Before you get too far down the road refinancing your personal loan, it's good to have an idea of where you’re headed and the benefits it may offer.

Yes, of course.

That's the easy answer. Every type of loan may be refinanced, but it's important to know if you should refinance a loan. Knowing whether it’s the right time to refinance a loan depends both on current economic conditions and your individual finances.

The process of refinancing a personal loan may not be too different from any other type of loan. It will usually include all the same steps as your original loan, except that you have a better idea of what to expect throughout the process. If you already have a personal loan, then getting a new one is more about the reasons why you should, if it’s the right time for you, and what the benefits (or shortcomings) of a shiny new loan may be for you. Those factors may also guide you to consider alternatives, so before you get too far down the road, it's good to have an idea of where you’re headed.

Reasons to refinance a personal loan

If you’re considering refinancing a personal loan, you've already gone through the process at least once, so the steps to getting a loan are not new to you. Your reason for refinancing will likely be the driving force in making the choice.

Let's face it: No one chooses to refinance any loan simply for the opportunity to subject themselves to more paperwork. Yes, you can expect that to be part of the process, but you already knew that. The real motivation comes from the upside it will bring to your finances.

The most likely reason to refinance any loan — whether a home equity loan, your collection of student loans, your auto loan, or even your home mortgage — is to lower your current interest rate. The goal is to save yourself money, and that is reason enough to consider the process.

If you have a credit card and a car loan, plus a couple of lingering student loans that you have let sit quietly accumulating interest, cleaning your financial house and consolidating them into a single loan may be the perfect reason to refinance your loans.

While personal loans will come with a slightly higher interest rate as an unsecured debt, simplifying your debt will bring your finances into line and give you a direct path towards longer-term benefits, such as an improved credit score or a single monthly payment. Getting rid of those multiple loans can make a lot of sense.

Perhaps back in the day when your credit was only *meh* you used your credit card to cover costs. For example, that time you needed new tires for the car and the tire shop extended you a special deal on their credit card in exchange for a buy now, pay later option. That definitely made sense in a pinch. Now you’re looking for a wiser way to manage expenses. Moving from a credit card loan to a personal loan is really just refinancing your personal debt — and a smarter way to do it, at that.

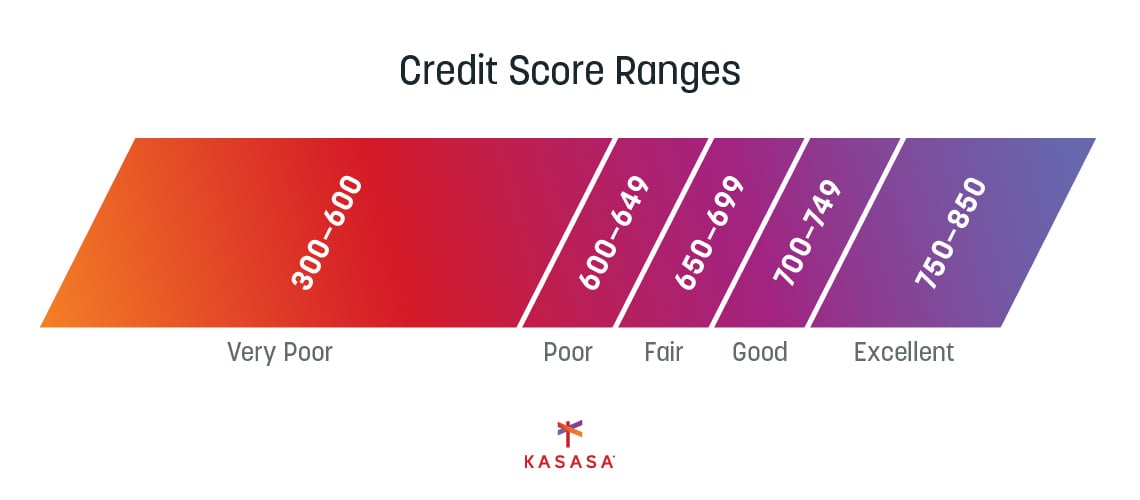

Prioritizing your credit score, whether for a future big purchase or for the stability it will bring, may be one of the best reasons to refinance your existing loan. You've seen how regular payments on your loan have moved you from a fair credit score (or perhaps at one point, bad credit) to a good credit score. A personal loan refinance can give you the ability to keep building on your success. It may lower the score slightly for a short time, but if you are committed to more aggressive payments than when you first opened your loan, why not make that lower monthly payment work to your advantage as you pay ahead on your loan and knock out your debt even faster.

You may discover dozens of other reasons to refi, such as a change in your marital status leading you to combine your debt and your partner's debt. You might be on track to purchase a home, and you want to reign in all those multiple loans. Perhaps you took out your loan with the megabank that had that clever Superbowl ad, but their service isn't what you expected, and you want to move to a community bank or credit union where you live. Whatever the reason, transitioning from your current loan to a loan that better suits your financial plan makes personal loan refinancing worth consideration.

When to refinance a personal loan

We've covered how lower interest rates, debt consolidation, lower monthly payments, and the elimination of your credit card debt might all be your motivation for refinancing a personal loan, but is now the right time?

The timing depends on current economic conditions. Looking back at those reasons, if your primary motivation for personal loan refinance is to lower your interest rate, you should make sure the current rates being offered are better than the rate on your old loan.

Review any loan offer carefully. If you discover you are not eligible for the best available rates, it may be due to your own credit history. There may be an unexpected debt that has appeared on your credit report, and sometimes that could be an error in your credit history. Again, the timing to refinance may depend on you — and a co-borrower, if you're combining debt — as much as it depends on market rates.

If you are in the process of paying down past debt and are making decent headway, you may want to consider the advantages of personal loan refinancing. It can take a few months for your credit report to reflect a recent pay down or pay off of an old loan, however. Speaking with a loan advisor at your bank or credit union may help you align on where your score needs to be for you to qualify for a better repayment term.

(Tip: Another upside to working directly with a lender is you’re often able to negotiate a better loan term than you might through a neobank or megabank.)

When considering the timing, it's helpful to look at the full loan term and how the payments are applied. Typically, the earlier loan payments cover the interest and the later loan payments cover the principal. Are you more than halfway through your payment plan on your existing loan? Knowing how close you are to the money-saving tipping point is the key to your timing.

Even the loan amount, especially what is remaining in comparison to the original loan amount, may factor into the timing. Again, having a personal loan advisor to help assess your timing will help answer the question of both when and if you should refinance your loan.

The timing of going through the application, the credit approval process, and receiving the funds can obviously vary, too. The timeline may be different if you’re refinancing an existing personal loan versus getting a new one, for example. If you have the flexibility to work through the process, it may be worth your while to consider the long-term benefits of combining multiple loans.

If your focus is on student loan refinancing, it may take more time for you to complete the necessary legwork — or homework, if you'll excuse the pun — to understand the implications of changing from a federal student loan to a private personal loan. You may lose some of the protections, so take the extra time to know what you may gain or lose in the process.

The pros and cons of refinancing a personal loan

Knowing all the implications may help evaluate the benefits of refinancing your personal loan in comparison to the drawbacks. In addition to the protections associated with student loans, there may also be fees and penalties moving from your existing loan to a new loan.

While a lower interest rate sounds appealing, take the time to calculate the overall savings. There may be a sweet spot, such as a dollar amount, where you decide it is or is not worth your time to refinance. Pull out your calculator, or use a personal loan calculator, and do the math.

Keep in mind the numbers may change throughout the life of your loan based on changing interest rates, especially if you have a variable rate on your loan. Other factors like how much you’ve paid ahead and your credit score can also affect the math, so the answers may change from year to year.

Let's talk prepayment penalties. Does your current loan have one? If you don't know, you'll want to find out. If you find out you are going to owe a chunk of change because you choose to refinance your existing loan, that's a big red flag to not pursue a new loan, even if the interest rates are better.

Those prepayment penalties absolutely depend on other factors. If you refinance your new loan with a financial institution where you already have an account, like a business account or where your spouse has a checking account, there might be some room to negotiate the fees and still get those attractive lower rates. Best advice? Ask.

One more factor to consider is whether the loan is fixed rate or variable rate. You may qualify for a lower interest rate, but if you switch to a rate that could change in a year or two based on the prime interest lending rate, you may not be saving any money. Likewise, if you know you can knock out the entire loan amount sooner than expected compared to the loan term, that may not be a concern for you.

Alternatives to refinancing

After reading this far, you may still opt against refinancing. So what other options are available?

Debt consolidation is also an option if decluttering your finances is your ultimate goal. This option will be impacted based on how many loans, and what kinds of loans, you already have and are looking to consolidate. Understanding the difference between debt consolidation and refinancing isn't too tricky, but it's worth a glance. The main difference is refinancing changes the terms of the loan. If you only have one existing loan and want to refinance it, there may be nothing to consolidate.

If refinancing isn't an option due to your credit situation, you may choose to pursue credit counseling. There is never a bad time to ask for help if you need it, especially if it’s going to get you back on the path you want to be following to improve your financial wellness. Be mindful of scams and disreputable options. The goal is to make the best choices for you, so make the first step the one to get you headed in the smartest direction.

You might also have a personal loan and would like to consider a personal line of credit. This may have the benefits of the best credit card with more reasonable loan terms. It may also require collateral if you are considering a secure loan, but if you plan to include your existing personal loan into the new line of credit, it may also include elements of new loan terms.

The obvious alternative to refinancing an existing loan is to love the one you're with. Keeping your current loan is always an option, especially if a new loan won't solve any of the reasons that made you want to consider refinancing in the first place.