When it's time to sign your name, having a plan for how to obtain and manage your vehicle loan should be just as important as the features you want.

Few purchases rank higher in your life than buying a car, perhaps second only to buying a home or starting a business. As often as you will use your new car to go to work, the store, your friend's house, (and yes, the gas station), the practical need to own your own car also requires most of us to take out a vehicle loan. Sure, paying cash would be ideal, whether you are buying brand new from a dealer, or just picking up a new-to-you pre-owned vehicle from a friend. Reality check: auto loans help us get from place to place as much as the four wheels and gas pedal.

You know you'll need to borrow the money to make the purchase, but before you start the car, you need to start the car buying process. Sales tax, an extended warranty, and auto insurance should all get a close look, but so should the dollars and cents as you fill out the credit application. When it's time to sign your name and you are handed the keys, already having a plan for how to obtain and manage your vehicle loan should be just as, if not more important, as the model and features you want.

Obviously loans accrue interest as you pay back over time, so prepare before you seal the deal knowing auto loan rates, your ideal monthly payment, and your responsibilities as a borrower. Let's take a few minutes to get you ready to find the car you want and the loan you need.

1. Know your credit score

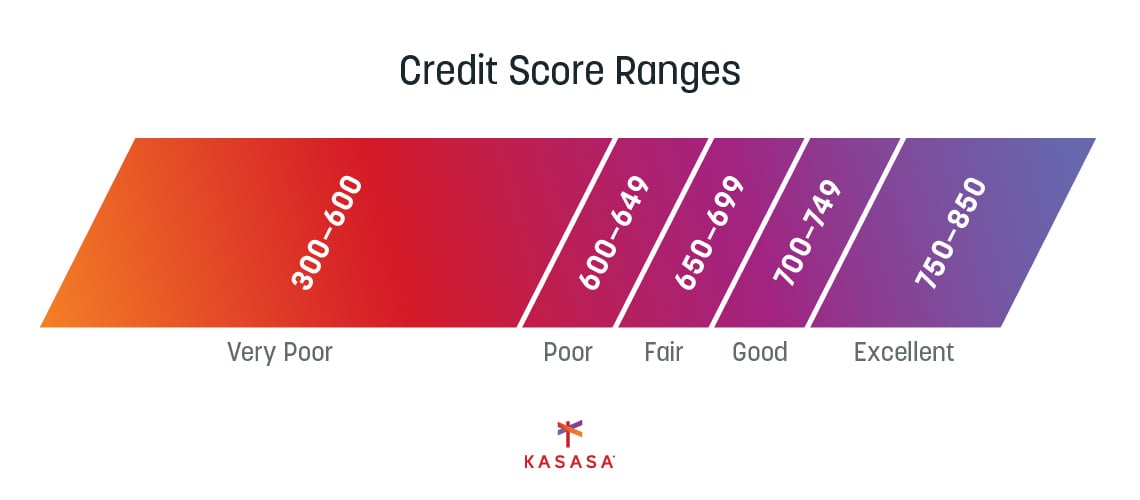

With any loan — student loan, refinance, car loan — your credit score is the single most important factor in determining everything from your interest rate, the loan amount, the monthly payment, and even the 'yeah' or 'nay' from the dealer — or your credit union or bank.

Note that not all lenders use, or look at, the same scoring system. "Different lenders have different criteria so the minimum score needed to qualify will vary depending on which company is providing the financing," according to Experian.

So how do you find out where you stand before you apply? That's easy. There are resources a-plenty to educate yourself on the details of your credit history and how to improve your credit score. Knowing what your credit history looks like will help you secure the maximum loan amount and the best auto loan rates, so know the likelihood of getting credit approval before you go for a test drive.

2. Apply for loans during a 14-day time span

Your credit score will slightly decrease when lenders check your credit history, but keeping your application process within a two-week period helps reduce the negative impact. For this reason, having your vehicle loan plan in place before you visit the dealership will avoid having multiple hits to your credit if you want to take your time to find the best car to fit your needs - or fulfill your wants.

Why is this? The "shopping period" is 14 days so all inquiries made during that time will be considered as one, reducing the hit on your score. Your credit score fluctuates based on your credit history and your current credit-related activity. Hint: Don't apply for a credit card at your favorite clothing store while you are also in car-buying mode.

3. Get pre-approved, then shop

It's always best to walk into the car dealership with a financing offer from a bank or credit union already established. A pre-approved offer guarantees that you have a loan to cover the cost of the car you want. Having auto financing finalized lets you focus on the vehicle choice without having to worry if you can swing the monthly payment.

Of course, planning ahead allows you to organize your financing. Perhaps you do not have excellent credit, but being able to have a level of control over your loan rate, the monthly payment amount, or even negotiate a competitive rate based on your financial history by having a relationship at your community bank or credit union can positively impact your loan terms.

There's an added bonus to having a loan already in hand: car buyers walking into dealerships with secured loans already in their pocket are irresistible — it gives you additional leverage to control the negotiations on price and features. You will find yourself, literally and figuratively in the driver's seat.

4. Calculate costs before saying yes

As you're securing your financing, it's important to understand the factors that go into setting your monthly car payment. The APR only has a small effect on the amount you pay each month. Once you get to the dealership, you could get hit with extra costs.

Sales tax will absolutely impact the bottom line as to the cost of the vehicle. If you include the taxes as part of the overall price of the vehicle, the sticker price won't be the same as the loan amount.

You might also need to consider the dealer fees that may be included in the price, as well as the cost of extra features. You could negotiate whether or not the vehicle includes some extras. The polarized windows and the leather seats may not be removable, only negotiable when agreeing upon the price. Before you say, "Yes," know when to say, "No," if the cost isn't within your budget.

Use an auto loan calculator to play with the numbers. You may be in a hurry to drive that car off the lot, but taking a day to run the numbers can save you thousands in the long run.

5. Understand dealership financing

Sometimes dealership financing can appear to be a more attractive offer. Deals like 0% financing and large cash back rebates, which can ultimately reduce the total amount of your loan, may sound like the best option.

Remember that most financing options are only available to the highest qualified buyers. If you have anything negative on your credit report, a low credit score, or limited credit experience, you will likely not qualify for these specials.

In either case, always shop around. Never accept the first financing option offered to you by a dealer, especially if you have already told the salesperson how much you love the car. They know you are thinking with your heart and not your head — or your wallet.

Also, consider borrowing an amount that allows your budget the flexibility to pay more than the monthly payment amount to help improve your credit score for the next auto loan after this one. Kasasa Loans® with Take-Backs™ give you the ability to pay ahead to get out of debt faster but still have access to those extra funds when you need them. Give yourself some wiggle room.

Having a financing plan for your new car is a great way to get the vehicle that you want and need without making unnecessary sacrifices. The process may feel complicated so keep these tips in mind before agreeing to anything. When you do your research, get pre-approved, and run the math by yourself, you'll walk away feeling good about the car and your financial situation.