media marketing efforts to business objectives and determining an accurate social media ROI.

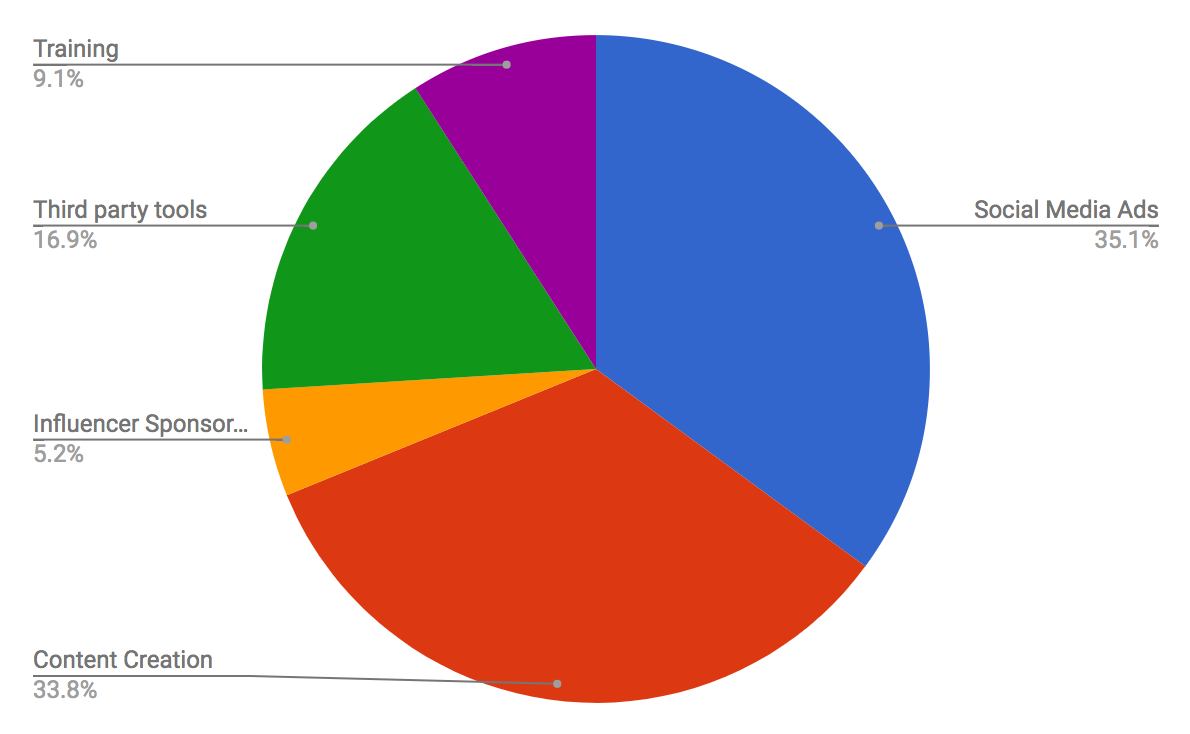

We also asked where community banks and credit unions are spending a majority of their social media budget.

Of those institutions spending more than $10,000, the most common expense was third-party tools.

Of those spending under $5,000, the most common answer was Social Media Ads followed closely by Content Creation.

The higher budgets had a correlation with time invested. Institutions reporting spend of over $10,000 also invested more than 11 hours a week into social media. Those spending under $5,000 invested between 1 and 5 hours on social media.

What does this mean?

Social media isn't free. Social media platforms, as a business, make money by creating an audience and charging you to reach them. You can do some of this through organic strategies but as the space gets more crowded and the social media platforms become more sophisticated, this will be harder to do.

You should plan for a social media budget and test which investments best deliver on your business objectives. Facebook Ads can be evaluated with as little as $5.00 a day. Here are some suggestions for getting started with Facebook ads.

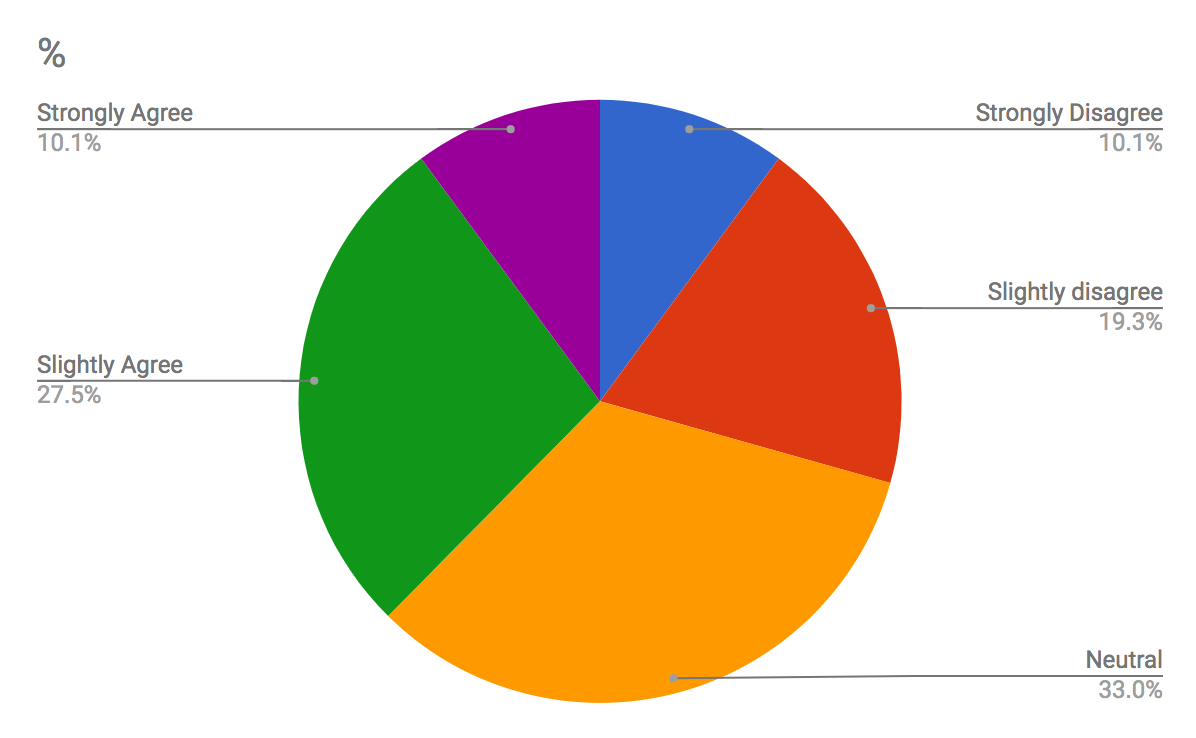

How strongly do you agree with the statement "Our social media marketing is effective."

This chart isn't terribly revealing by itself, but when you compare the data with other metrics a more interesting picture emerges.

For those who disagreed with the statement "Our social media marketing is effective," the biggest expense was content creation. (50% v.s. the social media survey average of 33.8%)

Of those who agreed with the statement, the biggest expense was social media advertising. (58% v.s. the social media survey average of 35.1%).

More simply put, institutions who spent their money on ads felt their strategy was more effective than those who invested in content creation. Does this mean that ads are more effective or does it mean that we like the transactional nature of ads? Ads are much easier to measure which makes it easier for us to determine how sound the investment was.

Another point of interest is that those who agreed with the statement reported an average engagement rate of 2.44% while those who didn't agree reported a 1.33% engagement rate. There was no difference in audience size. This leads us to believe that "effectiveness" in most bank marketers minds is connected to engagement rates.

What does this mean?

It's not how much you spend, but where you spend it. Make sure the tactics you spend money on align with your business goals and you determine what "success" looks like before you start. Not all tactics have an easy-to-measure metric. Ads can be a great place to start as they are easy to run and provide you with a wealth of data.

Closing

We appreciate everyone who participated in this social media survey and want to give a special thank you to CBANC and RivalIQ for assisting in the execution and interpretation of the data we received. We'd also love to hear what you thought of the data and if you have any questions you'd like for us to ask in our 2018 social media survey. Please feel free to leave your thoughts in the comments or email them to social@kasasa.com.