Picture your dream borrower. They might look something like this: a longstanding checking and savings account holder with an auto loan, mortgage, and credit card who always makes on-time payments for all three. Now, how many of your borrowers actually look like this?

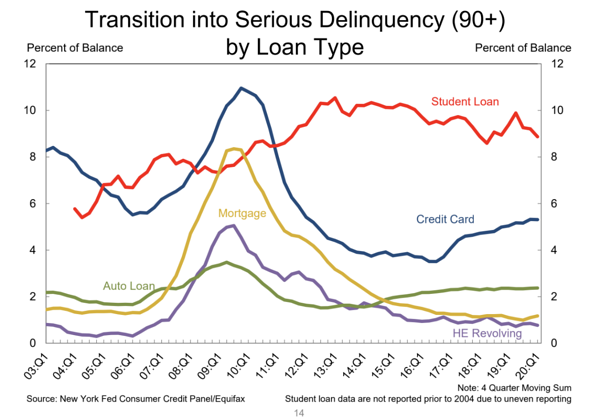

Unfortunately for many financial institutions, not every borrower is quite as engaged. Rising consumer debt has led to something no lender wants to deal with — borrowers making late payments, if any at all. According to the most recent Household Debt and Credit report, $652 billion of debt is currently delinquent.

Why are loan delinquencies on the rise?

Delinquency rates are on the rise for both younger and older consumers. For younger consumers, the reason could be a lack of financial experience and responsibility. Older consumers are facing something else entirely.

Consumers in the 50-69 age range typically have higher debt than their younger counterparts. At the same time, they’re entering a stage of life where job prospects are waning and medical expenses may be increasing. When forced to choose how to allocate their money, a loan or credit card payment often gets put on the backburner.

With 78% of Americans living paycheck to paycheck, this type of decision-making happens all too often. And since loans haven’t changed since the age of the dodo bird, there’s little help consumers can find in the product itself.

Financial institutions (and consumers) need a better lending product.

It’s time for loans to evolve. Better serving consumers and preventing loan delinquencies boils down to convenience, flexibility, and engagement — three things that traditional loans don’t quite deliver on. In order to see happier, more engaged borrowers, financial institutions need to offer loan products that do these three things:

1. Encourage Auto Pay

Last year, we talked about how Auto Pay can reduce risk in your loan portfolio. Many financial institutions offer borrowers an incentive for signing up for Auto Pay, like a rate discount. But what if the loan product itself encouraged more engagement from the borrower, so that signing up for Auto Pay were a natural step in getting the loan versus something a borrower had to be coaxed into?

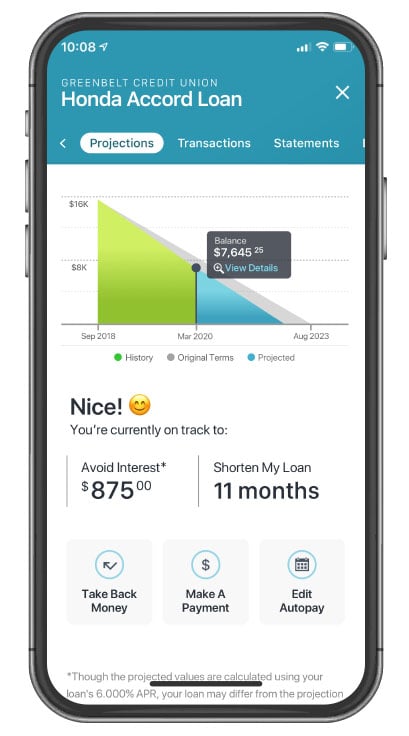

Kasasa Loans® have been shown to increase Auto Pay adoption — which is industry proven to reduce delinquency. In fact, performance data for the Kasasa Loan shows that 75% of borrowers enroll in Auto Pay without needing any discount. Why would borrowers be so willing to sign up for an automatic withdrawal from their account every month? See point number two.

2. Offer payment flexibility

We know that many consumers put off paying their loans because they may have unexpected needs arise (e.g. a hospital visit, job loss, etc.). A key component of a loan that borrowers would actually want to pay is flexibility within the payment itself. And we’re not just talking about one-time, skip-a-pay specials. We’re talking about completely eliminating a borrower’s payment paralysis.

Kasasa Loans offer Take-Backs™, which gives borrowers the ability to pay ahead and withdraw those funds whenever needed, for whatever reason. With Take-Backs, a borrower doesn’t have to be afraid to sign up for Auto Pay or pay a little extra on their loan. They’ll have access to those funds later, if they need them.

3. Facilitate ongoing engagement

Building relationships with your borrowers is vital to keeping them engaged and paying their loan too. Think about this: the rising auto loan delinquencies in 2019 were specifically for indirect auto loans. Presumably, borrowers who finance their vehicle directly at the car dealership have little to no relationship with the financial institution issuing the loan, other than making the payment once a month.

That’s where the problem lies. An unengaged borrower facing financial difficulties will have no qualms about pushing their loan with you aside to prioritize other expenses.

Even when a relationship can’t be built during the application process, as is the case with indirect lending, the loan product itself can offer ongoing engagement. A sleek, mobile-ready payment process is a must. And Kasasa Loans take that a step further with a digital dashboard that’s not only interactive for the consumer, but, dare we say it, fun.

Loan delinquencies are the symptom of a bigger problem. For financial institutions to truly engage with their borrowers and lower the risk of delinquencies within their loan portfolios, they must offer an innovative lending product. One that improves upon the rigidity of traditional loans and offers consumers the flexibility they need to manage all of their debt.