Deposit accounts provide the cash to make loans to borrowers. Here’s a look at what goes into the calculation so you can shop for the best rates for you.

You’ve probably seen a few surprising interest rates cross into your field of vision, which might have you asking questions. "How do you get an auto loan for an interest rate less than 2%? And, oh my, you can earn 3% interest on a savings account? How does that work?"

At its core, banking is all about bank accounts providing cash, which financial institutions use to make loans. But since there’s much more to it than that, here’s a look at what goes into the calculation so you can shop for the best rates for you.

Interest rates on loans

How do banks and credit unions determine the interest rate you pay on your loan (APR)? There are several factors.

-

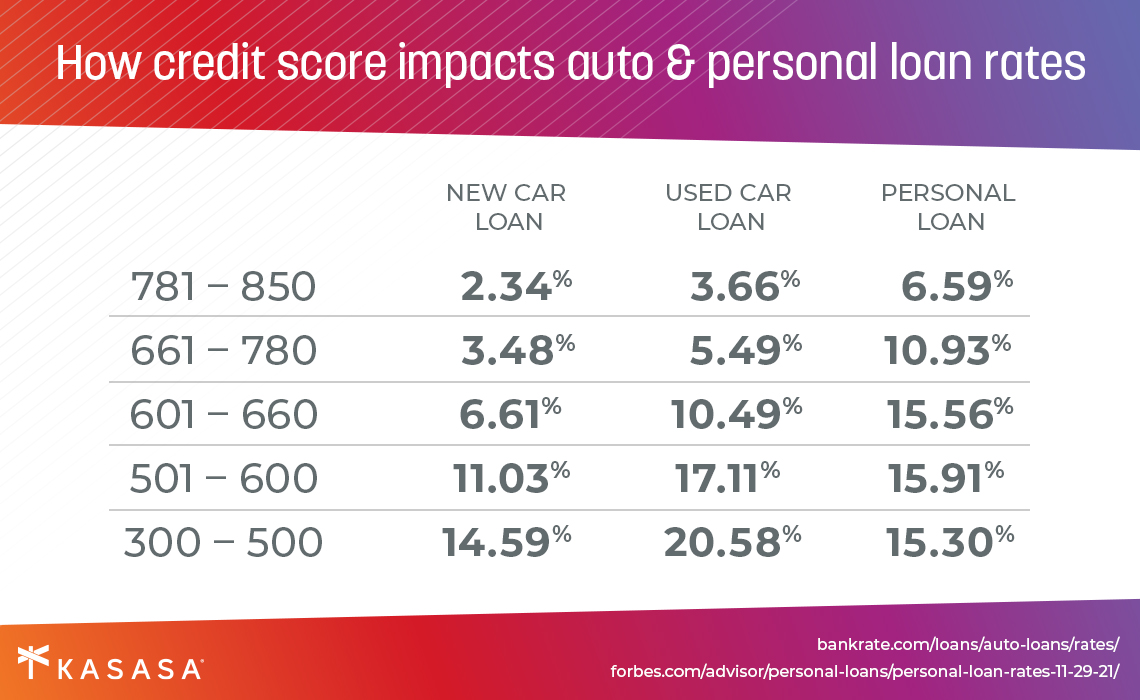

Your credit score: You might see an advertisement for a great rate on that gets you in the door. Before you shop for a new set of wheels, it's important to understand these are attractive promotional rates that go to customers who are deemed the most creditworthy. That is, they have built a good history of repaying their debts, which tells the lender that the customer is likely to repay the money. Luckily, it’s easy to find out where you stand ahead of time. Check your credit reports and get a free estimate of your credit score.

-

Federal Reserve: When you hear rumblings of “the Fed” raising rates, it’s time to pay attention — that’s because lenders follow suit, setting their own rates relative to that of the Federal Reserve. This affects your interest rate for credit cards, car loans, a home equity line of credit (HELOC), and, to a lesser extent, mortgages.

-

The market: Naturally, your bank or credit union will be keeping a close eye on the competition. They’re also looking at larger market forces, such as gross domestic product, inflation, the yield curve, as well as what the local market is doing. In a slow market, banks may dial down rates a bit to stoke more borrowing.

-

The type of loan: Most banks and credit unions will offer a wide range of loans. The most common are auto loans, mortgages, personal loans, home loans, and student loans. Some of these loans have items that can be repossessed in case the borrower is unable to pay (like the auto loan). That makes the loan less risky for the lender.

-

The duration of the loan: For some loans, you will have an option for how long you would like to take to pay it back. An easy example is a mortgage. You could get a 10-year, 15-year, 20-year, or 30-year mortgage. Each would slightly change your interest rate.

Interest rates on checking and savings accounts

Banks and credit unions offer these types of accounts in order to attract deposits. "Deposits" is banking jargon for your money that they will hold onto. This is one of the cash sources a bank or credit union will use to make loans. By offering checking and savings accounts with higher interest rates (APY) they bring in more deposits and can then make more loans. If a bank or credit union doesn't need more deposits, they might lower the rate they offer. This will save the institution money as they aren't having to pay out as much interest.

Interest Rate on CDs

A Certificate of Deposit (CD) is something a bank offers in order to guarantee that they will have access to your funds for an extended period of time. In return, they typically offer a higher interest rate than they would on either their checking or savings accounts. Of course, you only get that rate if you keep your money in the CD for agreed upon amount of time. If you withdraw your money early, then you incur a penalty. Interest Rates on CDs are set based off of several factors.

-

The type of CD: There are several types of CDs out there, each with different rules and rates associated with them. Some examples are the Traditional CD, the Bump-up CD, and the Zero-coupon CD.

-

The duration of the CD: CDs typically fall into three buckets: short-term, mid-term, and long-term.

-

Short-term: Between 3 and 12 months and a tiny amount of interest.

-

Mid-term: Between 1 and 3 years and a slightly better interest rate.

-

Long-term: Between 4 and 6 years and the best CD rates.

-

The rate which the bank or credit union sets: CDs are ultimately priced by the institution that issues it. Like we learned in the section on saving and checking accounts, banks and credit unions use this money to make loans. CDs are great for banks and credit unions because it guarantees access to the money for a certain amount of time and they can set the interest rate in anticipation of what the Federal Reserve will do.