A question many potential home buyers ask when applying for a mortgage is: Should I pay off debt before applying for a home loan?

A question many potential home buyers ask when applying for a mortgage is: Should I pay off debt before applying for a home loan? Credit card debt, auto loans and other forms of debt can all have an impact on a person's credit score, which in turn affects the rate they are able to get on their mortgage (or their ability to qualify in the first place). The answer isn't always as simple as a yes or a no, but there are a few figures to keep in mind that can aid in making this decision.

Potential home buyers that may have too much debt may limit the size of mortgage they are qualified to borrow. On the other hand, those who pay off debt too close to the date of application may experience other issues while obtaining a mortgage due to fluctuations in their credit score. Understanding the loan process, including what factors underwriters consider when they're approving a home mortgage, may help potential home buyers decide whether or not paying off debt is the correct decision for them.

Understanding your debt-to-income ratio

The debt to income ratio is an important factor that can influence how much a home buyer is approved to borrow. The ratio is important to mortgage lenders because research shows that borrowers who have too much debt are more likely to default on their loan.

The debt to income ratio is calculated by dividing a borrowers debt payments by their gross monthly income. For example, a home buyer who has a $500 per month car loan, $500 credit card payment with a $5,000 gross monthly income has a 20 percent debt to income ratio ($1,000/$5,000=20%). If that homebuyer were to be approved for a home loan with a $1,000 per month house payment, his or her debt to income ratio would then become 40 percent ($2,000/$5,000=40%).

In most cases, the maximum debt to income ratio that a home borrower can have and still be approved for a mortgage is 43% (including the future mortgage payment). A borrower who has too much debt to be approved for a mortgage may need to pay down their debt in order to proceed with the mortgage process. And, a potential home buyer who may desire to qualify for a higher loan amount (a more expensive home) than their debt to income ratio allows may also need to pay down some debt.

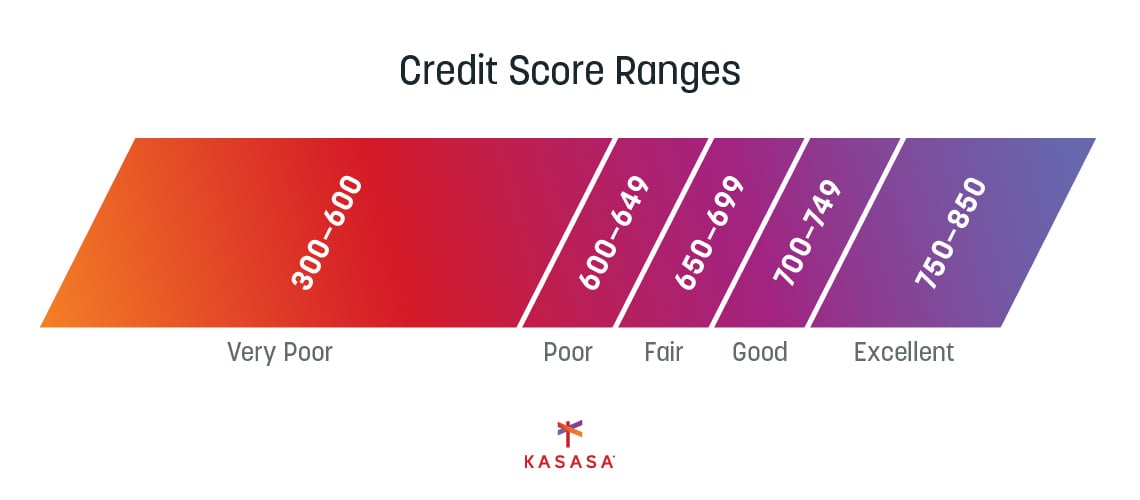

How debt relates to your credit score

Many people assume that a lack of debt is good for a credit score. In fact, the reverse is often true in a sense. A small, healthy amount of debt is good for a credit score if the debt is paid on time every month. For example, a car loan that is paid monthly shows that the borrower is reliable and responsible with debt in the eyes of a lender. Every timely payment contributes to the borrower's good credit score.

Eliminating that debt by paying it off before the mortgage application could potentially negatively impact the borrower's credit score, even if only temporarily. While the drop is often only a few points, and the credit score is likely to rise again fairly soon, paying debt off during or right before the mortgage process could have negative consequences for a buyer.

Mortgage underwriters often frown on any changes to a person's credit score in the crucial days before funding a loan. In addition, a borrower who may have a borderline acceptable credit score at the beginning of the loan process but then experiences a sudden drop at the end of the underwriting process, may not be approved for the loan or be approved at a higher interest rate.

Do you need cash on hand for the buying process?

Do you need cash on hand for the buying process?

Paying down large amounts of debt before the mortgage process might also be problematic as many potential home buyers may need the cash on hand for the home purchase. In most cases, a home buyer will need some cash when buying a home for the following items:

-

Down payment: The cash down payment is often anywhere from 3.5% of the loan to 20% of the loan.

-

Closing costs: In most cases, buyers will be expected to pay some closing costs.

-

Relocation expenses: Moving expenses can be costly depending on the distance, how much is being moved and whether or not a full-service mover is hired.

-

Remodeling: Home buyers typically make some improvements to their current home to help it sell, or they might wish to remodel their home after a purchase.

The bottom line

Paying off debt before applying for a loan can have a positive or negative effect on a home buyer's plans. It's up to buyers to identify which situation they are in. Potential home buyers (especially first-time buyers) often need guidance and advice before applying for a mortgage or for other types of loans. Borrowers should strongly consider speaking with a financial advisor or mortgage broker before making any big decisions. Additionally, home buyers who are currently in the mortgage process should maintain close contact with their lender during the process. Any financial changes of the borrower, both positive and negative, should be always be discussed and disclosed with the lender to ensure a smooth lending process.

This blog was contributed by Tony Gilbert of RealFX.com