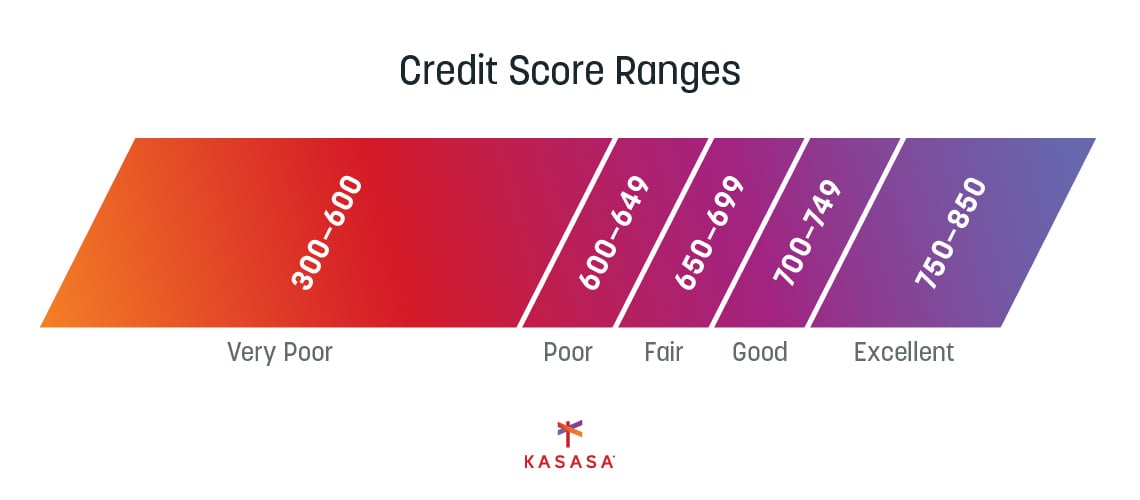

Keep your credit score is in good shape before you apply for a loan with five ways you can keep tabs on your credit report and track your credit score.

Your credit score is the most important factor in determining the interest rate you receive on a loan. You may have been working to improve your credit score for months or even years. Even just one-half of a percent difference in the interest rate could save you thousands over the term of the loan.

It might feel like how the score is calculated is out of your hands, and that it fluctuates every month, even when you are making payments on your existing debt and being attentive to your personal finance changes. In actuality, while all that matters, there are many other factors. Everything from your credit utilization ratio to your credit mix work together to come up with that all-important number. In the end, taking the time to make sure your score is as high as possible can help save you a lot of money —and that's what is important when you are considering a new loan.

So, how can you make sure your credit score is in good shape before you apply for a loan? Here are five ways you can keep tabs on your entire credit report and track the movement of your credit score.

1. Get your credit report and check it for errors

1. Get your credit report and check it for errors

Your to-do list may read "improve credit score," but you can't change what you don't know. The first step in garnering a higher credit score is to know everything in your credit history.

You will want to review the information for accuracy, so start by making sure every item on your credit report is yours. Mistakes that appear as bad credit on a consumer's reports are shockingly common.

The Federal Trade Commission conducted a study that showed one in five consumers had at least one error impacting their otherwise good credit reports from one credit reporting agency. This means there is a decent chance you may have a mistake on your report that is hurting your score. It may seem small, but as many as 33% of consumers saw an increase in their FICO credit score when the error was corrected. A little legwork can lift you to a good credit score, or help you build up to an excellent credit rating.

Go through your credit history closely and make sure there are no accounts you don't recognize. Also review your payment history. If you do find mistakes, you can contact the credit bureau where you find the error to dispute the information (phone numbers and online contact links below). Some common reasons to dispute a line on your credit score include:

-

Someone opened an account in your name

-

One of your existing accounts was stolen

-

A bank, collection agency, or vendor made an error

They have 30 days to investigate the dispute. Here are the websites and phone numbers for each of the three credit bureaus:

-

Equifax 888.548.7878

-

Experian 888.397.3742

-

TransUnion 800.916.8800

2. Sign up for free credit monitoring

In addition to the free annual credit report you can receive from all three major credit bureau companies, there are other easy ways to keep current with your changing credit score. Companies like Experian and Credit Karma offer free services that let you regularly track changes to your credit score and updates to your credit report.

These companies offer free credit monitoring that alerts you each time there is a change in your credit score, a new credit inquiry, new accounts, or anything else that impacts your credit score. This can be an action of yours, like paying down a loan, or an error to your credit report, like a fraudster opening an account with a credit card company using your information. Being aware of these changes helps you keep tabs on your credit report.

(Note: You may receive assorted credit card account and personal loan offers as part of your enrollment. Resist the temptation to jump into a loan without doing a bit of Lending 101 homework.)

Sometimes a late payment or past negative action sent to the credit reporting agency may affect your credit report. It can take time to fix those credit history hiccups. Here is a list of items that will hurt your score, and how long they remain on your credit report:

-

Late/Missed payments: 7 years

-

Bankruptcies: 7 years for completed Chapter 13 bankruptcies and 10 years for Chapter 7 bankruptcies

-

Foreclosures: 7 years

-

Collections: ~7 years, depending upon the age of the debt

-

Public record: ~7 years; unpaid tax liens can remain indefinitely

What's important about these time periods is to keep in mind when they’ll drop off your credit report. If they don't, and you know they are past their expiration date, contact the major credit bureau in question and get the adverse action removed. Just like an error or a fraudulent use of your credit information, it can take your effort to fix the bad credit. It's in your control to get those past issues resolved.

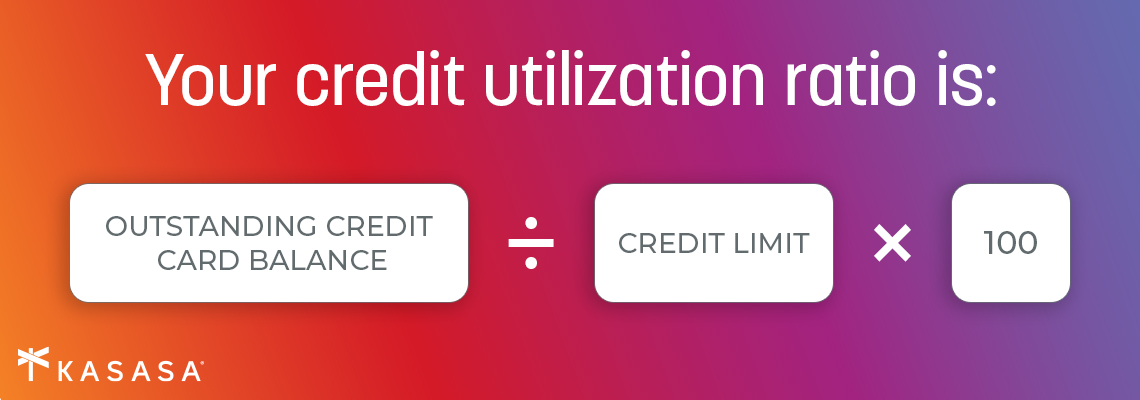

3. Keep your credit utilization ratio below 20%

Your credit utilization ratio is the amount of credit card debt you have, divided by your credit limit. Basically, the higher your balances are, the lower your score will be. Your total available credit will compare to how much of the available credit you're using. Keeping your debt below 20% of your credit limit will maximize your credit rating when a lender pulls your credit, so you'll get the best rate possible.

It’s also important to have a diverse credit mix. If all your debt is in revolving debt, such as credit cards, that may not look great to a credit bureau, since you can run up your credit ratio with a handful of big purchases. An installment loan, like an auto loan or a personal loan with scheduled payments and a final pay-down date, might provide the credit mix necessary to balance out your types of credit usage.

4. Have someone add you to their account

If you have a friend or family member with a credit card in good standing, ask if they will add you as an authorized user. An authorized user is someone who is authorized to use a credit account.

When the creditor does this, the entire account history will be added to your credit report. This helps by adding an additional credit line, but it also helps the average age of your open accounts, which makes up 15% of your FICO credit score.

The risk is minimal. You don't even need a physical card — you're just using it as credit repair, or to improve your credit score. This might be most helpful if you have a thin, or new, credit history to show your credit worthiness.

5. Contact collection companies

If you have any collection accounts on your report, they are significantly impacting your credit score. Fixing these is difficult; you might just have to wait seven years for the line to fall off of your credit report. What makes this issue more complicated is that there are two scoring models used: FICO 8 and FICO 9. With FICO 8, paying off the debt doesn't help your credit score; with FICO 9, it neutralizes it.

One option you have is to write a 'goodwill' letter. In it, you take responsibility for the issue and offer to settle the debt. At the end of the letter ask for a goodwill adjustment, effectively removing the negative line from your credit report. Keep in mind that they are under no obligation to do so. (In other words, be prepared for a "no.")

How to apply for a loan without hurting your credit

This deep dive before you apply for a loan will make the loan application process much cleaner. Once you begin the process of shopping around for a loan, there are a few tips that will help you minimize the impact of the credit inquiry.

Compare at least three different quotes to make sure you're getting a competitive rate. Keep in mind, if you are using a credit monitoring service that provides you with your current rate, it may not take into consideration the information from every major credit bureau.

Make sure to have lenders pull your credit within the 30-day rate shopping window. Multiple credit inquiries that may appear unrelated can negatively impact your credit score. All credit inquiries by the same type of lender within 30 days will count as one inquiry.

Avoid other credit offers once you begin the loan process. Even a simple credit card at a clothing store or when replacing your tires can affect your chances of getting the loan, or the interest rate, you've worked hard to earn.