Here's when (and when not) to auto refi, and how refinancing your auto loan today can help you roll into 2022 with a clearer, faster path to debt-free.

The last year has been a brutal time to buy a car, from the early days of pandemic uncertainty to the current wave of supply chain issues and crucial chip shortages. A reduced supply of new cars has drastically increased demand, which has driven prices way up. Nevertheless, we estimate 25 million people in the United States bought a car with an auto loan in 2021, covering this rising cost by taking it on as debt.

If you’re one of those 25 million — or if you’re just stuck in a bad auto loan — you can still get your financial picture in focus by refinancing your car loan. As we turn the corner on a long year, you’d be wise to consider the reasons why it’s an especially good time to auto refi today.

Maybe you’re slogging through your first auto loan, your car payment is too high, and you want to get a better deal. Or maybe you can get a more favorable interest rate now than you have on your current auto loan, meaning you will save money. Perhaps you just want to ditch the megabank that issued your current loan and pursue auto refinance with a new lender.

For many reasons, right now might be the BEST time for you to refinance your auto loan. Here's when (and when not) to auto refi, and how refinancing your auto loan today can help you roll into 2022 with a clearer, faster path to debt freedom.

Rule of thumb of when to refinance a car loan: three key signs

Let’s review some auto refi basics. We’ve previously covered three major signs that it’s time to refinance:

-

Interest rates are lower. This is always a good rule of thumb for refinancing, but for various historical reasons, right now the federal interest rate is at a historical low. What does that mean for your auto loan? The short version is that now is an especially good time to pursue auto loan refinancing. Those same super low rates won’t last forever, so get on it!

-

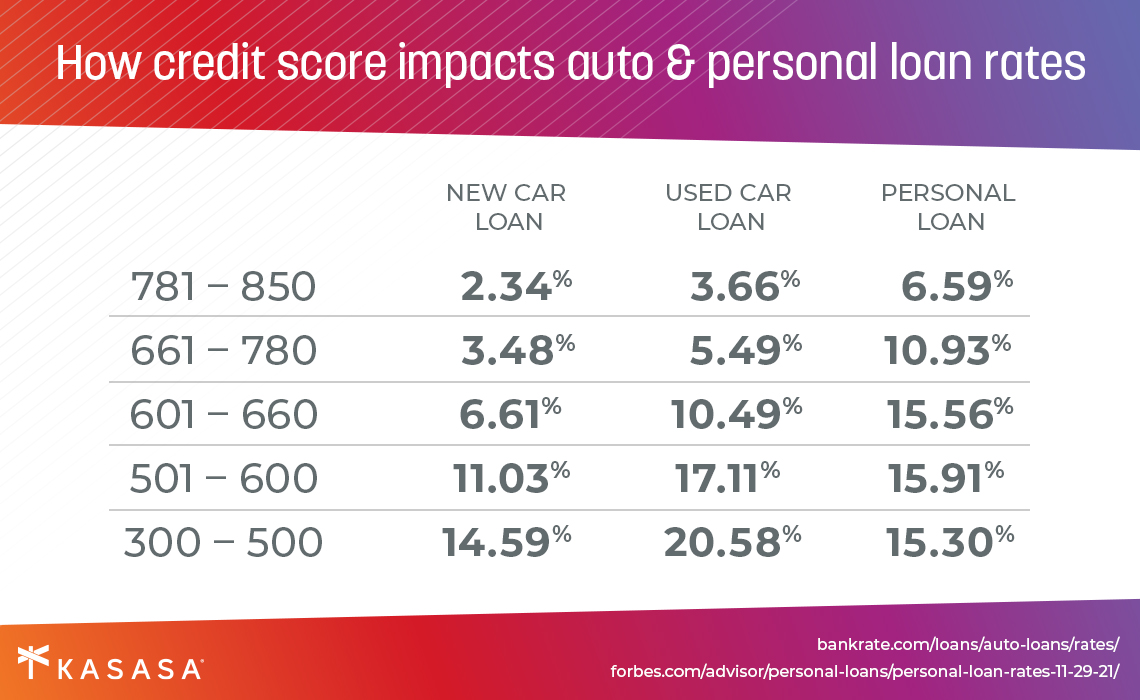

Your credit score has improved. This is another straightforward reason to refinance. Any lender will in large part base their loan offer (and interest rate) on your credit score. The better your credit score, the better rate you’ll be offered. If your score has shot up since you took out your first auto loan because you’ve been making your payments on time (congrats!), now’s a good time to look into auto loan refinancing. If not, check out these five tips to improve your credit score before taking out a loan.

-

Your credit file is thicker. This might seem like the same thing as your credit score, but it’s not. Your credit file is basically your long-term history of repaying debt, from your credit cards to your student loans, to your home loan, to your auto loan, to any other kind of loan. If you’re in your first auto loan, it’s likely that your credit file is “thin,” which from a lender’s perspective means there’s not enough data to verify that you can reliably pay back your loan over X number of years. You can’t just refinance your auto loan immediately. However, consistently hitting your repayments gradually adds credit history to your file (while improving your credit score). If you’re a first-timer, try looking into auto refinancing around the 12- or 18-month-mark. If it’s not your first time around the block, you can pursue auto refi as early as 6 months after taking out the initial auto loan

Is car loan refinancing right for you?

Let’s zoom out for a minute. Auto refinancing isn’t for everyone. As was just mentioned, you can’t refinance your auto loan if you just took one out less than six months ago (or less than a year ago, if you’re a newbie).

To reiterate another key point: Credit score significantly impacts your auto loan rate. Any bank or credit union will decide whether or not to offer you a loan based on your credit history and current financial situation. If your credit score is lower now than it was when you originally financed your car, you’ll probably get a worse offer now — best to hold off (and here are 11 more ways to improve your credit score in the meantime). Auto refinancing can even hurt your credit, though usually this is just a blip that goes away after you start making payments on the loan on time.

You might be motivated to refinance because you needed a cosigner when you took out your original loan, but are a bit more financially stable now and want to go it alone. Unfortunately, you may not get a better rate on a refinanced auto loan when going solo, even if your personal credit score has improved.

Refinancing can also affect your car insurance premium — sometimes saving you money, sometimes costing you a bit extra. Your mileage may vary on this one; consult your car insurance provider for more info.

How to get started with auto refinancing today

If you’ve weighed these factors, understand the refinance costs, and have decided to hit the gas on auto refi, your first step is to goal-set. Do you want a lower monthly auto payment? To pay less during the total life of your auto loan? Or do you just want to get your auto debt in the rearview mirror as quickly as possible?

Depending on your answers, decide if you want to change your loan term (aka the repayment timeline), and if you want to decrease your monthly auto bill, or increase it in order to pay down your loan faster.

Armed with that knowledge, you’re ready to approach a lending financial institution — aka a bank or credit union — with your ID and vehicle info. The bank or credit union will want to know details about the car you’re refinancing, so have the make, model, VIN number, and mileage on hand. You’ll also need to have a valid driver’s license. Anything you can provide as financial background — paystubs from your employer, or evidence of a fixed address — can also help you get a better rate during the auto refinancing loan application process.

Refinance with the Kasasa Loan® — the only loan with Take-Backs™!

The Kasasa Loan® is a new kind of loan that arms community financial institutions with the tech-forward tools they need to reach people like you: Informed and ready to borrow smarter. Kasasa® is the only financial tech (aka fintech) company whose mission, for nearly 20 years, has been to help community financial institutions survive — and thrive. The Kasasa Loan is the only auto refinancing loan with Take-Backs™, a unique feature that lets you pay ahead to get out of debt faster, but still have access to those extra funds when you need them.

In our opinion, the best auto refinance loans are the ones that support you and your community. Credit union auto refinanced car loans, or loans offered by small community banks, offer you a lot more than just potentially better rates.

When you take out an auto refi loan with a community financial institution, you get to reset your entire auto financing experience. This feels especially good if you got a lousy original loan from a car dealer, or are ready to ditch the impersonal megabank experience and cast your financial lot in with a community-oriented bank or credit union.

If you’ve read this far, it's likely you’re ready to get out of your bad auto loan and into something more your speed. Check out the Kasasa Loan today!