What you’re about to read in this article should concern you. The timing is pivotal. How you choose to adapt over the next 12 months will absolutely determine your success over the next five years. But first, we need to take a short walk down memory lane.

There’s an oft-referenced historical moment when many of us like to think we could see the writing on the wall: June 2004. This was when Blockbuster’s stock had fallen to $15 a share, half of what it was just two years earlier. But at that moment, plenty of people saw Blockbuster’s historical dominance as evidence that it could still recover. In reality, the stock had a few more “mini-rallies,” but it never even crossed the $11 threshold again.

OK, now let’s examine what’s happening in the world of community banks and credit unions.

First, here’s some good news for our industry.

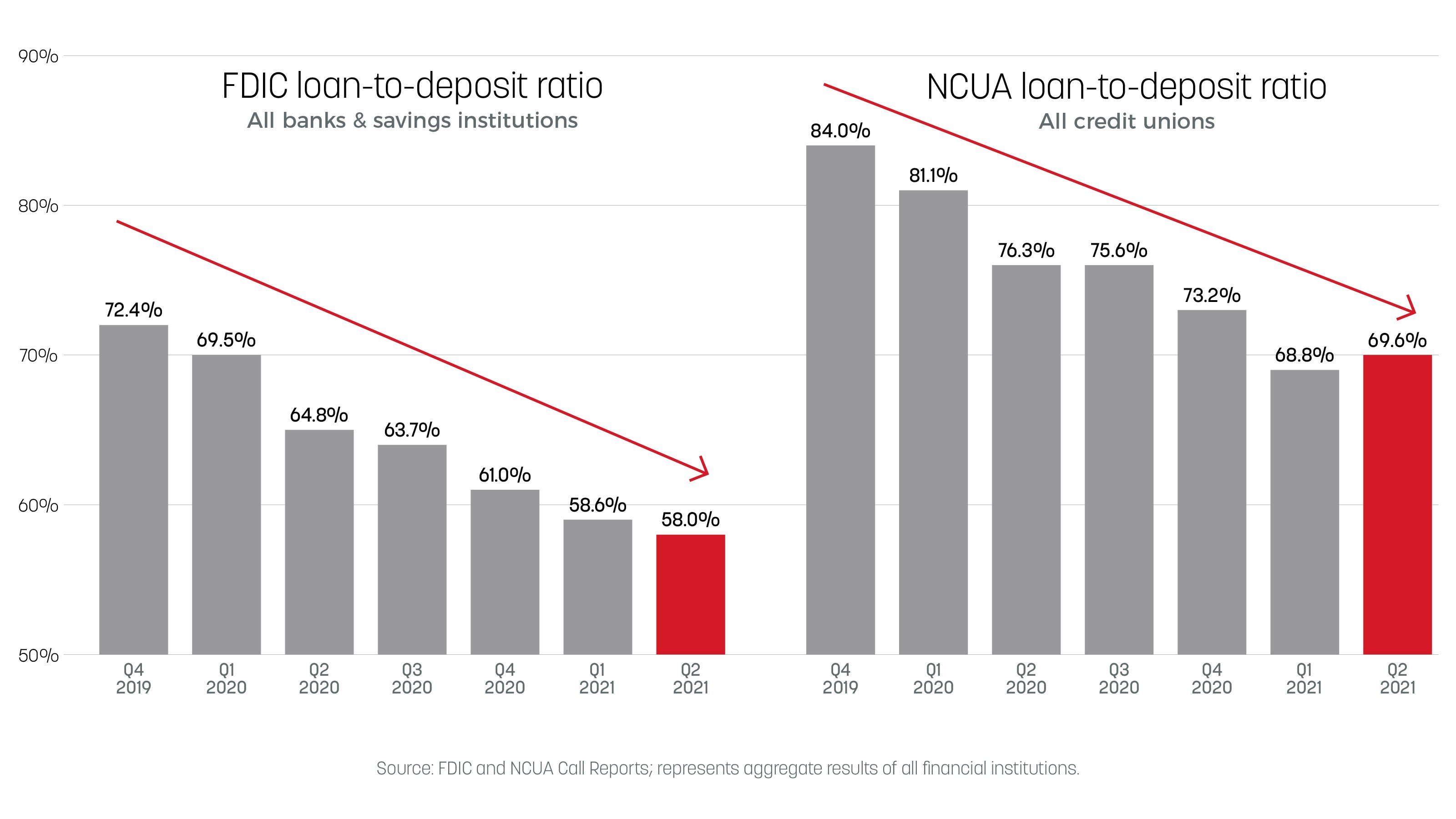

Consumer lending portfolios are showing some bright spots. And the 25- to 34-year-old cohort comprises 46 million people in their prime credit building years. The result appears to be a flattening out of loan-to-deposit ratios, which could signal a new trend of loan growth.

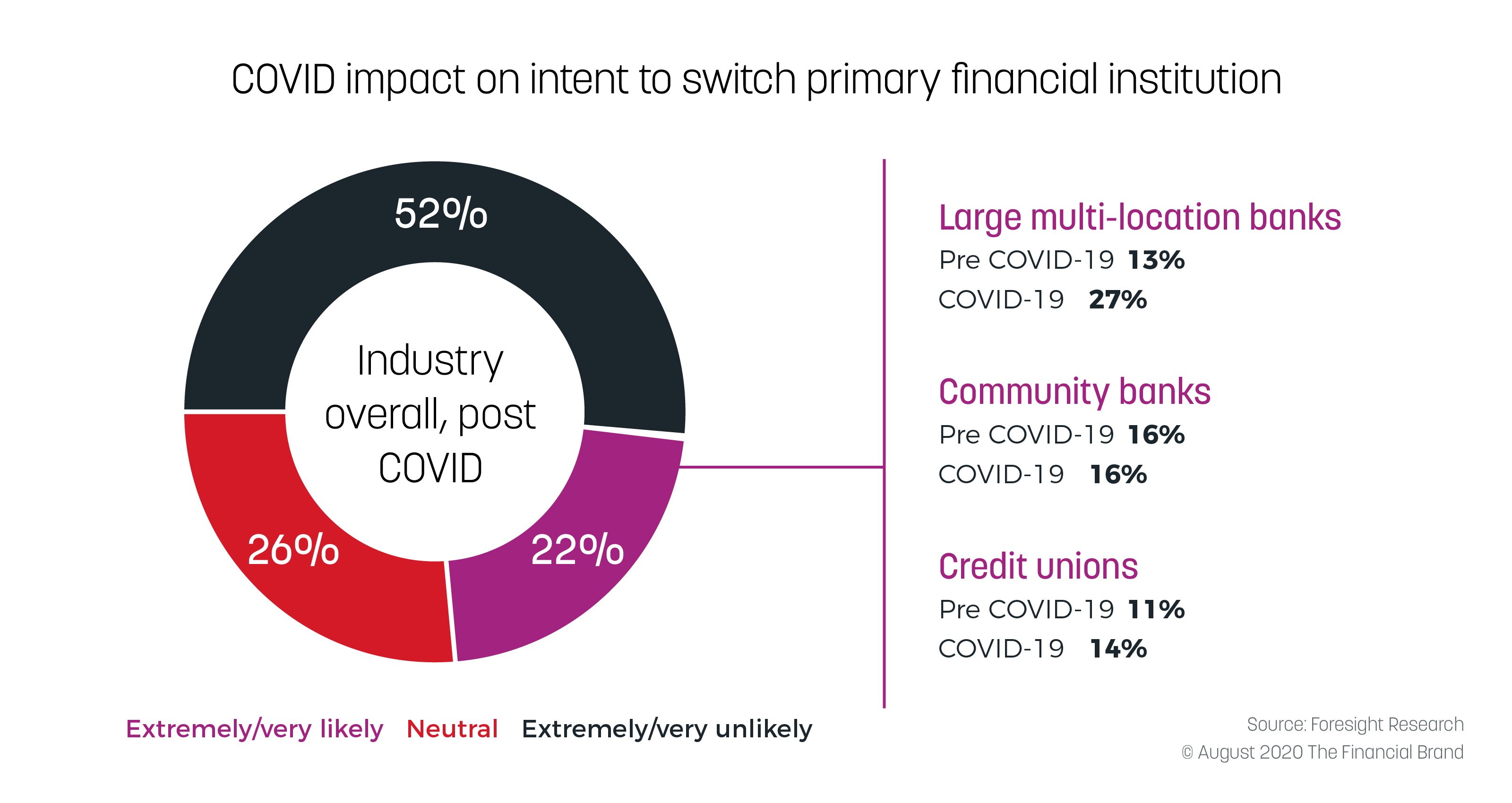

The pandemic has propelled consumers away from large banks in search of a better experience. Your institution has an opportunity to reach these consumers with the promise of better service and comparable products. What you need is a strong marketing strategy and the determination to keep marketing when others are hesitating.

The time to act is now, and tomorrow, and every day after.

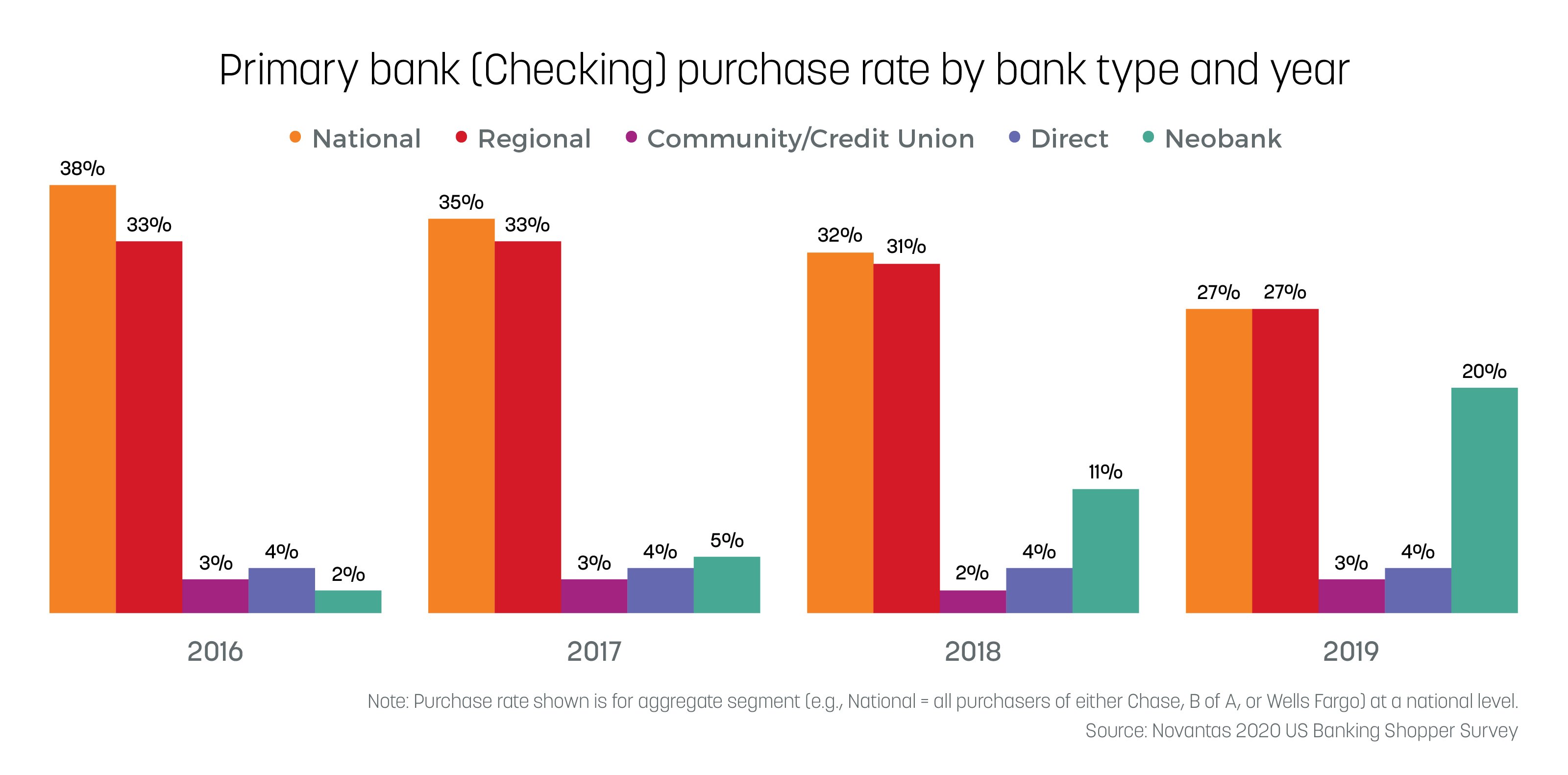

Kasasa has been warning our industry about the threat of neobanks for at least a decade. And it’s no longer a “when” or an “if.” The neobanks have established their beachhead and are mounting a full-scale invasion of the banking and payments systems.

Consumers may be ready to leave megabanks, but they’re clearly happy to adopt neobanks as their primary financial institutions. If you want to be in the consideration set, you must make aggressive moves with your products, services, marketing, and in your mindset.

The latest “front” in this battle is NSF fee income, something we covered in a recent blog. Capital One’s decision to eliminate NSF fees is a high visibility move that will garner a lot of positive press and push competitors to keep up. That puts many community financial institutions (CFIs) in a bad spot. Margins have compressed to slivers, and the historical rate of loan growth isn’t fast enough to provide the necessary revenue.

Thankfully, there are clear steps you can take to move your institution forward. You don’t have to cede ground to the neobanks or whichever competitor you’re fighting for market share.

Play to win, play to your strengths.

Community financial institutions have an advantage. Your branch locations allow you to have better, more engaged conversations about your products and services. You have a name and a face for anyone living or working nearby. The neobanks will barely allow you to reach a real human being by telephone. Their digital “imperson-ality” is only sufficient when everything works like it’s supposed to, but we all know that when somebody has a money problem, they want real help from a real human, right now!

The secret to uncovering opportunities is two-fold: To use a baseball metaphor, you need to increase your team’s “at-bats” and your skill at swinging. For CFIs, this means you need to expand your retail product offerings with products that consumers want (i.e., your “at-bats”) and your marketing effectiveness (i.e., how hard and accurate you swing the bat). By focusing on the right retail portfolio and building strong relationships you can reduce your institution’s reliance on NSF fee income by increasing the number of products per household. More aggressive, targeted marketing also has a cumulative effect. Over time, the more visible your institution is, and the more aware people are of your products, the more likely they are to choose you for their financial needs. It’s a virtuous cycle that starts slow, but it generates huge momentum when you commit to it.

Stay agile, use what you have, pivot.

Product penetration works well as a proxy for relationship depth — more products per household translates to more engaged, more loyal account holders. But how do you know which products to offer and how to market them? I know a lot of CFIs are stretched thin as it is, so the idea of spinning up a bunch of new products and marketing campaigns can sound… monumental.

Trust me, from my years working with CFIs, I’ve seen how tough that situation is. I wouldn’t be addressing this so strongly if I didn’t believe that there’s hope. Look for partners who can help you offer products that consumers want and that help you achieve your goals. You’ll also need partners who can help you execute marketing programs with sophisticated targeting.

Touching back on my Blockbuster point from the start of the article: You will not gain any ground on your competition if you keep doing exactly what you’ve been doing. Give consumers as many reasons as you can to trust you with their financial lives. Adapting to the current environment doesn’t mean losing the values you’ve stood by for decades. It means reimagining what those values mean for today’s consumers.

You can do this. It’s too late for Blockbuster — they could have partnered with Netflix and they said “no”. Now they’re an object lesson in business disruption. The moment is ripe for you to move boldly into the new era. Don't miss it.