The skinny on personal loans: no one type of loan fits everyone's need, but a personal loan may be the way to make purchases and manage debt responsibly.

Raise your hand if you've ever taken out a personal loan. ✋

That's a lot of hands. In fact, roughly $148 billion in personal debt is held in personal loans. If you're one of those people who raised your hand, you may already be familiar with some of the details about this type of loan, including what it can be used to finance or even personal loan rates.

If you didn't raise your hand — and a lot of you did not — you may not know much about personal loans. You may guess, and not incorrectly, that it's for a person, as opposed to a business loan. That's true, but an auto loan can be extended to a person or a business, so we'll clarify what counts as a personal loan in a moment.

The skinny on a personal loan is this: No one type of loan fits everyone's need, but a personal loan may be exactly what you need. Whether you are looking to buy a household appliance, consolidate debt, establish credit, or even take a vacation, personal loans may be the ideal way to make sizable purchases and manage your debt responsibly.

What makes a loan a personal loan?

From a non-banking, non-technical, and non-jargon-y perspective, every loan made to a person could theoretically be a personal loan. While that makes sense in the most simple terms, loans offered by banks, credit unions, and even faceless online websites offered to individuals, as opposed to businesses, fit into different loan categories. There are credit card loans, home equity loans, cash advances, vehicle loans, home loans, signature loans, and, yes, personal loans.

All of these types of loans are either secured or unsecured, which simply means there is a tangible object of value that secures, or backs up, the loan, or a loan is offered on good faith that it will be repaid with nothing backing up that promise other than the borrower's previous credit history.

A secured loan can be backed up with a car, a home, or even cash. In case the loan doesn't get paid, there is an object at stake for the lender to take back to cover the unpaid debt. Secured loans are a good loan option if you are just starting to build a credit history for yourself.

An unsecured loan, which includes most credit cards loans (yes, it's a loan even if you just call it by its more common nickname: credit card), signature loans, and personal loans don't have anything of value to pay back the financial institution if the loan goes unpaid. For example, if you an unsecured loan to pay for a vacation, no one is going to come and repossess your photos and souvenirs as payment.

A signature loan relies more heavily on your credit history, and these are often available to established account holders with a known track record at a financial institution. This is quite likely the opposite of a credit card loan, where the card company doesn't know you from Adam, or from every other of their millions of card holders.

Now that we've narrowed down what a personal loan is compared to other types of loans, let's look at when you might consider a personal loan.

Why would you want a personal loan?

There are myriad reasons you might want to take out a loan. Maybe you just want to make a sizable purchase. Consider where you may be in your financial journey to discover if a personal loan might move your personal finances forward.

Big-ticket purchase

Do you rent rather than own? If so, a home equity line of credit (also known as a personal line of credit) will not be an option until you both own your home and have made a dent in the principal. But you'd like to have a washer and dryer in your apartment since there are hook-ups and you are tired of hauling your laundry every week or two, not to mention all those quarters you could be putting towards the expense. A personal loan could help you make that purchase possible.

Establishing credit

You've just landed a promotion at your full-time job. You knew college wasn't a good fit given your plans and this opportunity is proving you have what it takes to succeed. You've never borrowed money, so your credit history is thin. With this promotion, you can afford to buy a new car in a couple years, but without any credit history, good or bad, it will be tough to get a good interest rate on a car loan. A personal loan to purchase some new tools may allow you to buy yourself some gear and establish good credit.

Travel

Your best friend from college is getting married this summer. Of course, you want to travel for the wedding, plus you will want to buy an item or two from the gift registry. Once she asks you to be one of her bridesmaids, you know this is going to be a bit of a stretch for your budget between now and the wedding. Plus, there's always the likelihood of an unexpected expense from now until she walks down the aisle, such as bridal showers and bachelorette parties. Getting a personal loan may allow you to start paying now and continue paying over a two-year span so you aren't hit with all these expenses in the next six months.

Debt consolidation

You remember bringing your first credit card to the clothing store at the mall. In college you opened your first "real" credit card and you've been great about paying it all the way down every few months. You picked up a second credit card when you needed new tires on your car and the store offered you interest-free financing and a $50 gift card if you paid it off in six months, which you know is doable.

Now you have multiple cards, and your next plan is to save up for a down payment on a condo. Debt consolidation may simplify your budget and better position you for your first home. (If you already carry significant credit card balances or are flirting with bad credit, you may not be able to consolidate at a reasonable rate, so be mindful of debt consolidation offers — they may not help you in the long run.)

Isn't a credit card loan capable of providing all those same services? Yes, but there are some differences you should know between these two types of loans that may help you make smarter debt management decisions.

Aren't credit cards just as easy as a personal loan?

When it comes to ease of use, credit cards are the quickest, fastest way to buy what you want.They are also the quickest, fastest way to find yourself in debt. This month you owe $75. Next month you owe $250. The month after that you're now looking at a monthly payment of $400. Sure, you can just pay the minimum balance of $75, but now you have accumulating debt.

Luckily for the credit card company, you have become their bread and butter — they were hoping this would happen. It's how they make their money.

A personal loan is most often an unsecured loan, and you might say a credit card loan is its closest cousin because they have a lot in common, but there are some definite differences between the two.

Here's where personal loans vary from credit cards loans: a personal loan is a set amount you are given up front, unlike when you borrow money in drips and drabs from your overall available credit (aka your credit limit). Credit card limits are basically the total amount of the credit card loan you receive when you apply. A personal loan pays you the full amount of your loan once you are approved.

With credit card loans, your monthly payment changes based on usage. Credit card companies cut you some slack and don't expect all the money up front, but they do expect your minimum payment. If that's all you pay them each month, your repayment period will last far longer than is necessary.

A personal loan establishes a monthly payment amount that remains the same over the life of the loan. No surprises. You will owe the same amount this month as you did last month. Same thing next month. That's a far more logical and convenient way to manage your money.

Credit cards offer you introductory rates, and then up the rates after the first few months of dating your credit card company. This new rate will be entirely based on the current prime rate, plus whatever additional amount was mentioned, likely in smaller print, when you opened your credit card loan. Of course, if the prime lending rate changes again, your credit card rate might also change. Personal loans come with a fixed rate, so no surprises when you make your monthly payments.

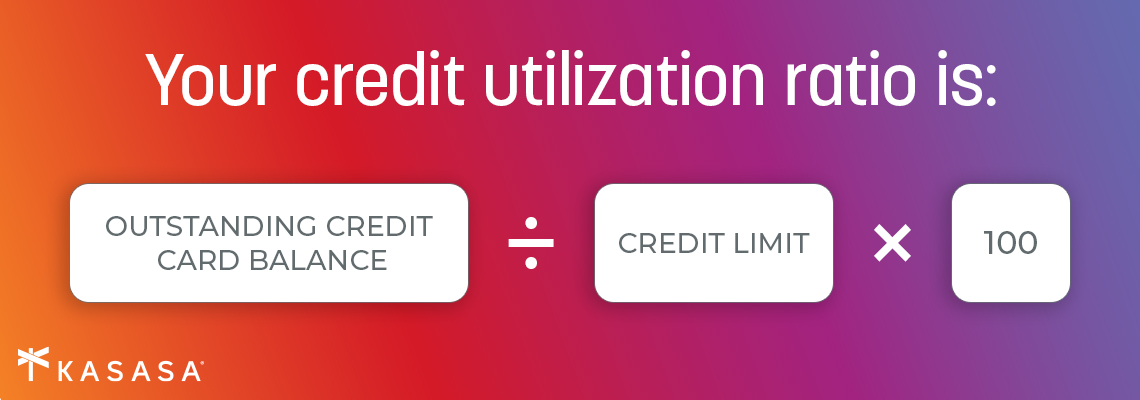

Credit cards are super easy to get. How often have you been at a store and been offered the ability to save 10% today on your purchase by opening a credit card right here, right now? Tempting? Yes. Convenient? Yes. Smart? Nope. Your credit score will take a hit, not just from the credit inquiry, but also from extending your credit utilization ratio.

With a personal loan, you can still expect a credit pull, and yes, your credit will take a hit, but that's true when you apply for any loan. The upside with a personal loan is the level of control you may have over the payment terms, the interest rate (which is often better than credit card interest rates, especially after the hot-and-heavy introductory rate is over), and the way the payments can fit into your budget month over month.

Features like repayment plans, lower interest rates, and a different application process separate personal loans from other unsecured loans. Applying for a personal loan is similar to applying for an auto loan. Your credit worthiness will get a close look, and by providing your credit history, credit score, and income, you'll help the lender answer one question: How likely are you to repay this debt?

Can you get a personal loan anywhere?

Where can't you find a personal loan these days? Everyone from the credit union down the street, to the bank in your grocery store, to the national bank with the offices downtown, to the list of logos served up after an Internet search can offer you a personal loan. It may be helpful to understand how different types of financial institutions manage, or service, loans.

There are three main types of lenders in the personal loans marketplace these days: Megabanks, community financial institutions, and neobanks. You obviously know the first two categories, but we'll introduce you to all three to clarify what each provides when it comes to places to take out a personal loan.

Megabanks are the big, national chains with a branch or ATM on every corner. They're the Starbucks of banks. Megabanks have a strong brick-and-mortar presence in larger cities, many of them are multinational corporations that focus on large-scale business, that brag about every feature on their mobile app (even the ones you'll never use), and that in some cases have been around for more than a century. You will have less flexibility when it comes to negotiating personal loan interest rates, but you'll be in good company — lots of people borrow here and they have lots of money to lend.

Megabanks exist as the giant in a David-and-Goliath struggle against the little guy, community financial institutions. Small, local banks and credit unions also operate brick-and-mortar branches, but at a much smaller, more human scale than megabanks. The best community banks and credit unions put their focus on real, human relationships front and center. When it comes to the loan process, expect the customer service to be detailed and personal, which is especially helpful if you are taking out your first loan.

The third type of lender is online-only, and a new entrant to the field of banking, even though almost half of loans are now serviced online only. Sometimes called "neobanks," this new wave of online lender uses whiz-bang technology to cut out the middleman: megabanks and other traditional financial institutions. They offer a seamless, app-first approach to lending, but rarely have any offline presence to handle problems if something goes wrong. Although, they are more than happy to send you lots of communication. Lots and lots of emails. All the time.

Can you just start applying and hope for the best loan?

Yes, much like credit cards offer you the ease of quick point-of-sale use, applying for a personal loan online will give you the ability to provide all the necessary information from the convenience of your dining room table, home office, or living room couch. Most local banks and credit unions offer online loan applications, too. This certainly is the easiest place to get started, but take your time. Applying for a loan isn't one or two small steps, and the impacts on your credit and budget will matter as you move through the application process.

There will be a point in this process, however, when a "hard pull" is made against your credit. This is when it shows up on your credit report. It's a good idea to do your homework before this happens. Even if you only proceed as far as a "soft pull" that doesn't ding your credit score, once you offer up your personal information — let's say your email address — you are going to receive non-stop offer information, reminders to continue the process, and prompts that try to grab your attention. If you have time to sort through all the clutter, do it, but it might be easier to spend time doing a bit of research to avoid being pummeled by the onslaught of "Pick me! Pick me!" emails.

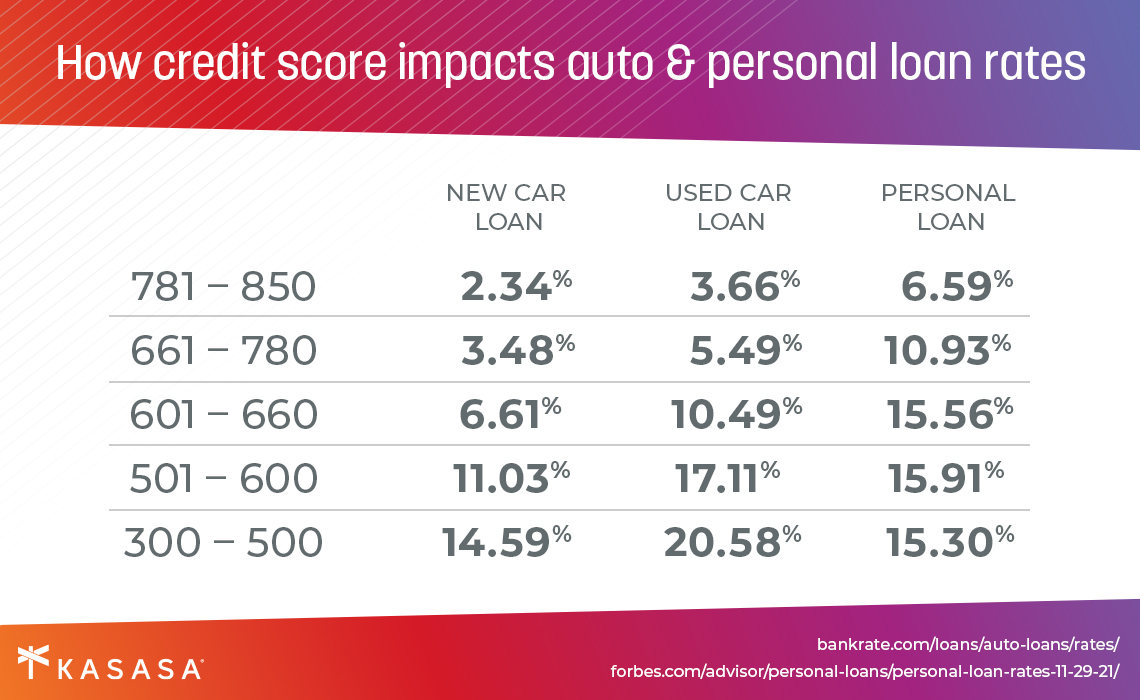

Expect that most website offers lead with the interest rates that will be the lowest rate for those with excellent credit, not necessarily the rate for which you will qualify. To further educate yourself, find out your credit score before you apply anywhere. You can obtain this information from a variety of sources. Some banks and credit unions include it in their online banking feature, but you can also get it for free from a variety of reputable websites. Knowing your credit score will give you a better idea of what kind of personal loan interest rates you could get, or, better yet, what interest rate you can negotiate.

Taking out a personal loan from a local lender, like a small bank or credit union, is the better choice if you aren't entirely sure where to get started. Borrowing local often means you can find the loan term that fits your specific plans, a monthly payment that fits your budget, and peace of mind knowing that you'll have one bill to keep track of, rather than multiple messy credit card statements with different interest rates and repayment schedules.

What should you expect when you apply for a personal loan?

There are a few basics to understand up front about the application process for a personal loan. These personal loan requirements come into play whether you're taking out a loan at a big, national bank, a smaller, regional bank based in your local community, or a tiny, rural credit union.

Application and credit check

The first thing you're going to do is fill out a loan application. This form will ask for your full name, a valid form of identification, and your Social Security number. That last piece of info not only verifies that you are who you say you are; it also allows the lender to access your credit history and current credit score. This is a major factor in getting qualified for a loan. Your credit history and credit score also affect the interest rate that a lender will be willing to offer you once approved.

While a credit score gives a potential lender an idea about your financial past, you'll also be asked to give information about your financial future by proving regular income. The other key pieces of information that you will provide on your application are the amount you'd like to borrow (also called the loan amount ), and the amount of time over which you plan to pay that loan amount back (the loan term, or repayment term).

Loan application review

Once the loan officer has all this information, the information will be reviewed and, if you qualify and receive credit approval, you will receive a loan offer that includes an interest rate and a monthly payment based on the repayment term. If you borrow from the bank or credit union you already know and love, it is not uncommon to have the funds direct deposited into your checking account and have the loan account show up on your mobile app or online banking the next time you log in.

Loan acceptance

Some online lenders might provide you with an immediate acceptance, or at least within a short response time, but the loan offer may not include the annual percentage rate (APR) of the loan. Be certain of all the loan terms before finalizing any choices. There may be fees associated with the initial loan, so be sure to know what these are in advance of signing your loan paperwork (which can also be done from your home office or living room couch).

Online security

Online safety alert since scammers are out there: Never give your Social Security number or any other personal information to an unverified online party, like an unsolicited loan offer you get via email or social media. It's normal, even necessary, for a legitimate lender to request this information before offering you a loan, but be sure you're providing this info to a real financial institution and not a scammer! If a lender is asking you for any other information up front, such as bank account info, or is charging you "processing" fees of any kind, these are signs of personal loan scams.)

But do you qualify for a personal loan?

Submitting all the necessary paperwork, while not the most fun activity you can do, will complete the adult-homework portion of the process. What happens next? How do you maximize your chances of qualifying for a personal loan?

As we mentioned, your credit score and your employment situation are going to play a major part in determining whether you will qualify. From a lender's perspective, any loan is a risk, and an unsecured loan is riskier for the bank than a secured loan. At this point, there's not much you can do about your credit score (although, we can offer a few tips to help it rise over time), but the more info you can provide in terms of income and employer verification, the higher your chances of qualifying for a loan, and getting a better interest rate.

When you send in a loan application asking a lender (a bank or credit union) to be paid back over a period of 12 months, the lender will want to know how much you can afford to borrow, from their perspective. They'll first verify your ID based on the info you've provided, then get a financial snapshot from your credit history and employment information. The more info you can give to the lender about your financial picture on top of that, the better. Proof of address, like mail in your name, can give the lending officer a better sense of your overall stability.

Giving a lender more information about what you plan to use the loan for can also go a long way to getting you qualified. This may feel like extra work — let's face it, the credit card company doesn't care where you plan to spend your money as long as they get their interest charges and fees. If you want to eliminate the downsides of maxing out your credit card, these extra steps may prove worthwhile.

Let's say you've moved to a sunnier locale and the family plans caravan down for Thanksgiving this year. It won't take long before a family gathering of any type snowballs into a huge family reunion. This might be the time to consider a personal loan to cover all the things you know you'll need: more chairs, a bigger dining room table, maybe even a minor, last-minute home improvement project so you aren't forced to play the family football skirmish in the yet-to-be-landscaped mud pit that is your new back yard.

Rather than put all that expense on your credit card and trying to pay as much as possible just before Christmas, you want to take out a personal loan and have a clear repayment schedule in place to make up for those costs over the course of a year. Identifying how you plan to allocate the loan amount will give the lender a clear picture of what your plan is for both spending and repaying the money.

Your loan eligibility will depend upon all the factors above no matter where you apply, but we at Kasasa® believe in borrowing local with a community bank or credit union, which will have a greater investment in you as a person and valued client, rather than just a faceless consumer. The requirements for an unsecured personal loan will depend on the loan amounts and loan terms, which will in turn affect the interest rate, which determines your monthly loan payment, but your experience will vary greatly between a community financial institution and a megabank, or so-called neobank. Plus, we have an ace up our sleeves.

What if you need to borrow more money in the future?

Good news: your initial personal loan is helping you establish good credit. Whether your next loan is a personal loan, and auto loan, or a home mortgage, establishing excellent credit starts with making timely monthly payments on your first loan, so you're off to a good start.

Kasasa isn't a "neobank." In fact, we're not a bank at all. We are the only financial technology (aka "fintech") company whose mission, for nearly two decades, has been to help community financial institutions thrive. Kasasa partners with community financial institutions around the country to offer the best of both worlds: a technically sophisticated, easy-to-use personal loan that is serviced by a trusted local community financial institution.

Here's that ace we mentioned: The Kasasa Loan® offers the most flexibility of any personal loan because it's the only loan with Take-BacksTM. They're just what they sound like: Take-Backs let you pay ahead to get out of debt faster but still have access to those extra funds when you need them. So now the personal loan has the flexibility of a credit card to utilize the amount you've paid ahead on your loan, but with the benefits of personal loan interest rates, fixed monthly payments, and the personal service of a financial institution you trust.

So what are you waiting for?

We've covered various types of loans, the difference between secured versus unsecured loans, and all the ins and outs of personal loans. You are well informed. So how do you know if a personal loan is right for you? Here are four questions that may zero in on the answer you are trying to find:

1. Do I have enough money on hand to make this purchase?

If yes, then you might not need a loan at all, but you may still want to consider a personal loan if you are looking to beef up your credit history.

2. Am I looking for a better interest rate than I can get with my credit card?

Why wouldn't you want a better interest rate? But you might also want to benefit from the fixed interest rate for the duration of your loan.

3. Do I want to have consistency in my monthly payments?

If your goal is to manage your budget in the short term and improve your credit score in the long term, fixed monthly payments make the possibility much more plausible.

4. What am I waiting for?

A personal loan offers a wide spectrum of debt management solutions and long-term financial benefits to consumers. Making informed choices about what type of loan works best for your budget, your needs, and your future purchasing plans requires more than the fastest application process or the quickest swipe of a card. But getting started applying for a loan may be the first step to building excellent credit and enjoying your friend's wedding, the invasion of your family for Thanksgiving, or your first step to a lifetime of financial health.