College is getting more expensive every year. Most students choose to take on massive amounts of debt. But there is a better option, Federal Pell Grants.

Despite rising higher education costs and student loan debt, there is a baffling amount of federal student aid that goes unclaimed each year.

A NerdWallet analysis showed that high school graduates left $2.7 billion in free college funding on the table in 2014.

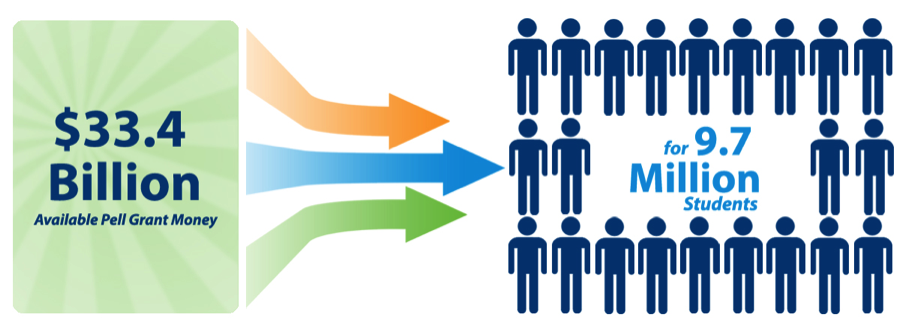

One of the key components of financial aid for students comes in the form of Pell Grants. Pell Grants, provide over 9 million low and middle-income students each year with much-needed college funding.

via @SimpleTuition

What is a Pell Grant?

First, it’s important to point out that while Pell Grants are federally funded, they are not a federal loan. Which means they don’t have to be repaid!

Pell Grants also fall under what is called an “entitlement grant” – meaning they aren’t tied to a specific school or geographical location, similar to the way scholarships are set up. If you qualify for a Pell Grant, you can take your entitlement grant with you to nearly any college or university.

The grant will come to you as a tax-free subsidy. In cases where you don’t utilize your entire Pell Grant for tuition costs, your school will pay you the remainder of your grant; however, any leftover money must be reported on your taxes.

How much student aid can you receive from a Pell Grant?

Your Pell Grant amount will depend on several factors:

-

The current Pell Grant maximum

-

Your EFC (we’ll cover that more in the next section)

-

The cost of attendance

-

Your enrollment status

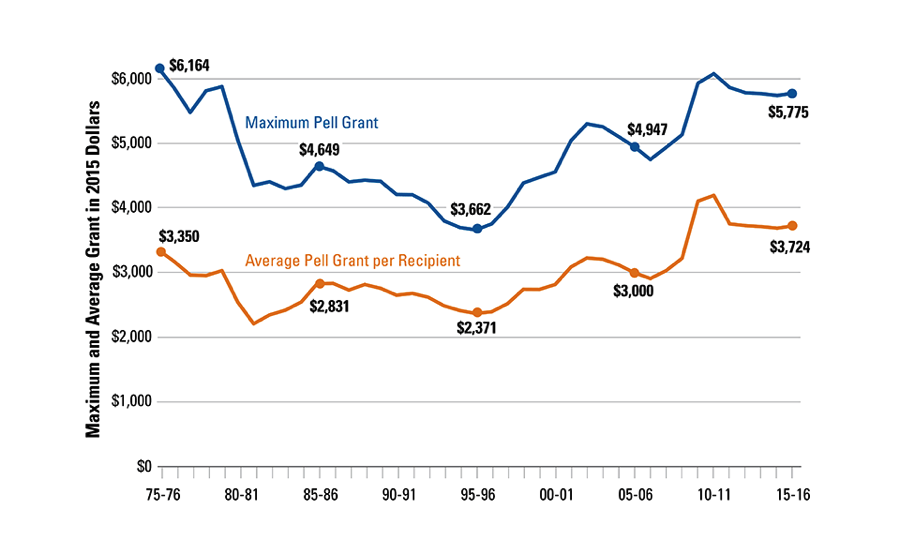

For the current 2017-18 semesters, the maximum Pell Grant a student can receive is $5,920.

via @Collegeboard

The above graph shows the changes in both maximum amount awarded and average grant per student over the past 40 years.

How to know if you qualify

Qualifying for a Pell Grant depends on your EFC.

To give some perspective, Pell Grants are typically awarded to students whose families make less than $50,000 a year in pre-taxed income. Any family making less than $24,000 a year has an EFC of 0 and stands an excellent shot at being awarded a Pell Grant.

Not sure what your family’s EFC is? No problem.

Fill out a Free Application for Federal Student Aid (FAFSA) to see if you qualify for a Pell Grant, or any of the other $150 billion in federally funded loans, grants, and work-study programs offered each year.

via Bankrate

Steps to apply

-

Start by filling out your FAFSA – aim to have this submitted as close to January 1 as possible.

-

Once your FAFSA application is submitted, you’ll receive a student aid report (SAR).

-

Your SAR will tell you how much aid you will receive, what programs you’re eligible for, as well as your EFC.

-

-

Once you receive your SAR, respond ASAP.

-

Pell Grants are served on a first-come-first-serve basis. If you delay response, you risk losing your grant

-

-

Your Pell Grants and student aid will be paid out directly to your school 2-4 weeks prior to the semester.

-

Any leftover funds will be dispersed to the student and must be reported on your taxes.

Tips On Applying For Pell Grants

-

Reapply early every semester - The earlier you submit your FAFSA, the better chances you have of receiving aid.

-

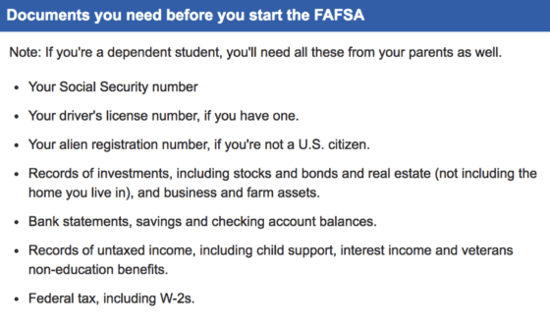

To save time, make sure you have all your documents together before you apply.

via Bankrate

-

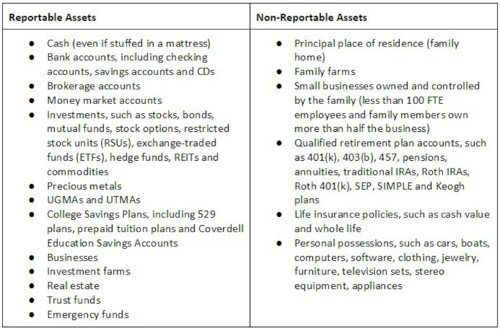

Get a clear understanding of what assets are reportable vs. non-reportable

via Cappex

-

Transfer or spend reportable assets to maximize possible student aid. Examples:

-

Pay down debt (mortgage, credit cards, etc.)

-

Max out your Roth IRA or increase contributions to 401K

-

Purchase supplies for student (laptop, books, etc.)

-

Put money into expenses you were already planning for (house remodeling, new car)

-

-

Transfer or spend student assets first then move on to parents.

-

Student assets are assessed at a higher rate than parents 20% for students vs. 5.6% for parents. So for every $10,000 in assets the student has, the available federal funds are decreased by $2,000.

-

-

Even if you’re in school half time you should still apply for a Pell Grant. You won’t receive as much funding, but every bit helps.

Other types of financial aid

Pell Grants are just one of many ways to help with the cost of college. If you don’t qualify for a Pell Grant, consider these other options:

-

FSEOG - You may be eligible for a Federal Supplemental Education Opportunity Grant .

-

Work-study jobs – these jobs usually have a civic or community focus to them, and tend to be with the school itself or certain approved locations. They offer a way for lower-income students to earn extra money to pay for school.

-

Scholarships - Similar to grants in that scholarships don’t require repayment. The difference is that they are awarded through individual institutions or private organizations.

-

Check out these five scholarship websites that could help you find a match.

-

-

Federal Loans (Subsidized) – these loans are for students that need financial aid. They are favorable because the U.S. Department of Education pays your interest while you’re in school and for 6 months after you graduate.

-

Federal Loans (Unsubsidized) – these are backed by the Federal Government, but the student is responsible for paying interest through the life of the loan.

-

Private loans – offered by banks to help fund high education expenses, private loans tend to have less favorable terms like higher interest rates.

No matter what your financial situation is heading into college, it’s important to weigh your financial aid options. A great way to begin this process is by filing a FAFSA.