If you’re a car owner looking to refinance your vehicle, we’re here to give you a comprehensive picture of how to refinance your car. Get a pen and paper.

We’ve been over the pros and the cons of auto refinancing, when and why you should refinance your car. Now let’s get down to brass tacks (or lugnuts, if you will): How do you refinance? What all will you need, where should you do it, and how can you get started today?

Have you ever been cruising down the highway and done a double take at a billboard advertising an auto loan rate way lower than what you’re paying now? Then you’re in the right place.

If you’re a car owner looking to refinance your vehicle, we’re here to give you a comprehensive picture of how to refinance your car, different options for where to refinance, and why a local lender may be the best choice for vehicle refinancing. Get a pen and paper out and read on! 🤓

When you shouldn’t refinance your existing auto loan

First, let's recap some basics to make sure you’re in the right place. When might refinancing your car be ill-advised? How does refinancing an existing auto loan impact your credit score?

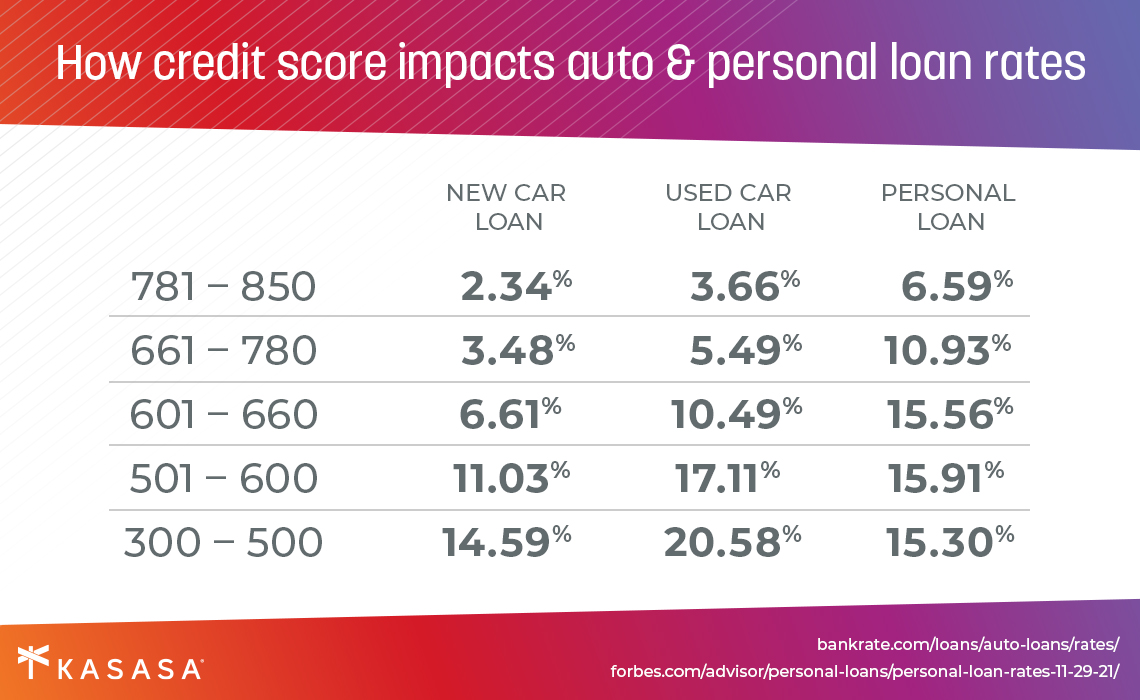

Credit history is an extremely important factor in your auto refinancing loan application. A potential lender will decide whether or not to offer you a loan (and if so, at what interest rate) based on your credit history and your current finances. A bank or credit union extending a loan is largely informed by an applicant’s FICO credit score, which is based on information from your credit report and your current monthly payment plan of any existing credit sources.

If your credit score has gone down since you originally financed your vehicle, you’re not likely to get a better deal now, so it’s probably not worth applying. Refinancing your auto loan can sometimes harm your credit score, but in most cases, your credit score only takes a small and short-lived hit when you take out an auto refinance loan. (Learn more about how auto refi affects credit here.)

If your credit score has improved but you don’t have enough credit history, you still might have to wait on refinancing. Many first-time car owners have what lenders called a “thin” credit file, meaning there’s not enough car payment history to establish your ability to repay your vehicle loan on time, over time. All you have to do is be consistent, though: You can typically look into refinancing after a year as long as you don’t get behind on payments.

Finally, if there are higher interest rates in the market now than when you originally financed your vehicle, you may want to wait for a better rate before pursuing auto refinancing.

How to refinance your car

If you’re still reading, let’s move on. You’re ready to move forward with refinancing your auto loan, either because you’re able to get a good APR, a lower monthly payment, or both. Your credit score has improved and your credit history stretches back a little longer now. You can finally lose your co-signer (thanks, Mom!).

Time to break down some basic loan facts. What information do you need to refinance your car? What are the steps involved with auto refi? What are some common pitfalls to avoid when refinancing an auto loan?

The first thing to do is decide your overall goal: Do you want to lower your monthly car payment? Do you want to pay less money in the total life of your loan? Do you want to get out of debt ASAP, even if that means a shorter-term loan and a larger monthly payment?

Depending on those factors, decide if you want to change your loan term (aka the repayment timeline), and if you want to increase or decrease your monthly auto bill. Here's the other information you’ll need:

-

Your credit score. By now you know how important that is! If you don’t know yours, you can check it using a free service like Experian.

-

Your ID and car details. A lender will want to know details about the car you’re refinancing. Have your car’s make, model, VIN number, and mileage on hand. You’ll also need to have a valid driver’s license.

That’s really all you need. There’s only one important question that remains to be answered...

Where is the best place to refinance your auto loan?

A lot of us, when we’re younger, don’t really know exactly what to look for when financing a vehicle. Maybe it’s the path of least resistance to take out a loan at the dealership, or from the cookie cutter megabank where you already have a savings and checking account. Now that you’re ready to refinance, and you’ve done your homework, you are probably realizing that it’s time to fly the coop and refinance your auto loan with a financial institution that will give you a better rate, better terms, and better service.

So, what are your options?

There are of course the megabanks. The huge, national chain banks all offer auto loans, though their rates usually aren’t great, and their customer service is about what you’d expect from massively bureaucratic, multinational corporations. Megabanks have branches and ATMs all over the place, which is convenient. But they deal in volume, which means you're treated more like a number than a person. A lot of times you'll be directed to a 1-800 number that’s answered on the other side of the Pacific.

Community financial institutions, on the other hand, usually don’t offshore their customer service. Small local banks and credit unions have the same product offerings as megabanks, but operate at a much smaller scale. Some are just a single brick-and-mortar shop; some are rural credit unions connecting a small number of people spread across a humongous stretch of land. The best community financial institutions put a focus on real, human relationships front and center, and function as the financial heart of their local economy.

Kasasa® partners with such community financial institutions around the country to offer a technically sophisticated, easy-to-use auto refinancing loan that helps smaller community financial institutions, the bedrock of local communities nationwide, to hold their ground against the big corporate banks, who are trying to gobble them up.

Why you should choose a local lender for vehicle refinance

All lenders want to know details about you and your credit history. That’s why they ask for your ID and so much financial data. What makes a good local bank or credit union different is they want you to know who they are. Your long-term success means their long-term success, and an auto refi loan with a community financial institution is more of a relationship than a product transaction.

When you take out an auto refi loan with a community financial institution, you get to reset your entire auto financing experience. This feels especially good if you got a lousy original loan from a car dealer, or are ready to ditch the impersonal megabank experience and cast your financial lot in with a community-oriented bank or credit union.

The Kasasa Loan® is a new kind of loan that arms community financial institutions with the tech-forward tools they need to reach people like you: Informed and ready to borrow smarter. We are the only financial tech (aka fintech) company whose mission, for nearly 20 years, has been to help community financial institutions survive — and thrive. The Kasasa Loan is the only auto refinancing loan with Take-Backs™, a unique feature that lets you pay ahead to get out of debt faster, but still have access to those extra funds when you need them.

If you’ve read this far, have all your information lined up, and are ready to get out of your bad auto loan and into something more your speed, check out the Kasasa Loan today.