In “Forrest Gump” the main character, for whom the movie is titled, offers chocolate to a stranger and recalls a piece of wisdom from his mother: “Life is like a box of chocolates, you never know what you are gonna get.”

But today we’re talking about the world of banking, so let’s reframe the statement as, “Fees are like a box of chocolate-covered marzipan: not a pleasant surprise for any consumer.”

Even the restatement borders on cliché, yet it illustrates the important role expectations play... in banking as well as in life. And notice that the operative word in the previous sentence is “surprise.”

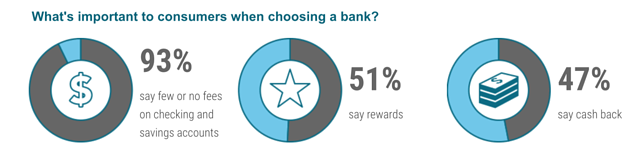

Let's take a look at how consumer expectations influence their relationship with their financial institution. We'll start with the obvious: In a recent study, 93% of account holders ages 18 and up said few or no fees was important to them when selecting a financial institution. Most fees can be classified in two ways:

1. Fees That Are Highly Itemized

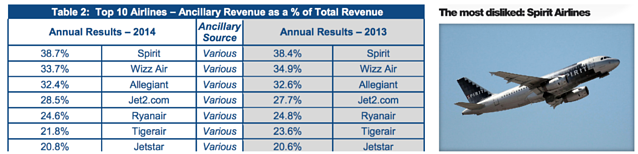

The benefit of the itemized approach is that it allows the consumer to pay only for the services they want or need. The downside is that it can leave consumers feeling nickeled and dimed. Spirit Airlines is an example: some travelers love the cheap fares and embrace the “travel light” ethos — other travelers feel cheated by paying for things other airlines include in the ticket price (carry-on baggage, printing out your boarding pass, drinks). You can see the consumer response by looking at two studies; CBS News found that Spirit was the "most disliked airline" and IdeaWorksCompany found that Spirit Airlines had the highest fee-driven ancillary revenue. Coincidence?

2. Fees That Are Bundled

Southwest Airlines has taken the opposite approach and bucked the itemizing trend in the industry by leveraging their “Bags Fly Free” policy. When you do the math and compare the cost of checking two bags with another airline, the total cost can be surprisingly close. Do you always need to check two bags? Nope. Is it nice to know that you don’t have to worry about a baggage fee if you change your mind at the last minute? Yup. (Oh, and by the way, they ranked as America's favorite airline in the study referenced above.)

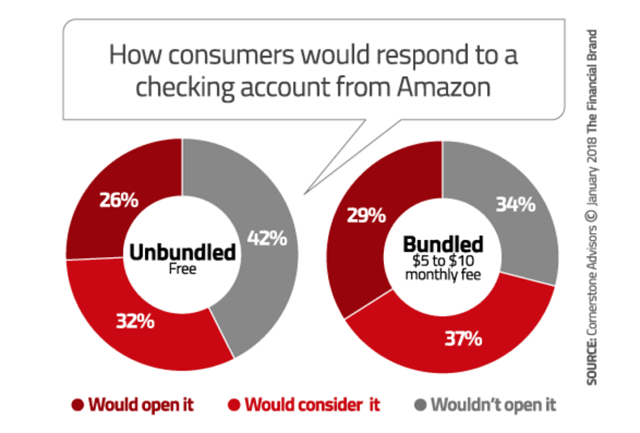

When a business decides to bundle their fees, they are certainly building their costs into the total, but they are doing so in a way that also increases the perceived value. Bundling fees creates a change in the consumer's thinking from "Oh, another thing to pay for!" to "Wow, look at all value I get!" This mental switch is illustrated in the results of a study conducted by Cornerstone Advisors on consumer appetite for an Amazon banking product.

The bundled package with a monthly fee was actually more attractive to consumers than a free account with no added value.

You Can Help Consumers to Feel Good About What They Pay For

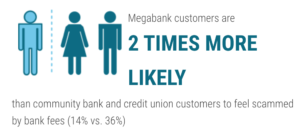

In many cases, the total cost to the consumer may be similar in both itemized and bundled scenarios, but how consumers feel is likely to be as different as night and day. Our research found that 36% of consumers who are charged fees at megabanks report feeling scammed, and 41% of millennials would switch institutions just to avoid fees.

To illustrate the impact of fees on consumer trust, let's look at the high-profile case of Netflix vs. Blockbuster: At its peak, Blockbuster earned $800 million in late fees. Netflix has never charged a late fee. Keep the discs as long as you want, just pay your monthly subscription fee. How much money did the average Blockbuster customer spend on rentals and late fees in a year? It stands to reason that it probably wasn’t far off from a year’s worth of Netflix. And while Netflix has raised their prices over the years, the only time they ever truly upset their customers was when they attempted to split their video streaming and DVD rental businesses. (Remember Qwikster? Thanks to public outcry and corporate humility, nobody else does either.) The creation of Qwikster would have required people to (surprise!) pay for two separate subscriptions instead of one.

Three Rules for Charging Fees That Don’t Leave Account Holders Feeling Bitter

What’s the lesson for community financial institutions? Be careful what you charge for. While certain fees, such as NSF and investment fees, have a transparent logic to them, other fees create consternation. (Just ask Bank of America about their new $12 monthly maintenance fees.) To earn the goodwill of your account holders, you must observe three rules:

1. Be Transparent

Explain what the fee is for and why it’s necessary. If you write out the explanation and don’t feel good about it, consider waiving or bundling it. Sticking with our box-of-chocolate analogy, this would be charging a "chocolate wrapping fee" after buying the box. Consumers don't mind paying for their services but they do feel cheated when you pass along expected costs of operations in the form of a fee (like passing of your electric bill as an "Energy Recovery Fee").

It's important to remember there is a difference between writing and communicating an idea. Part of transparency means putting the reasons for the fee in understandable language. Yes, you might need to include the conditions of the fee in legalese somewhere, but make sure to take the time to clarify the fee in terms the consumer will understand.

2. Limit Fee Schedules

Take a quick look at a megabank fee schedule. It’s huge and complicated. It’s a virtual box of melted chocolates. You have the opportunity to create simple fee schedules and make them easy to access. You can even use them to start conversations about how your institution works hard to keep fees to a minimum — this level of honesty builds trust.

3. Reward Good Behavior

Another way to build trust and partnership is to reward consumers for doing the right thing (such as using their debit card, taking e-statements, and setting up direct deposit). The adage of "You can catch more flies with honey than vinegar" translates nicely to the banking world. Consumers will be attracted to institutions that take the position of a financial partner over ones that act as a disciplinarian; Reward the good behaviors instead of punishing the bad. In parenting, this is known as positive reinforcement — in the world of community financial institutions, it’s known as being awesome.

Staying Profitable Without Fees

The evidence is clear (and kind of obvious): consumers hate fees. Businesses, however, recognize fees as a means to increase revenue. After all, Blockbuster and Spirit made more than 30% of their revenue from fees...

But at what cost? We've seen that relying so heavily on fees is a risky proposition that primes your institution for disruption. A new business simply needs to offer more perceived value to win your market share. So, how can you stay profitable and still cut fees?

You might have already noticed the answers: bundle services and grow non-interest income.

Being rewarded to change behavior is much more palatable to consumers than being charged fees, especially when it creates win-win scenarios. As an institution, you can incentivize consumers to adopt money-saving behavior (moving to digital banking only) and drive non-interest income (debit card swipes). As we explored above, consumers are actively seeking these kinds of partnership relationships with their financial institution. Once this is established, it opens the door for upselling. Consumers are willing to pay for monthly fees on an account they feel the value delivered above the fee they are paying, specifically ones that help them feel more in control of their finances.

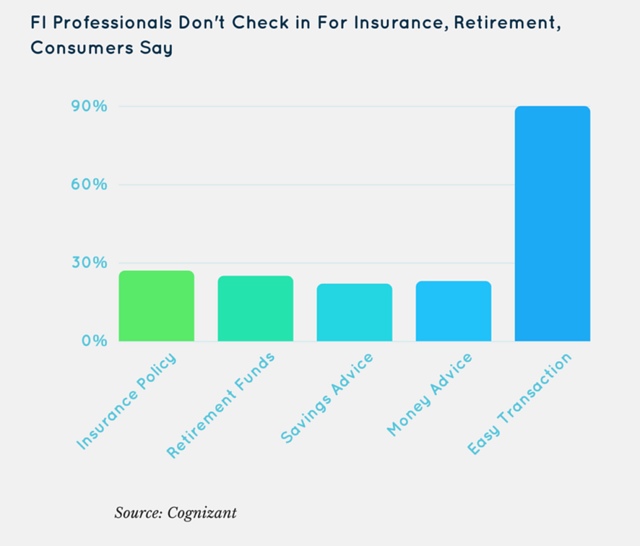

Cognizant found that financial concerns are the number one stressor in adult's lives and that these adults are actively looking for guidance and products from their financial institutions. However, most institutions are only offering services for "easy transactions." This means you are leaving a lot of revenue and trust on the table.

Want to learn how Kasasa can help drive more NII, increase upsells, and help you build deeper relationships with your consumers? Request a demo, we'll be happy to walk you through how we can work with your institution.