A few minutes searching with Kasasa Care and GoodRx can save you up to 80% on the over-the-counter medications you regularly reach for.

For those nearing the age of 65 (the Medicare eligibility age), let us be the first to wish you a happy early birthday! Party hats and cake slicing aside, you’ve probably also been receiving some (okay, a lot) of information about Medicare — and, as usual when choosing a health plan, we understand it can get quite overwhelming.

When it comes to your health coverage (especially Medicare), you shouldn’t stay in the dark. There’s a lot of options — and letters — to choose from, but we hope this handy 101 guide makes this milestone decision a little easier.

What is Medicare?

Medicare is the federal health insurance program for people who are in the following Medicare eligibility groups: those 65 years of age or older, people who have certain disabilities that currently receive disability benefits — like people with end-stage renal disease and amyotrophic lateral sclerosis (also known as ALS).

How does Medicare work?

You can begin the Medicare enrollment process three months before your 65th birthday. If you’re currently receiving Social Security benefits, you don’t need to do anything — you’ll be automatically enrolled in Traditional Medicare, or Original Medicare (Parts A and B), the month you turn 65. If you’re not currently receiving Social Security benefits, then you can sign up for Original Medicare coverage by calling the Social Security Administration, or visiting their site online here. But if you’d rather a different Medicare plan (like Medicare Advantage) or Medicare Supplement, keep reading — we’ll get into those specifics, too.

How many people are enrolled in Medicare?

Medicare provided health insurance coverage for 60 million Americans with Medicare eligibility.

What are the parts of Medicare?

Medicare is uniquely divided into four parts: Parts A, B, C, and D. There’s Original Medicare (Parts A and B), and Medicare Advantage (Part C). If you’re already confused, hang tight — we’re going to break down the types of coverage next.

-

Medicare Part A is hospital insurance. These benefits include inpatient hospital stays, care in a nursing facility, hospice care, and some home health care. These benefits do not cover regular doctor visits or prescription drugs. To enroll, you can get Part A directly from the government, or through a Medicare Advantage plan. (More on that later.)

-

Medicare Part B is medical insurance. These benefits include certain doctors’ services, outpatient care, labs, medical supplies, and preventive services. To enroll, you can get Part B directly from the government, or through a Medicare Advantage plan. (Stay with us, it’s coming.)

Together, Part A and Part B are referred to as “Original Medicare,” or “traditional Medicare,” so you’re covered if you need to go to the hospital or just have a checkup with your primary physician. Medicare benefits are a bit different from what you might have been used to with your previous health coverage — so if you find you need extra coverage, there are Medicare supplement plans to look into, as well as...

-

Medicare Part C, or Medicare Advantage, is privatized, all-in-one health insurance. These benefits are the alternative to Original Medicare, bundled together with Parts A, B, and usually D. These Medicare benefits also sometimes cover dental care, vision care, over-the-counter items, and other specialized health needs. The requirements for Medicare Advantage enrollment are that you must have Part A and Part B Medicare, and also live within the service area of your Medicare Advantage plan.

-

Medicare Part D is prescription drug coverage. These prescription drug coverage benefits include your prescription drugs, which are not covered in Parts A and B. To enroll, you can get Part D through a private insurance company that offers prescription drug coverage on its own, or through a Medicare Advantage plan (almost there!).

-

A Medigap plan (also known as a Medicare Supplement insurance plan) is extra health insurance you can buy from a private company to pay for health costs not covered by Original Medicare. Medigap plans are offered by private insurance companies. Designed to fill in the “gaps” in your overall Medicare costs, a Medigap policy could be beneficial for your budget.

Original Medicare or Medicare Advantage?

Deciding on a Medicare plan during your enrollment period is a huge step, because there are a lot of factors to keep in mind. Here are a few of them:

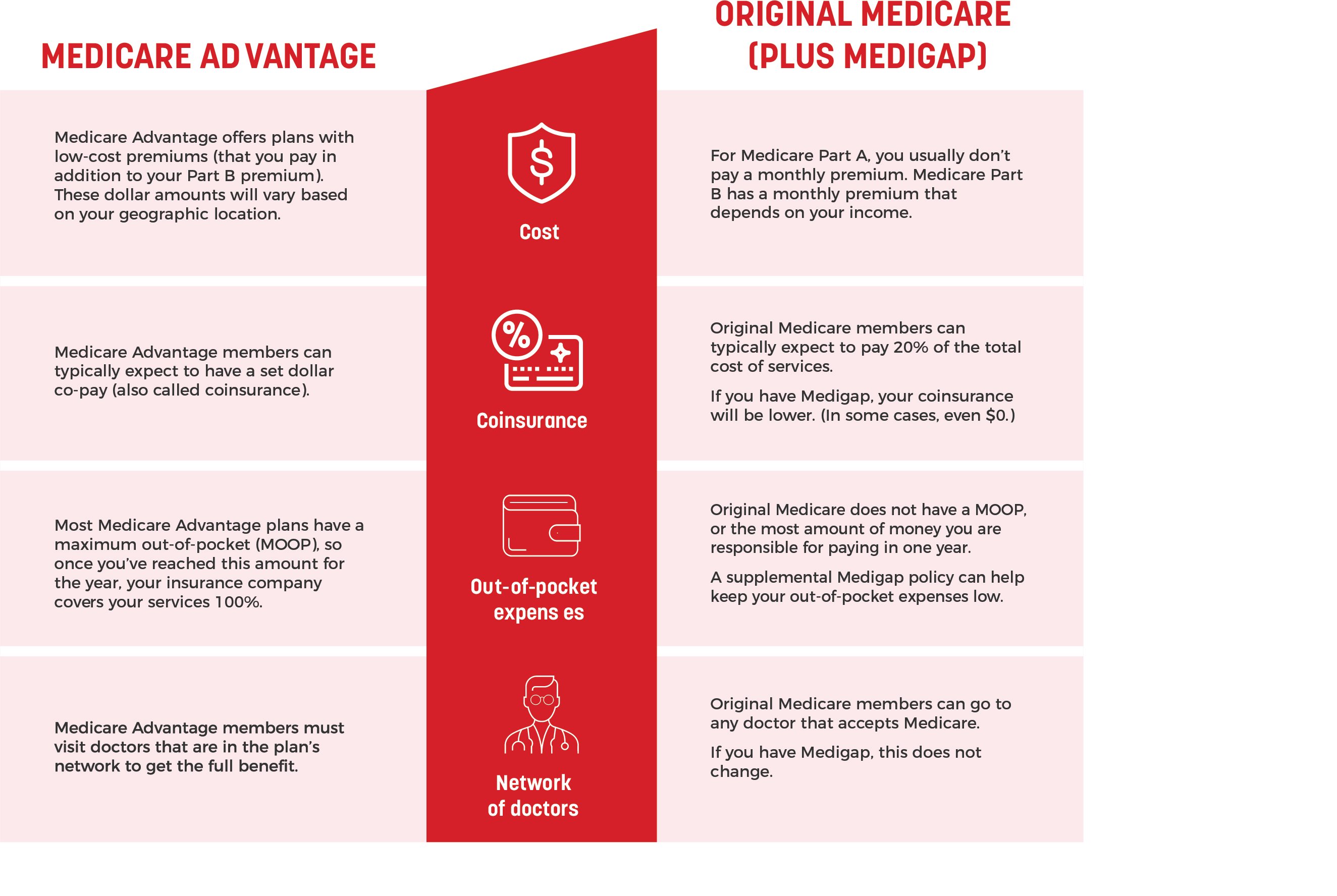

Cost

-

For Medicare Part A, you usually don’t pay a monthly premium if you (or your spouse) paid enough in Medicare tax while you were working. For 2021, Medicare Part B has a standard monthly premium amount of $148.50. So, if you opt for Original Medicare (instead of just Part A or just Part B), you can expect to pay around that much per month for your health care — unless you decide to add on Medicare Part D or a Medicare Supplement plan.

-

Medicare Part D, or prescription drug coverage, is an additional cost, with a monthly premium, yearly deductible, co-pays, and coinsurance, and is offered by private insurance companies. A Medicare prescription drug plan can help offset the rising costs of your prescription medications.

-

If you opt into a Medicare Supplement (or Medigap) plan, those benefits are an additional cost, with a monthly premium, yearly deductible, co-pays, and coinsurance.

-

Medicare Advantage, on the other hand, offers plans (prescription coverage and other supplemental benefits included) with low-cost premiums — sometimes as low as $0. However, these dollar amounts will vary based on your geographic location.

-

Both plans have premiums, co-pays, deductibles, and coinsurance.

Coinsurance

-

Original Medicare members can typically expect to pay 20% of the total cost of services.

-

Medicare Advantage members can typically expect to have a set dollar co-pay, so you can plan ahead and budget accordingly.

Out-of-pocket expenses

- An Original Medicare plan does not have a maximum out-of-pocket (MOOP), or the most amount of money you are responsible for paying in one year.

- Most Medicare Advantage plans have a MOOP, so once you’ve reached this amount for the year, your insurance company covers your services 100%.

Network of doctors

- Original Medicare members can go to any doctor that accepts Medicare.

- Medicare Advantage members must visit doctors that are in the plan’s network to get the full benefit. This is similar to an HMO, or a health maintenance organization, in which the plan requires you to stay in-network for your health care.

Who is eligible for Medicare?

No matter what, people who are 65 years of age or older have Medicare eligibility. You must also be a U.S. citizen (or lawfully present), and you or your spouse must have paid Medicare taxes for at least 10 years.

For those younger than age 65, you qualify for Medicare coverage if you have certain disabilities, end-stage renal disease, and amyotrophic lateral sclerosis (also known as ALS). You must have been receiving Social Security disability benefits for at least 24 months prior to enrollment.

How can I enroll in Original Medicare?

Enrolling in Medicare is a little different than the Open Enrollment period you might be used to with your previous health insurance coverage. Your 65th birthday gift is automatic enrollment and eligibility into Original Medicare (Part A and Part B) if you’re receiving Social Security retirement or Railroad Retirement benefits. The government will send you a welcome letter with all of the details of your Medicare benefits in lieu of a birthday card. (It’s the thought that counts, right?) If for some reason you have not received your red, white, and blue Medicare card in the mail, contact Social Security for your membership information.

Additionally, if you’re not automatically enrolled, you have the opportunity to sign up during your Initial Enrollment Period (IEP). Your Initial Enrollment Period is a seven-month stretch of time when you can enroll in Medicare Parts A and B for the first time, and it begins three months before your birthday, lasts throughout your birth month, and ends three months after your birthday. You can also enroll in a prescription drug coverage plan during this time, too.

When can I enroll in Medicare Advantage?

If you’d like to enroll in a Medicare Advantage Plan, or Medicare Part C, make sure you:

-

Already have Medicare Parts A and B.

-

Have checked to make sure you live in the Medicare Advantage plan’s service area.

-

Do not have end-stage renal disease.

Medicare Advantage enrollees can complete the enrollment process during your Initial Enrollment Period. But you can also enroll during:

-

The Annual Election Period. This is the time in which you can change your plan or enroll in Medicare Advantage. Your benefits will go into effect on January 1 of the upcoming year.

-

A Special Enrollment Period, which is when you can enroll in a Medicare health plan after certain qualifying life events occur, like retirement, losing employer-covered insurance, or even if you move out of your plan’s service area.

-

The Medicare Open Enrollment Period. The Medicare Open Enrollment Period is the time in which those that are already enrolled in a Medicare Advantage plan have the opportunity to change plans.

How can I get help to pay for my Medicare plan premiums?

If you need assistance in paying for your Medicare premiums, you may be able to qualify for the Qualified Medicare Beneficiary (QMB) Program. This program is one of four Medicare Savings Programs that allow you to get help from the state you live in to pay for your Medicare premiums. However, a Medicare Savings Program is just for Original Medicare, and qualified Medicare beneficiaries can expect to receive payment assistance for Part A premiums, Part B premiums, deductibles, coinsurance, and co-pays.

To be considered a qualified Medicare beneficiary and receive this benefit, you must have:

-

An individual monthly income limit of $1,060.

-

A married couple monthly income limit of $1,430.

-

An individual resource limit of $7,730.

-

A married couple resource limit of $11,600.

Which is better: Original Medicare or Medicare Advantage?

This depends on what your priorities are — if you find having a flexible network of doctors is important to you, Original Medicare could be the better option. Or, if you like the financial certainty of a maximum out-of-pocket and bundled care, Medicare Advantage is probably your best bet. It all comes down to what you want out of your healthcare and what you’d like your approach to be for Medicare costs — it’s different for everyone!