Use our life insurance calculator to find out how much life insurance you need to give you and your family ultimate peace of mind.

What is life insurance?

Life insurance is a “peace of mind product” designed to help protect your loved ones in the event of one of life’s more unpleasant certainties. If you’ve thought about what will happen to your family or loved ones after you’re gone, life insurance is a great option that comes in many different forms — and if you’re a full-time eligible employee, you might have been offered free life insurance by your employer.

Everyone’s needs are different, and a life insurance policy can be customized to your specific situation — like if you have young children, are caring for someone that doesn’t work outside the home or is unemployed for the foreseeable future. These factors can determine the type of plan you get — and where you get it from.

My employer offers free life insurance. Is that enough?

A lot of employers offer life insurance as part of their benefits package. If you’re lucky enough to be a full-time eligible employee, this is a great option! But the real question is: would it be enough?

There are some additional things to consider when deciding on the kind of life insurance that’s right for you and your loved ones. Your employer-provided life insurance may seem like the easy slam dunk choice, but it’s important to also think:

1. You could be saving money by going with your own policy. According to the National Association of Personal Financial Advisors (NAPFA), a healthy 50-year-old man could be saving almost 80% on premiums in the first year alone by switching to an individual life insurance plan from an employer-provided policy. In addition, NAPFA urges “young, healthy employees” to at least look at individual life insurance policies, as they can lock in lower rates for decades to come.

2. You may need more coverage than is allotted in this one-size-fits-all approach to your life insurance needs that most employer-provided plans take. Life insurance is intended to replace your income in the event of your untimely death, and employer-provided life insurance might work just fine for some people. But be careful if you have any of the following:

-

A stay-at-home partner

-

A mortgage loan

-

An unusual amount of debt (say, from higher education costs)

-

A large family

If so, an individual life insurance policy might be a better option for you, as your premature death could be a larger financial burden to your family.

3. You’ll lose your employer contribution to your life insurance if you lose your job. While we’re talking about unpleasant things, your life insurance policy benefits will be affected by a job loss or change. A move to part-time or contract work will leave you vulnerable to gaps in your employer-provided life insurance coverage. However, if you have your own policy, you’ll always be covered.

4. Your employer’s choice for life insurance may not cover your partner. While many of your employer’s insurance benefits extend to your partner, life insurance may not. Before you accept an employer’s job offer, make sure you carefully read all the details and know what you’ll need to pay out of pocket for all the coverage you want.

Ok. So how much life insurance should you buy?

We’re glad you asked! You should plan to buy a term life insurance policy that is valued at a minimum of 10 times your annual salary. This figure will change over the course of your life. So it’s a good idea to take a look at your life insurance policy every few years.

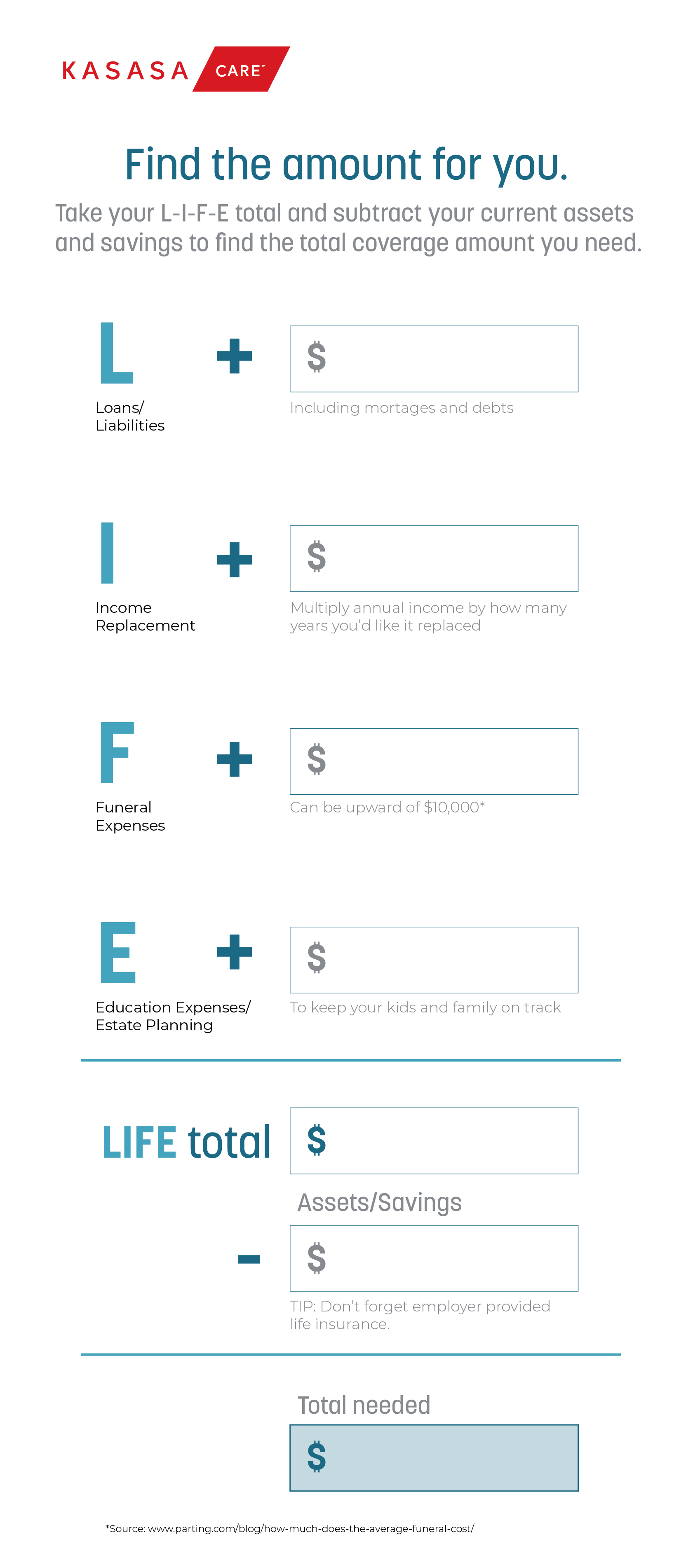

Your life insurance payout amount should reflect your salary as it increases over the course of your L-I-F-E. How can you get a better idea of what that number should be? Here’s a handy guide to get you started:

Do you have other options for life insurance?

It’s important you pick the right life insurance policy for you and your family’s needs. And just like any other form of insurance, you have options. If you’re in the market for life insurance, it’s important to take the time to shop around and get quotes from several companies before you choose an insurer. Additionally, you’ll want to make sure, wherever you choose, that the insurer is in good standing to be in business for the long haul, and does not run the risk of going out of business during your insurance plan timeline.

With so many more pleasant things to spend your time thinking about, it’s best to do a little research and planning for your end-of-life plan now. Enjoy every moment, knowing your loved ones are in good financial hands when you’re gone.