Does your CD rate make you shake your head every time you see it? You’re definitely not alone. Big names have entered the playing field that weren’t there 5 years ago. They’ve got massive capital behind them and they’re snatching up consumers left and right. In fact, 46% of new accounts were opened at fin techs in 2023. If you want consumers and deposits, you’re going to have to fight for them.

Expensive money.

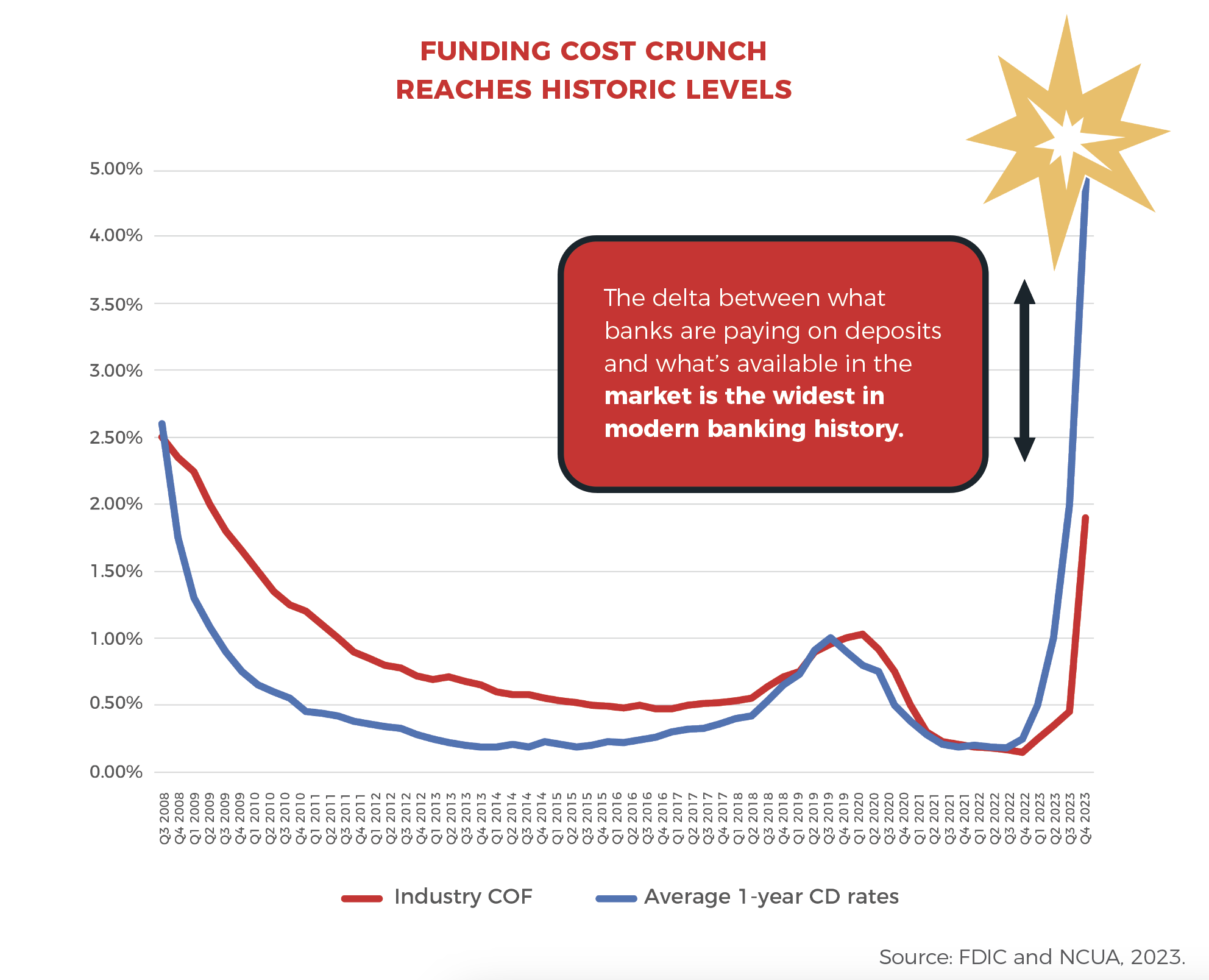

Growing deposits is a BIG issue for CFIs across the country right now. The traditional route of using CDs to bring in deposits has made the process unbearably, if not dangerously, expensive. And there are no signs of this trend slowing down. In the last 20 years as the industry Cost Of Funds (COF) has risen and fallen, the 1-year CD rate has moved in lockstep with the industry COF. However, that’s not happening today, and the industry COF and average CD rate have never been further apart.

As shown in Diagram A, there’s a correlation that’s been very consistent at least as far back as the big financial crisis of 2008; for most institutions, the cost of the dollars they currently have and the cost of a new dollar out of the marketplace (a one-year CD) have been very similar. In fact, most of the time the current cost is actually higher. Recently, those lines have started to diverge, and the replacement cost has become dramatically higher. Losing a consumer is now more expensive than it has ever been in modern history.

<Diagram A: Funding cost crunch reaching historic levels.>

A lot of financial institutions have seen fluctuations in their deposits due to this liquidity crisis. They are caught in the middle trying to aggressively raise funds and at a much higher cost. Traditional funding methods like CDs often lead to unsustainable funding costs, high attrition, rate shoppers, constant repricing, ongoing liquidity struggles, and more. This is what’s known as phantom growth. New deposit strategies are required to create real growth in order to thrive in this financial environment.

So how can you create real growth?

The race for deposits is more aggressive than it’s ever been. If you want to compete, you have to find ways to bring in deposits at a lower cost. High-yield checking allows you to leverage a built-in COF discount that can significantly lower your annual expense. Using this strategy allows you to grow strategically significant core deposits at an average all-in cost of 2%.

The ideal consumers are local, core deposit account holders who are engaged. While deposits and low-cost liquidity are important, institutions also want a relationship that stays longer and adds more products. CDs can lock a consumer in for a couple of years, but because they’re rate-sensitive, they’re also likely to leave after that term is up in search of a better rate.

High-yield checking account holders, on the other hand, tend to be much more engaged and more prone to exhibit behaviors that can lead to primary financial institution relationships, and create additional income opportunities.

New challenges call for new strategies.

Mid-term, rate-sensitive instruments such as CDs may have worked in other eras, but today’s unprecedented circumstances call for a very different approach. Growing low-cost core deposits is a must to survive. Taking a closer look at the advantages of high-yield checking accounts — and their unique COF discount — could be a key strategy to slowing the increase in Cost Of Funds and bringing in real deposits, real margin, and real engagement.

1FDIC/NCUA Q1 2023 data compared to Q4 data, comparing Kasasa partners to non-Kasasa partners.