Which debt consolidation loan is right for you? There's no one-size-fits-all answer, but we can point you in the direction to find the size that fits you.

You've spent years juggling debt on multiple credit cards with different rates and payment schedules, and you have hit your limit (literally or figuratively).

Maybe you've already consolidated your debt, are on the road to a healthier financial profile, and want to renegotiate the loan term. Or maybe you are just tired of the constant drumbeat of credit card payments, student loan payments, auto loan payments, and want to quiet it down to a manageable buzz.

Which debt consolidation loan is right for you? There's no one-size-fits-all answer, but we can help point you in the right direction to find the size that fits you.

Benefits of debt consolidation

The terms of your debt consolidation loan will depend on your credit history and other factors, like employment situation and total debt picture. You're probably looking for at least one of the following:

-

Simplicity. A debt consolidation loan turns many debts into one: one monthly loan payment, one interest rate (preferably a fixed rate so the monthly payments stay consistent month-to-month), one repayment timeline

-

Flexibility. A personal loan for debt consolidation lets you alter the terms to make monthly obligations more manageable (in other words, lower monthly payments), or to pay off a loan more quickly (getting to debt-free faster)

-

Savings. Many people are enticed by the simple prospect of saving money over time by getting into a loan with a lower interest rate than the one they have now

If you're looking for debt settlement loan help, you're in the right place. Here are the key factors to look at when you're consolidating debt:

-

What you should know about debt consolidation loan

-

The benefits of using a personal loan for debt consolidation

-

When a debt consolidation loan is right for you

-

How to find the best debt consolidation loans near you

What you should know about debt consolidation loans

It may surprise you to learn that many people who consider debt consolidation don't necessarily have bad credit scores. They are not making just the minimum payment on their credit card debt or running behind on their auto loan payments. Most are simply looking to clean up their finances or move their good credit score to an excellent credit score.

Maybe you've gotten married, both you and your partner have a couple of loans each, and now you want to buy a home. You have a credit card balance, which can also be considered high-interest debt. Debt consolidation loan, here we come!

Debt isn't the same for everyone, so the loan amount isn’t the same for everyone. Let's get an idea about what debt consolidation is and how it works. It might be the best personal loan for you.

How does a debt consolidation loan work?

Debt consolidation involves taking out a new loan to pay off one or more existing loans. The shiny new loan can come from the same source as the old loans, especially if you have a bank or credit union that you really value.

But this might also be the time to consider that maybe your debt is a hot mess of accounts spread out over a variety of places because you haven't settled down with a credit union or bank that has your best interests in mind. A debt consolidation loan is cleaning house of your assorted debts, so this is the time to consider what is the best personal loan for where you are headed and what you want to achieve financially as you pay down your debt.

Some debt consolidation loans are backed by assets, like your home or car. This is called secured debt. A personal loan for debt consolidation is usually the opposite -- unsecured debt -- and it's largely backed up by your previous history of repayment (your credit score).

What are the upsides of a debt consolidation loan?

The main reason people consolidate their loans is to streamline multiple existing loans into a single monthly loan payment. Remember that your credit card bill is also a loan you're paying interest on.

It's not uncommon to include an auto loan with other loans when you bundle your debt into a single loan, especially if the interest rates you are currently paying are really unappealing. For the most part, though, debt consolidation loans aren’t secured loans.

Because unsecured debt has higher interest rates than secured debt, this may increase your interest rate on one of your loans, but overall improve your interest rates across the board. This is the time to do the math to make sure your long-term repayment term improves your long-term savings. You know who can help you with that math problem? A loan officer at a community bank who wants to help you find the best personal loan for you.

Overall, you'll be getting a better interest rate and a clearer repayment schedule as part of the deal, since many debt consolidation loans are also low interest loans, especially compared to credit card debt.

Benefits of using a personal loan for debt consolidation

Of course, we want people to find the right place to borrow money based on their financial needs, their geography, and their values. But when it comes to debt consolidation loans, your motivation to find the right loan starts with those three reasons you might be looking to manage your multiple debt payments: simplicity, flexibility, and savings. Most often, people are looking to move their existing debt into an opportunity for a lower interest rate, so let's start there.

Better rates

Interest rate is one of the most important factors when considering any personal loan (or credit card, for that matter). You probably know the basics already. A higher interest rate means you're getting juiced for more money in the long run. Getting a lower interest rate on an existing loan — if, for example, your credit score has improved to a level where you may be offered a rate reduction — is one of the main reasons for using a personal loan for debt consolidation. So yes, find a good rate and do the math.

Consistent payment amounts

Another common goal is to gain clarity over the total amount you'll pay over the life of the loan. Some loans come with a variable interest rate: the amount paid back each month goes up and down depending on market factors. These are impossible to precisely plan around, as you're paying a different amount each month. If you have a variable-rate loan but would like to know exactly how much you'll pay every month — and when you'll be totally debt-free — you should refinance into a fixed-rate loan.

There are other factors besides a floating interest rate that can result in fluctuating monthly payment amounts. Some loans come with an unexpectedly large "balloon payment" at the end of the repayment period: a huge final bill that can come as a rude shock. If you're currently balancing multiple debts with different interest rates and monthly schedules, consolidating them into one consistent monthly payment is a smart move. Ask questions of your potential lender to learn if your repayment term includes any such surprises.

Faster repayment, lower monthly payments... or both

Maybe you're a calendar-oriented person and your main concern is adjusting your repayment timeline. Hey, we get it -- life is complicated enough. There are several reasons to do this.

Some people want to get out of debt ASAP. They've been chipping away at their balance for years and want to speed up the process to put it behind them. While the interest rate is still an important number to keep an eye on so that you don't end up paying more in high interest debt, a shorter repayment schedule is a major factor for those whose main goal is to sprint to debt-free status. If you're positioning yourself for a future home purchase, especially one in the not-so-distant future, this is exactly what can get you to an excellent credit score.

And some people need an extended repayment period — in other words, lower monthly payments, even if it takes a little longer to pay down. This is obviously a major factor for many people in the process of consolidating debt.

Sometimes it's possible to hit both goals. If you consolidate into a loan where you have a lower monthly payment but keep paying the previous payment amount when you can, you might be able to get out of debt faster while still paying less in the long run. Win-win!

Flexibility and transparency around the repayment period is as big a factor as interest rate for many people looking to refinance. Make sure to keep both in mind.

When is a debt consolidation loan right for you?

Debt consolidation loans work well for people with one or more existing loans that they want to refinance in order to pay a lower interest rate, lower their monthly loan payments, or both.

Consider the reasons why people consolidate debt. Some people need simplicity: turning many debts into one. Some are going for flexibility: altering the terms to make monthly payments more comfortable. Many people are enticed by the simple prospect of saving money over time. Again, many sizes, many reasons, many goals, but all worth considering to determine which option is right for you.

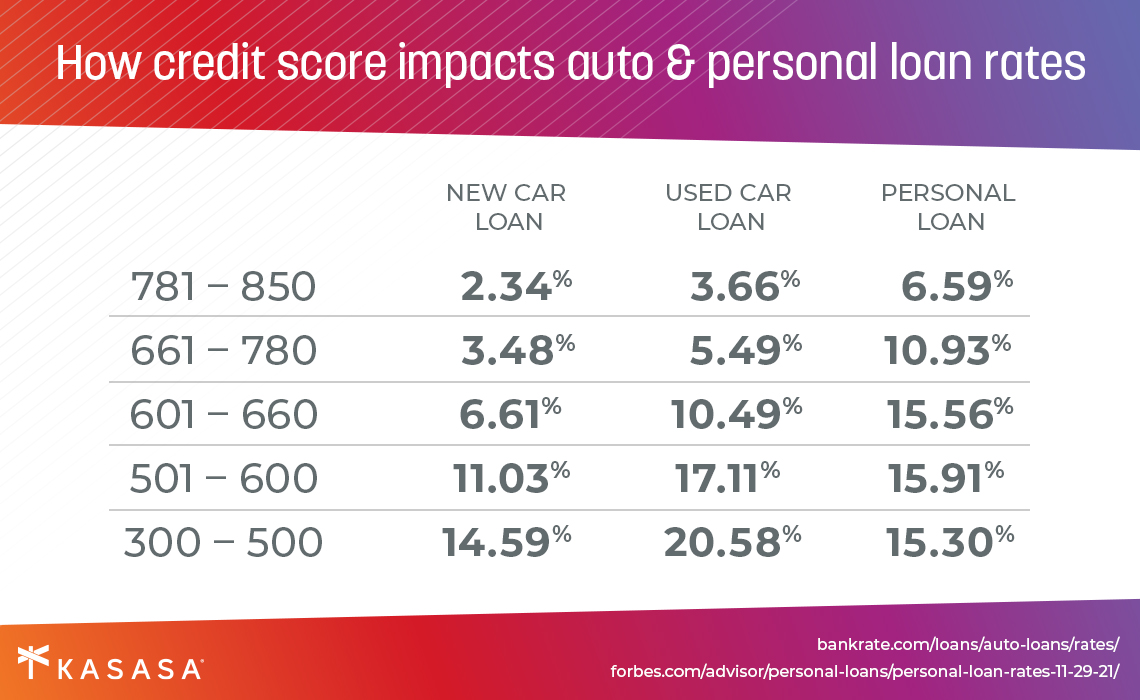

As with any loan, the terms will depend on your credit history and other factors, like employment situation and total debt picture. You'll go through the credit approval process, so it's a good idea to find out what your current credit score is and look at all the places where you may have outstanding debt.

The why of a debt consolidation loan is to reduce the total amount you'll pay back, or to simplify repayment. The when depends on you. If you're overwhelmed by too many credit card bills, or if you've recently had a life change that makes it easier to pay off your past loans, debt consolidation might be the right next move for you.

A personal loan used to refinance one or more pre-existing loans can help save you money and put you on a risk-free path to getting out of debt. Take a look at your financial situation and goals. You want to pay close attention to the rate, monthly payment amount, and repayment schedule of a debt consolidation loan offer.

Want to be debt-free as quickly as possible? Look for a loan with the shortest possible repayment period.

Rate shopping? Get a loan with a similar repayment period but a lower interest rate.

Looking for more clarity in your repayment terms, while also trying to lower your monthly payment? Take out a debt consolidation loan with a fixed interest rate and a longer repayment period.

The only debt consolidation loan with Take-Backs™

We're going to throw one more consideration into the mix. Once you have your debt consolidation loan in place, what if you stumble into an unexpected expense, like a friend's wedding you don't want to miss, or a new apartment where you have to provide your own washer and dryer? Remember, you're trying to eliminate multiple debts, and you've just combined your debt into a single monthly payment.

A Kasasa Loan® includes a unique feature that lets you tap into the extra payments you've been making and use that money without having to consider another loan.

Hey, you're enjoying the simplicity, flexibility, and the savings your debt consolidation loan has given you. Don't you want to stay focused on those goals even when (expensive) surprises pop up?

A Kasasa Loan gives you total control over these variables, and a new perspective on how they interact over time. Our unique dashboard tool lets you visualize the life of your loan in terms of both time and money, and our unique Take-Back® feature lets you reclaim money you've already paid toward your loan, giving you access to funds when you need them most

Get started with a Kasasa Loan for debt consolidation here.