Money management is a crucial skill: cultivate the best mindset and best practices to maximize your financial well-being and keep debt to a minimum.

Do you know what a money mindset is? It can mean different things for different people. In the simplest terms, your money mindset is the way you think about money, and the beliefs you hold about it. Your attitude towards money largely shapes how you earn, spend, and save it.

Whether or not you’re directly motivated by making bank, you almost certainly have a money mindset — even if you don’t think about it consciously. We’re here to tell you that the smart money is on knowing thyself: figure out how your relationship to moolah works, and you’ll eventually feel like you’ve gained a new superpower. The more financial tools in your toolbox, the better your life.

Whether you’re trying to answer basic money questions or tackle big financial goals, money management is a crucial skill that you can build from any starting point. Read on if you’re interested in getting your money right: cultivating the best mindset and best practices to maximize financial well-being and keep debt to a minimum.

Types of money management strategies

There are different types of personal money management strategies, depending on your past behaviors, your current financial picture, and your future goals.

The past

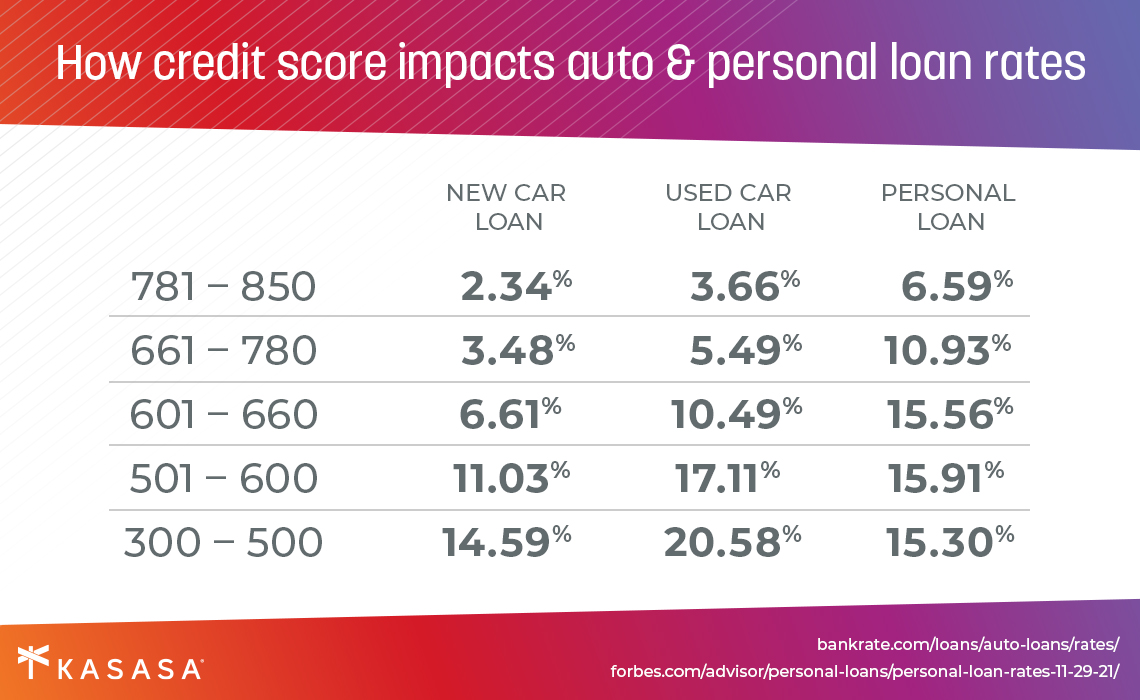

One key facet of your overall financial situation is your credit score. This three-digit number is mainly a record of how consistently you’ve paid back your credit card and other loans or debts in the past.

Let’s get one thing out of the way up front: A low credit score does not mean you aren’t able to improve your money mindset and get your money right. In fact, you’re the type of person that will benefit most from reading further!

The present

No matter what your credit score is, there’s no time like the present to make a jump on improving things. One way to think about which money management strategies might be right for you is to begin by analyzing where you’ve been in the past — especially areas where improvement is called for.

Let’s say you bought your current car at a dealership and didn’t have the time or the energy to research the best possible auto loan rate. Plus, your credit score wasn’t so hot back then, but it’s a little better now. Reflecting on that past decision, now you can arm yourself with information about refinancing auto loans, and then go on and find yourself a loan with a much better rate, and you greatly improve your cash flow virtually overnight. That’s getting your money right.

The future

This is the fun part. Where do you want your financial roadmap to take you? Do you want a well-stocked emergency fund, cash flow available for occasional indulgences, or a savings account that holds more than the leftovers of your last paycheck? Depending on what your tomorrow looks like, you should be thinking about your money decisions today.

If you’d like to retire on a fat pile of money at some point, you can start investigating money market funds or savings accounts that incentivize leaving your wealth mostly untouched.

If you’re more inclined to spend it if you got it, on the other hand, you may plan for the future by looking into checking accounts with cash back rewards.

Are you a spender or a saver?

That brings up an important distinction, one that ties into your money mindset. Some people think of their bank account as a vessel, a bucket that gets filled with money on payday and subsequently spent. Those people are spenders. The other major type views their bank account as an organism, something that should grow over time rather than go from full to empty like a gas tank. Those people are savers.

The world doesn’t break down into black and white like that, of course. You’re probably somewhere on the grayscale in between. But it’s important to realize your own tendencies, what you’re cool with keeping, and what you want to change. Often, this means moving more of your thought patterns and behaviors from the “spender” to the “saver” category by doing things like establishing a budget or checking out personal finance classes.

Keeping debt to a minimum

Getting your money right and acting like a saver versus a spender isn’t only about your savings account, either. Debt is a central feature of our society, something you can’t easily live in America without experiencing. We’re talking everything from your credit-building credit card you put the odd coffee on to the mortgage that protects your claim to the roof over your head.

Getting a clearer picture of your overall debt picture and then making proactive choices to improve it is a strategy at the core of getting your money right. Chances are very high that you have some form of credit card debt right now, probably running balances on multiple cards with different schedules and minimum payments. Let’s not even get into student debt, auto loans, or that mortgage.

Consolidating debt or refinancing an existing, less-than-stellar loan is a powerful first step to get a grip on your finances if you’re on the debt-heavier side of your journey. (Pro tip: A Kasasa Loan® is a great tool designed to do just this: help you borrow smarter instead of racking up more high-interest debt. Get started with a Kasasa Loan for debt consolidation.)

Get your money and your mind right

No matter what your situation is, you use money. You might juggle multiple bank accounts, which means different account balances, interest rates, monthly statements and bills, and other fun stuff like that to keep straight at all times. As a result, you understandably might lack a good overview of what your finances really look like, the overall picture of how much you have (your savings) versus how much you owe (your debt).

Sounds stressful! But if you’ve read this far, you’re already on the way out of this predicament.

Let Kasasa® be the light at the end of that tunnel. If you’re trying to inch from “spender” to “saver,” to get out of debt faster and watch your savings account swell over time, Kasasa has exactly the tools you need to get there.

Maybe you need a high-yield savings account, a reward-packed checking account, or a personal loan that will help you consolidate your existing debt and make it a lot easier and more straightforward to manage. No matter your specific needs, Kasasa and our national network of community financial institutions are here to help you get your finances in focus, and to be proud of your money.