You're out for dinner and the waiter hands you the wine menu. It's at least thirty pages long, each page highlighting different wines from all over the world. You know you prefer white wines, so that instantly rules out half of the options. You also prefer Pinot Grigio, which further culls the list. However, you're still looking at a list of around 30 wines.

This example demonstrates the mental process that everyone experiences when shopping a market that's saturated with options. We try to eliminate huge categories with mental filters. This works when the filters reduce the selection to a single option. But more and more frequently we find that, despite our best efforts, the filtering process leaves us facing a multitude of very similar options. Options that appear to be essentially the same to everyone except connoisseurs.

Thanks to the accessibility of the internet, we've reached this point in banking.

The Sea of Same

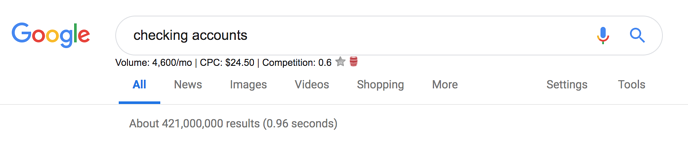

A Google search for "checking accounts" returns 421,000,000 options. 421 million. Not only do consumers have plenty of financial institutions from which to choose, there are additional product choices to be made once that consumer has settled on a bank or credit union. Do they put their emergency fund in a savings account, CD, or MMA? What of the multiple variants of checking accounts should they choose?

Consumers are bombarded with options and, while that makes for overall better products, they can't tell the difference. 53% of Millennials think all banks are the same.

On some level, this makes sense. Financial institutions are all playing from the same playbook. The thought process is, when the Federal Reserve changes rates, so will we. When they move, we all move. We all want to be profitable, maximizing income from arbitrage, so we keep our cost of funds (COF) low and price loans competitively.

If all financial institutions act the same, how are you supposed to stand out from the herd?

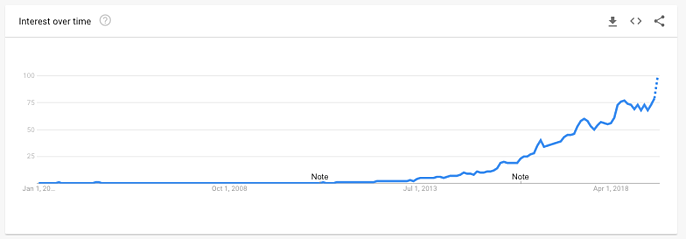

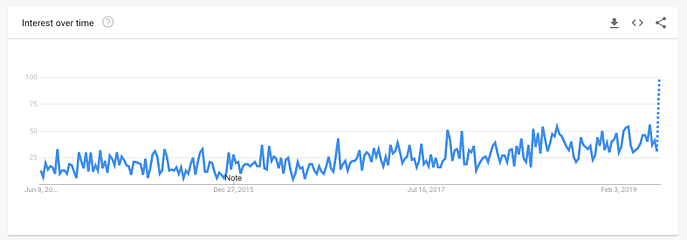

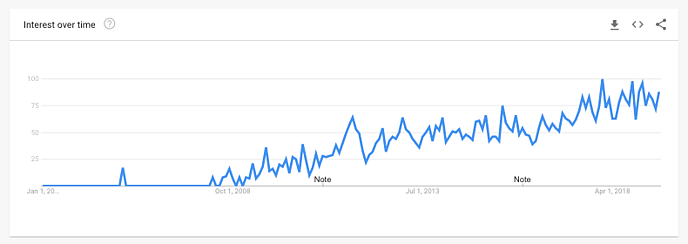

Looking at Google data, you can see that consumers are increasingly trying to apply the filters in order to find an account that is different.

Here's a search for "banks near me."

"High interest checking"

"Best bank app"

These and other modified searches have grown steadily since 2015. When one institution gains a brief moment of differentiation, another moves quickly to fill the now-exposed gap. You might be known for service, but if a consumer says, "The bank across the street has better rates," how would you respond?

This fixing of deficits makes sense on the surface, but it makes every institution look more the same. Not different.

Mapping Your Value

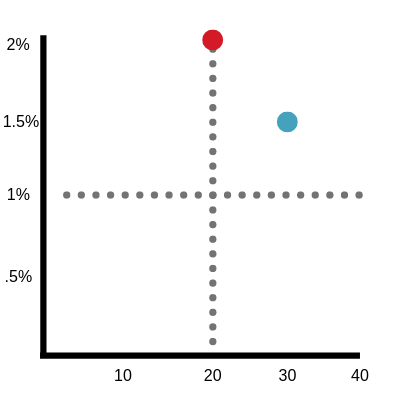

Consider a standard tool of product marketers: the value matrix. For the sake of simplicity, we will distill checking accounts down to two features: APY and the number of ATMs in a geographical area. Your institution offers 2%, whereas your competitor offers 1.5%. Your institution has 20 ATMs, but your competitor has 30. You (the red dot) have better rates, they (the blue dot) are more convenient.

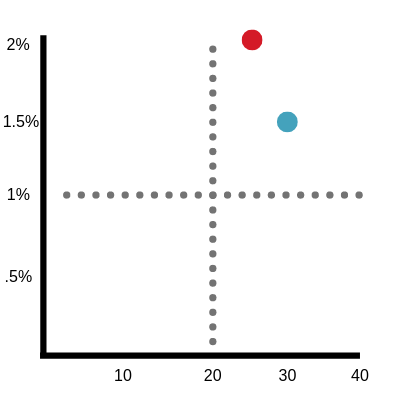

To increase your competitiveness you expand your ATM footprint to 25 ATMs. Redrawing the value matrix -- are you closer (more similar) or further (more different) from your competitor.

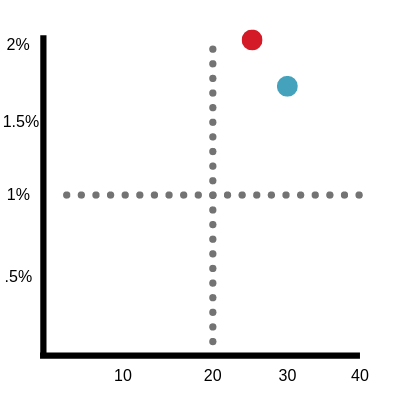

And, of course, their customers are mentioning how you have better rates, so they move their rate to 1.75%. The gap narrows. You are basically indistinguishable from your competitor to everyone except the savviest consumer.

With the use of credit cards and the availability of cash-back, ATM availability holds decreasing value for some consumers. So, while you are now more similar to your competitor, you invested in a feature that your consumers may or may not think is valuable.

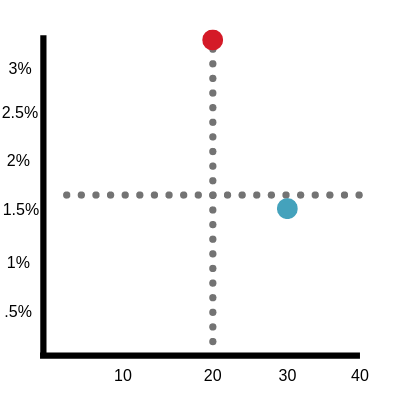

Consider what happens when you don't fix your deficit, but instead, you further your advantage. You look at the data and see that most of your consumers actually don't use ATMs very often, so you don't touch your ATM network. Instead, you focus on where you are strong and raise your rates to 3%. If we redraw the value matrix, the distance from your competitor has increased. Now your differences are more obvious, which makes it easier for consumers to choose.

Now you own a segment. Your institution is the institution to turn to if a consumer cares about rates. Prospective account holders have something to weigh, and even those who thought they cared about ATM distribution might consider this better rate as more valuable.

The Power of Branded Features

If you want safety, you get a Toyota.

If you want electric, you get a Tesla.

If you want incredible engineering, you get a BMW.

All of these brands have similar features deployed in their vehicles, but they made it a strategic priority to make their brand synonymous with a point of differentiation. Consumers know which brand to turn to based on their needs and wants.

Taking Control

You might be rolling your eyes and asking a question about profitability. That is a conversation for another post, but suffice it to say that there are strategies to offer high-interest reward accounts without sacrificing profitability.