Understanding how to manage debt and building a debt management plan enables you to pay down your debt and improve your financial and personal well-being.

It's curious that people often feel stress about money — about 75% of Americans say so. In reality, money is a tool you use to pay off credit card debt, or student loan debt, a car payment, or any personal or home expense. What really causes the stress is debt.

While your economic situation may change over time based on income, employment, expenses, and financial obligations, your debt management determines whether you are using the tool you have — money — to dig your way out of debt. The metaphor makes sense. Many of us have found ourselves in a financial hole when there is more money going out than money coming in. Truth is, you're not digging a hole: You're in the hole trying to dig your way out. If you picture yourself literally in a hole, digging more is only going to make the situation worse.

Understanding how to manage debt and building a debt management plan will enable you to pay down your debt and improve your financial and personal well-being. Depending on how deep your financial hole is, you may find you are building yourself back up a little at a time to lift you to where you want to be: back above ground.

How debt affects your well-being

Perhaps you are constantly being reminded how far down in the debt hole you are. Your credit score has taken a hit. The interest rate on your credit card has increased. Every statement reminds you how long it will take to pay off your debt if you only make minimum payments. Even a monthly reminder about your debt repayment on your student loan may be that voice telling you that you are not where you want to be financially. Is it any wonder why you feel stress about finances when the reminders are non-stop?

You've probably figured out that getting into debt is easier than getting out of it. Maybe you've been hit by an employment gap, or an unexpected expense. Perhaps your student loans are coming due soon, or you simply enjoyed a few too many nice-to-haves on your credit card. Everyone gets into debt the exact same way: more money goes out than is coming in. This is where we develop stress about debt.

Of course, not every purchase is as exciting as your autographed replica of the Starship Enterprise that you splurged to buy during the online fan auction. We also find ourselves accumulating debt for car repairs and adult orthodontics. It gets stressful in tangible, physical ways that affect our overall well-being when acknowledging the size of your student loan debt or your credit card balance takes away from the reward of finishing college or displaying your movie memorabilia. Keep in mind, money is your tool and you are using it to achieve what matters to you. Be proud of your money.

The first step in alleviating that stress and building a plan that develops confidence in your financial health is to find ways to turn that equation around and have more money coming in than is going out. Easier said than done, right? If you are able to make more than your minimum payment, you are one step closer to eliminating the stress of your debt, but also improving your financial well-being. If you even have one monthly payment that is weighing on you, consider where you can trim other expenses to be able to get your debt management plan where you want it to be.

If you still feel like there are more outgoing payments than incoming finances, why not ask for some help? Credit counseling services and various forms of debt relief can provide crucial assistance. Getting set up with a debt management program won't suddenly open the floodgates of income, but recognizing when you need help getting out of debt may be a far less painless step than being hounded by a creditor or even facing bankruptcy.

Keep in mind that there are both responsible and unscrupulous options for debt relief, so find a credit counselor that is reputable and whose goal is to help you climb out of that hole in which you find yourself.

Different strategies to pay down debt

If you've ever shoveled snow, you know it takes more energy than you expect. If it happens to be snowing while you're shoveling, you might look back at your sidewalk and wonder if you really accomplished what you hoped you would. You feel daunted. While you'd love to wait until it stops snowing, you may not have that luxury any more than you can put off paying your outstanding debt.

The two main strategies for debt repayment both have winter-weather nicknames. Commonly known as debt avalanche and debt snowball, each strategy is designed to eliminate one debt at a time and help lift you out of that debt hole. Which method is most effective may be different for you than it is for your neighbor across the street with the snow blower.

A debt avalanche looks at all your debt and recommends you first tackle the one with the highest interest rate. This is rarely your home mortgage debt, since that is secured debt and often has a lower interest rate. Be sure to look closely, though. If you have multiple student loans, you likely have a variety of interest rates, so you should look at each one separately. The plan: Pay as much as you can on the debt with the highest interest rate, and the minimum on everything else.

The debt snowball suggests a debt reduction strategy starting with the smallest debt on which you owe the least. Put all your extra effort into that debt, and just the minimum on everything else. Once you erase that debt, move on to the next smallest, and roll the full amount you were paying on the previous debt into the effort.

With either of these plans, keep in mind that you may have to shovel while it's still snowing, so wherever possible, limit accumulating any new debt as you go.

Your bigger debt picture

If you have a variety of debts (student loan, personal loan, credit card debt, mortgage, etc.), you ought to consider how much each is costing you and which you should try to knock out first. Again, it may be worth contacting a credit counseling agency just to make sure you are picking the best option for your current financial state, or your long-term financial well-being.

If you have a manageable amount of debt still somewhat under your control but you'd like to fill in the hole a little faster, a debt consolidation loan might provide you with a way to organize your debt into a single payment. These loans will check your current credit score (which may experience a dip), but rather than trying to determine which debt to eliminate first, this lumps them into a single debt payment. This may be best if you are still able to climb out of the hole by yourself.

But when your financial situation finds you deeper in debt, and new loans are just adding more bad debt, you need a financial plan that gives you additional options to help your money do whatever lifting it can. Whether the credit counseling agency can help you with a debt settlement, negotiating a lower interest rate on your credit cards, or keeping the debt collection hassles away, resolving your debt in a manageable way gives you the confidence you need to improve your financial well-being. Knowing you are not down in that hole alone might help your overall well-being, too.

Don’t dodge the debt collectors

Okay, when you reach this point, the hole is already pretty deep. Regardless of which strategies you might try, there are a few truths to accept at this point. Your debt isn't going to improve by prolonging the tough conversations, and every step you take towards debt payoff is one step closer to your own financial wellness. Debt collection doesn't need to be seen as a personal attack on you, just the point of more money going out than coming in. It's time to bring in some help.

Acknowledging your debt can lead you down several paths, including discovering small ways to pay your debt faster, reviewing your budget, examining your credit, working with a financial credit counselor, and providing debt management guidance. Don't put off speaking to a debt collector to avoid the debt, but do put together a plan for managing debt before speaking to the creditor. Know what information to share, and which information you can keep private.

If you reach the point where you're facing a legal debt settlement, it will be best if you know where you stand, what you owe, what you are able to pay, and what options are available to you.

Believe it or not, asking for help is not the hardest part of resolving your debt. In fact, it may provide relief to the stress debt is putting on you. While you may not want to talk with others about how to manage debt, you might find out that there are ways to get to a place of improved financial well-being. You might also realize you are not the only person who has been in this hole, and other people may be able to show you the best way to get out of it.

Tips for maintaining minimal debt

Congratulations! You're filling in the hole. Bit by bit, you are improving your financial well-being. Alternatively, you might also be at the start of your financial journey, whether you are renting your first apartment, starting your first full-time job, or hoping to purchase your first car.

Keep in mind that there is such a thing as good debt. Establishing good credit requires you to have debt, and to show off your strong debt management abilities. You may have a "thin credit file," which means you have not yet been in a position to make a recurring, monthly payment on a personal loan or credit card. Look at it this way: If you're going to dig a small hole to establish your credit or maintain your good credit, refill the hole with a new plant or sapling that will improve your financial well-being over time. Don’t simply pay down debt — use it to grow and thrive.

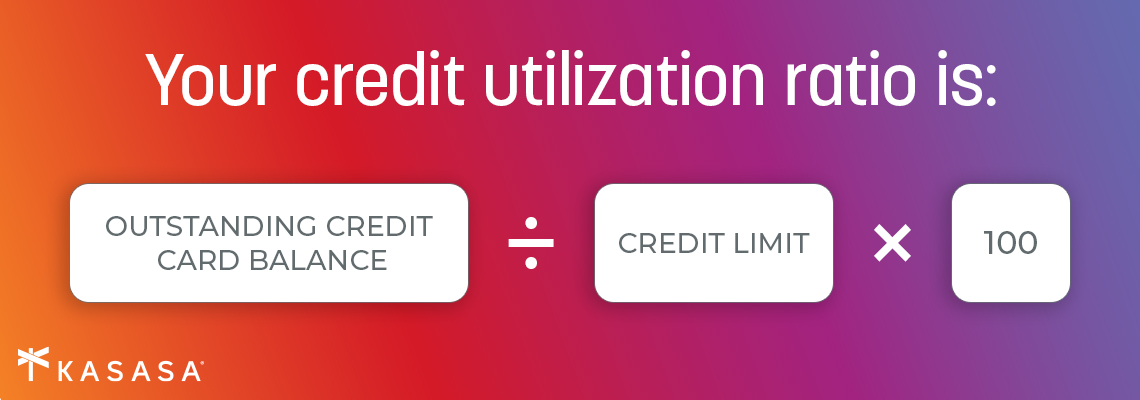

Whether you are whittling down your debt or just starting to build your credit history, always keep tabs on your credit report. This includes reviewing it frequently and reporting errors that may be impacting your good credit. When you do have debt, keep your credit utilization under 20% whenever possible. Pay off your credit card balance in full each month — and don't sweat it if you aren't doing that yet. You’ll get there.

Experts will tell you that having a budget helps you control your spending and your debt. Having a monthly budget is only helpful if you are looking at it and tracking your spending.

If you know that's not your style, you at least need to have a clear picture of where all your money lives and moves. Having money spread out in a variety of accounts and locations — in traditional accounts, neobanks and P2P payment apps on your phone, employer-funded investments plans, and student loan payments from when you were in college — might make moving money and paying bills convenient, but it's good to find where you might have extra financial resources and where those dollars could be applied to lower your debt. Knowledge is power, and you cannot use your best tool — your money — if you don't have a good grasp of where it's going.

Once you have the debt under control, use your money to amp up your financial well-being. Contribute to your retirement, create an emergency fund for life's little surprises, and look for ways to lift your credit score from fair to good and from good to excellent. Keep using your money to see your financial well-being improve, paycheck after paycheck, year after year.