There are many scenarios when taking out a personal loan rather than credit card transactions can be the smarter, easier way to pay for the holidays.

Itchy spending fingers tend to reach unconsciously for the credit card around this time of year. Unexpected and totally planned expenses add up, and can get out of control fast, ultimately damaging your credit score. Boo! Holiday party foul.

There are many scenarios when taking out a personal loan rather than stacking up a big pile of credit card transactions can be the smarter, easier way to pay for the holidays and all they entail.

Maybe after laying low in 2020 you are cautiously planning some Thanksgiving or end-of-year travel. You probably have a gift or two (or ten) to pick up in the coming weeks. Lots of big meals going down in that same time frame most likely. And, holidays aside, you may have a few personal-use items on your shopping list that’ll look a lot more attractive when deeply discounted on Black Friday or Cyber Monday.

Taking out a personal loan from a local lender, like a small bank or credit union, is the better choice if you know you’re looking at a big end-of-year spend. Borrowing local often means you can find the loan term that fits your specific plans, a monthly payment that fits your budget, and peace of mind knowing that you’ll have one bill to keep track of, rather than multiple messy credit card statements with different interest rates and repayment schedules.

Plus, paying off a modest personal loan on time improves your credit score. Win, win!

So what’s the best way to take out a simple loan for the holidays? Is it better to get a personal loan online or in a brick-and-mortar bank or credit union?

If you’re interested in getting a financial boost just in time for that anticipated bump in holiday spending, we’ll help you figure out how to apply for a personal loan, which factors figure into how you qualify for one, and the best place to get a personal loan for the holidays.

How to apply for a personal loan

There are a few basics to understand up front about the application process for a personal loan. These personal loan requirements come into play whether you’re taking out a loan at a big, national bank, a smaller, regional bank based in your local community, or a tiny, rural credit union.

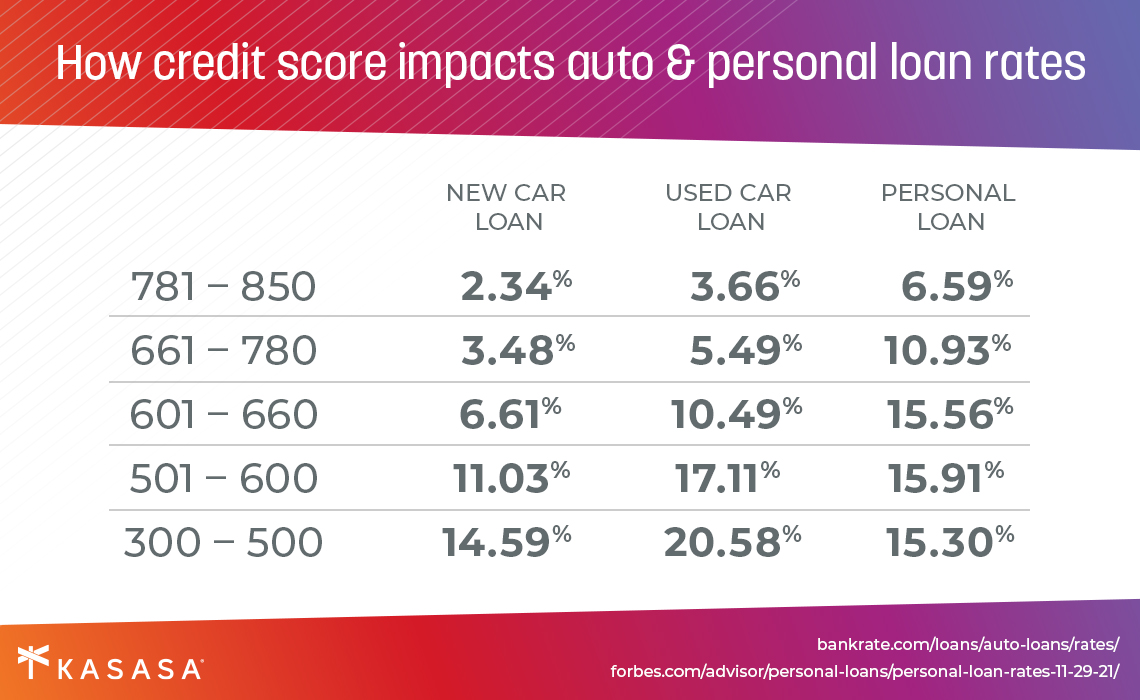

The first thing you’re going to do is fill out a loan application. This form will ask for your full name, a valid form of identification, and your Social Security number. That last piece of info not only verifies that you are who you say you are; it also allows the lender to access your credit history and current credit score. This is a major factor in getting qualified for a loan. Your credit history and credit score also affect the interest rate that a lender will be willing to offer you once approved.

While a credit score gives a potential lender an idea about your financial past (specifically, your ability to pay back the tiny loans you rack up on your credit card on time), you’ll also be asked to give information about your financial future by proving regular income.

The other key pieces of information that you will provide on your personal loan application are the amount you’d like to borrow (also called the loan amount), and the amount of time over which you plan to pay that loan amount back (the loan term, or repayment term).

Now that the loan officer has all this information, they'll run through it and, if you qualify, come back to you with a loan offer that includes an interest rate and a monthly payment based on the repayment term.

(A quick word to the wise, since scammers especially love to take advantage of people during the holidays: never give your Social Security number or any other personal information to an unverified online party, like an unsolicited loan offer you get via email or social media. It’s normal, even necessary, for a legitimate lender to request this information before offering you a loan, but be sure you're providing this info to a real financial institution and not a scammer! If a lender is asking you for any other information up front, such as bank account info, or is charging you a “processing” fee of any kind, these are signs of personal loan scams.)

How to qualify for a personal loan

You have all your documents and information in order and are ready to send your personal loan application through. What happens next? How do you maximize your chances of qualifying for a loan?

As we just mentioned, your credit score and your employment situation are going to play a major part in determining whether you qualify for a loan. From a lender’s perspective, any loan is a risk, and an unsecured loan (like one you might take out to cover holiday incidentals) is riskier than a secured loan (which has an asset like a car or house to back it up). There’s not much you can do about your credit score (except pay back your loans on time and watch it rise!), but the more info you can provide in terms of income and employer verification, the higher your chances of qualifying for a loan, and getting a better interest rate.

Giving a lender more information about what you plan to use the loan for can also go a long way to getting you qualified. Let’s say it's your turn to host Thanksgiving this year, and it’s snowballed into a huge family reunion that you weren’t prepared to handle. You want to take out a small loan, $1,500, to cover all the things you know you’ll need: more chairs, at least one extra bird, maybe even a last-minute home improvement project to knock down a wall and make more space for all the grandkids to roam.

Rather than put all that (and who knows what else) on your already over-extended credit card, you want to take out a personal loan and have a clear repayment schedule in place to make up for those costs over the course of a year.

When you send in a loan application asking a lender (a bank or credit union) for the $1,500, to be paid back over a period of 12 months, the lender will want to know how much you can afford to borrow, from their perspective. They’ll first verify your ID based on the info you’ve provided, then get a financial snapshot from your credit history and employment information. The more info you can give to the lender about your financial picture on top of that, the better. Proof of address, like mail in your name, can give the lending officer a better sense of your overall stability.

Your loan eligibility will depend upon all the factors above no matter where you apply, but we at Kasasa® believe in borrowing local with a community bank or credit union, which will have a greater investment in you as a person and valued client, rather than just a faceless consumer. The requirements for an unsecured personal loan will depend on the loan amounts and loan terms, which will in turn affect the interest rate, which determines your monthly loan payment, but your experience will vary greatly between a community financial institution and a megabank, or so-called neobank...

Where to obtain a personal loan for the holidays

There are three main types of lender in the personal loans marketplace these days: Megabanks, community financial institutions, and neobanks. The first two you’re probably familiar with; the third one probably sounds a bit funky. Let’s briefly describe the three major places to take out a personal loan.

Megabanks are the big, national chains that seem to have a branch or ATM terminal on every corner. The Starbucks of banks. Megabanks have a strong brick-and-mortar presence, many of them are multinational corporations, and some have been around for more than a century.

Megabanks exist as the giant in a David-and-Goliath struggle against the little guy, community financial institutions. Small local banks and credit unions also operate brick-and-mortar, but at a much smaller, more human scale than megabanks. The best community banks and credit unions put a focus on real, human relationships front and center.

The third type of lender is online-only, and a new entrant to the field. Sometimes called “neobanks,” this new wave of online lender uses whiz-bang technology to cut out the middleman — megabanks and other traditional financial institutions. They offer a seamless, app-first approach to lending, but rarely have any offline presence to handle problems if something goes wrong.

Kasasa isn’t a “neobank” — we’re not a bank at all. We are the only financial tech (aka fintech) company whose mission, for nearly two decades, has been to help community financial institutions thrive. Kasasa partners with community financial institutions around the country to offer the best of both worlds: a technically sophisticated, easy-to-use personal loan that is serviced by a trusted local community financial institution. The Kasasa Loan® is the best loan for holiday expenses because it’s the only loan with Take-Backs™, which let you pay ahead to get out of debt faster but still have access to those extra funds when you need them.

What to consider when choosing a lender

Let’s recap: If you are anticipating a big end-of-year spending spree for whatever reason — holiday travel, gift shopping, or just spoiling yourself on big sale days — an unsecured personal loan to cover holiday incidentals may be the best call for you.

And regardless of your credit history or current employment status, a community financial institution is probably the best bet for taking out a modest personal loan with a manageable monthly payment and a loan term that fits your needs.

Megabanks will likely cost you more money in the long run, and have famously bad customer service. Neobanks can be good for getting a loan quickly and easily if you’re the always-online type, but may not offer the best personal loan interest rates, and most likely won’t have great customer service if you ever encounter a problem.

A community financial institution that will be more invested in your long-term well-being is the obvious choice for maximizing holiday cheer!

A Kasasa Loan gives you total control over the variables we just covered, and can help you borrow smarter this holiday season instead of racking up more high-interest credit card debt. Our unique Take-Back® feature lets you reclaim extra money you’ve already paid toward your loan, giving you access to funds when you need them most. Just the thing you need for super-last-minute stocking stuffers!